If Institutional Systems Are Supposed to Be More “Auditable, Accurate and Repeatable”… Why Don’t Advisers Trust Them?

For years, one of the major arguments made by large financial services technology providers has been that institutional systems are inherently safer and more reliable than individuals using AI tools independently.

The logic usually sounds something like this:

- institutional systems are auditable,

- workflows are controlled,

- outputs are repeatable,

- compliance oversight exists,

- and therefore the outcomes are more trustworthy.

Meanwhile, individuals using AI are often portrayed as operating in a dangerous “wild west” of hallucinations, inconsistency, and uncontrolled experimentation.

But a new survey from Defaqto introduces an uncomfortable question for the industry:

If institutional systems are genuinely delivering this superior consistency and reliability… why do advisers themselves appear not to trust the outputs?

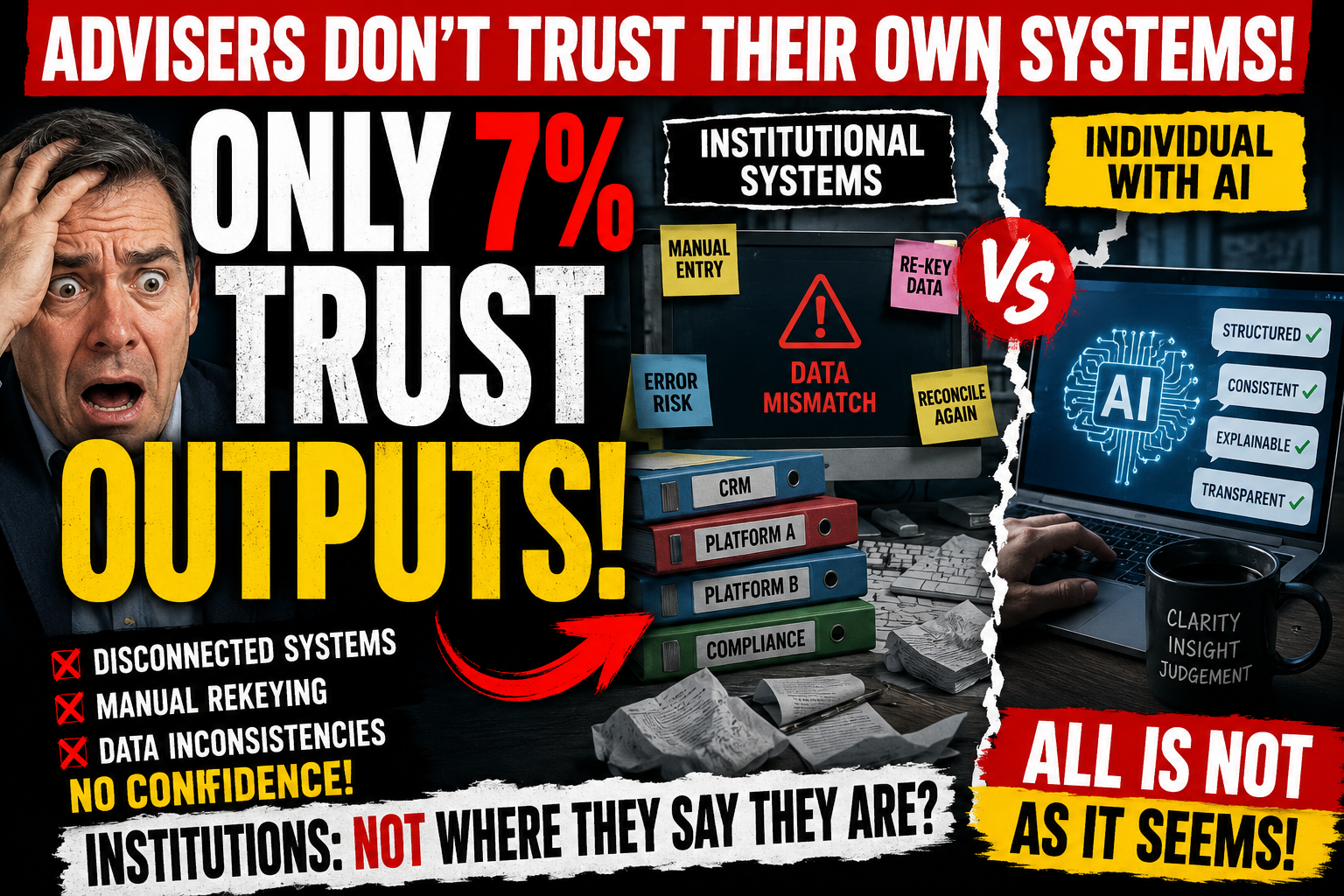

According to the research, only 7% of UK advisers are “very confident” that their technology systems produce consistent outputs.

That is an astonishingly low number.

Especially considering these are not consumers experimenting with early-stage AI tools at home.

These are regulated firms operating inside mature, expensive, enterprise-grade technology environments.

And the findings become even more revealing when examined more closely.

89% of advisers reportedly use three or more disconnected systems.

67% frequently re-enter the same client data multiple times.

Advisers are spending large portions of their working lives manually reconciling inconsistencies between platforms.

In other words:

the industry’s “trusted institutional infrastructure” is itself fragmented, duplicated, and operationally unstable.

The narrative being presented publicly — that institutions possess robust, unified, highly reliable decision environments while individuals merely possess risky AI tools — may not be entirely accurate.

Or at least not yet.

Because what this survey actually exposes is something deeper:

many institutional systems are still collections of disconnected silos stitched together through human effort.

That matters enormously.

Especially now.

Because the criticism often directed toward consumer AI is:

- “How do you audit it?”

- “How do you know the outputs are accurate?”

- “How do you ensure consistency?”

- “How do you avoid hallucinations?”

- “How do you maintain compliance oversight?”

Yet advisers themselves appear to be saying:

