What Happens When AI Can Do Most of the Regulated Work?

For thirty years, financial planning and financial advice have largely travelled together.

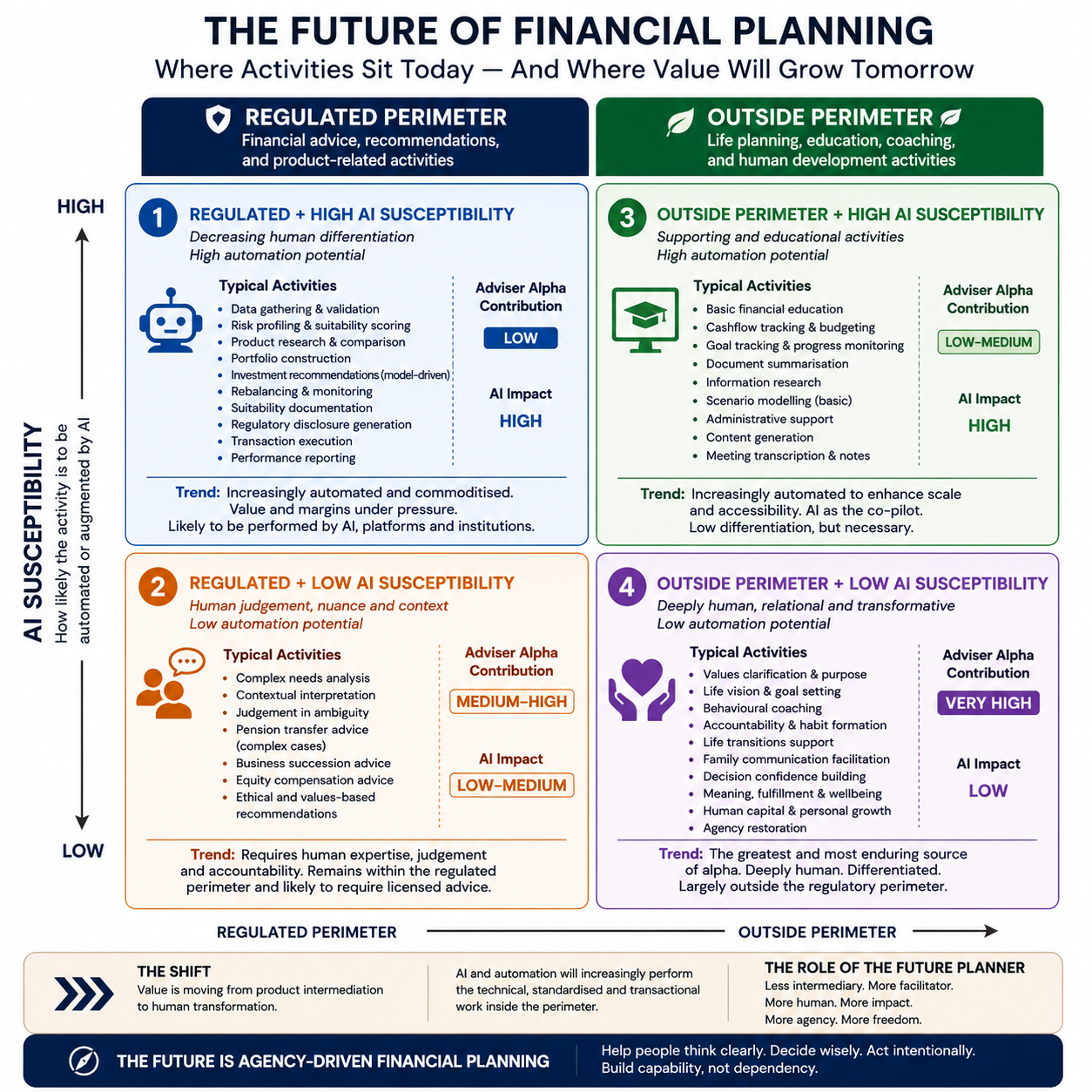

In practice, most consumers have experienced financial planning through the lens of regulated financial advice. The planner gathered information, analysed circumstances, made recommendations, arranged products, implemented transactions, reviewed outcomes, and managed ongoing relationships.

The two became almost synonymous.

But they were never actually the same thing.

One is a profession concerned with helping people make better life decisions.

The other is a regulated activity concerned with the distribution, recommendation, and implementation of financial products.

Historically, these activities were bundled together because they needed to be.

Tomorrow, they may not be.

And artificial intelligence is one of the reasons why.

What Actually Creates Value?

The famous Adviser Alpha studies repeatedly found that the greatest sources of value delivered by advisers were not product selection.

Instead, they came from activities such as:

- Behavioural coaching

- Helping clients avoid costly mistakes

- Goal clarification

- Decision support

- Accountability

- Tax awareness

- Spending discipline

- Retirement confidence

- Family communication

- Long-term planning

These are fundamentally human activities.

At the same time, many of the activities traditionally performed by advisers involve:

- Data gathering

- Fact finding

- Risk profiling

- Portfolio construction

- Product comparison

- Suitability documentation

- Regulatory disclosure

- Research

- Rebalancing

- Monitoring

These activities are process-driven, rules-based, and increasingly automatable.

This distinction matters.

Because one group of activities sits largely inside the regulatory perimeter.

The other sits largely outside it.

The Regulatory Perimeter Is Not The Profession

Financial regulators exist primarily to regulate financial products, recommendations, and transactions.

Activities typically associated with regulated advice include:

- Personal recommendations

- Product selection

- Investment recommendations

- Pension transfer recommendations

- Insurance recommendations

- Arranging transactions

- Executing transactions

- Managing investments

These functions exist because poor recommendations can cause financial harm.

But many activities commonly associated with financial planning sit outside the perimeter:

- Life planning

- Values clarification

- Goal setting

- Cashflow modelling

- Financial education

- Behavioural coaching

- Accountability

- Family discussions

- Life transitions

- Career planning

- Purpose and meaning

- Human capital development

- Social capital development

These activities influence financial outcomes.

Yet they are not generally regulated financial advice.

They are planning.

The distinction is becoming increasingly important.

AI Changes The Economics

Artificial intelligence excels at structured tasks.

It can:

- Analyse large datasets

- Compare products

- Generate reports

- Review documents

- Draft suitability assessments

- Model scenarios

- Identify inconsistencies

- Monitor portfolios

- Conduct research

- Automate administration

In many cases it can already perform these tasks faster and more consistently than humans.

These happen to be many of the activities located inside the regulatory perimeter.

By contrast, AI remains less capable at:

- Building trust

- Facilitating difficult conversations

- Resolving family conflict

- Understanding emotional context

- Supporting life transitions

- Developing wisdom

- Creating accountability

- Helping people navigate uncertainty

- Restoring confidence after setbacks

- Supporting human agency

These activities are increasingly where human value resides.

And many sit outside the regulatory perimeter.

The Financial Planner Of Today

The traditional financial planner often operates as an intermediary.

The process looks something like this:

Consumer → Planner → Financial Product

The planner gathers information.

The planner interprets information.

The planner recommends solutions.

The planner implements solutions.

The planner remains central to the decision-making process.

This model made sense when information was scarce and expertise was difficult to access.

The Financial Planner Of Tomorrow

A different model is beginning to emerge.

Consumer → AI → Planner → Consumer

In this model:

The AI helps the individual understand options.

The AI helps analyse information.

The AI helps prepare decisions.

The planner helps the person think.

The planner helps the person decide.

The planner helps the person remain aligned with their goals and values.

The planner becomes less intermediary and more facilitator.

Less gatekeeper and more guide.

Less adviser and more agency-builder.

The centre of gravity moves from institutional expertise to individual capability.

The Rise Of The Agency-Driven Planner

For decades, financial services has been built around delegation.

Consumers delegated understanding.

Consumers delegated analysis.

Consumers delegated decision-making.

Consumers delegated implementation.

AI changes that equation.

For the first time, ordinary individuals can access personalised intelligence at scale.

The planner’s role increasingly becomes helping people use that intelligence wisely.

Not replacing judgement.

Strengthening judgement.

Not creating dependency.

Building capability.

Not acting on behalf of the client.

Helping the client act on their own behalf.

This is agency-driven financial planning.

Will Future Financial Planners Need To Be Regulated?

Some will.

Anyone providing regulated financial advice, recommendations, arrangements, or discretionary management will remain subject to regulation.

That is unlikely to change.

But a growing number of planners may choose a different path.

One focused on:

- Education

- Planning

- Coaching

- Accountability

- Behaviour

- Decision support

- Human development

- Life planning

- Agency restoration

Activities that sit primarily outside the regulatory perimeter.

Activities increasingly difficult to automate.

Activities increasingly valuable in an AI-enabled world.

The Opportunity

This is not the end of financial planning.

It may be the beginning of financial planning becoming a profession in its own right.

Separate from product distribution.

Separate from financial intermediation.

Separate from institutional dependency.

A profession focused on helping people think clearly, decide wisely, and act intentionally across all areas of life.

As AI increasingly performs the technical work, the human planner becomes more human.

The question for today’s planners is simple:

Are you building a practice designed for the world that is disappearing?

Or the one that is emerging?

The Academy of Life Planning exists to help planners explore that future.

A future in which the most valuable work is not recommending products, but restoring human agency.