“We already struggle with those problems inside institutional systems.”

That does not mean consumer AI is automatically safe.

Nor does it mean professional advice becomes irrelevant.

Far from it.

But it does challenge the simplistic assumption that institutions already possess the coherent, trustworthy, integrated technological superiority they often imply.

The reality may be more nuanced.

Many firms are still operating across fragmented architectures built over decades:

- legacy back-office systems,

- separate cashflow tools,

- disconnected CRMs,

- external platforms,

- provider portals,

- suitability systems,

- compliance overlays,

- fragmented data structures.

The human adviser frequently becomes the integration layer.

Not the technology.

And that creates a fascinating shift in the conversation.

Because increasingly, the question is no longer:

“Can AI replace advisers?”

The more important question may be:

“Who can create coherent systems that genuinely help human beings think clearly inside complexity?”

That is a very different challenge.

At the Academy of Life Planning, we believe the future is unlikely to belong solely to either:

- giant institutional infrastructures,

or - isolated individuals using generic AI tools alone.

The future likely belongs to those who can combine:

- human judgement,

- contextual understanding,

- structured thinking frameworks,

- transparent reasoning,

- and intelligent technology support.

In other words:

capability systems.

Not merely automation systems.

That distinction matters.

Because automation without coherence simply accelerates confusion.

And adding more disconnected tools does not necessarily create more trustworthy outcomes.

Sometimes it simply creates more layers to reconcile.

This is why the emerging role of the Total Wealth Planner is becoming increasingly important.

Not as a product distributor.

Not merely as a compliance process manager.

But as a structured thinking partner helping individuals maintain clarity, judgement, and agency in increasingly complex systems.

The irony is difficult to ignore.

At precisely the moment institutions are warning consumers about trusting AI outputs…

many advisers appear unconvinced by the outputs of their own institutional technology environments.

All may not yet be as seamless, auditable, and repeatable as the marketing narratives suggest.

And perhaps that honesty is where the next phase of financial planning begins.

Not with the illusion of certainty.

But with the transparent design of systems that genuinely help human beings stay capable.

Curious how others see this.