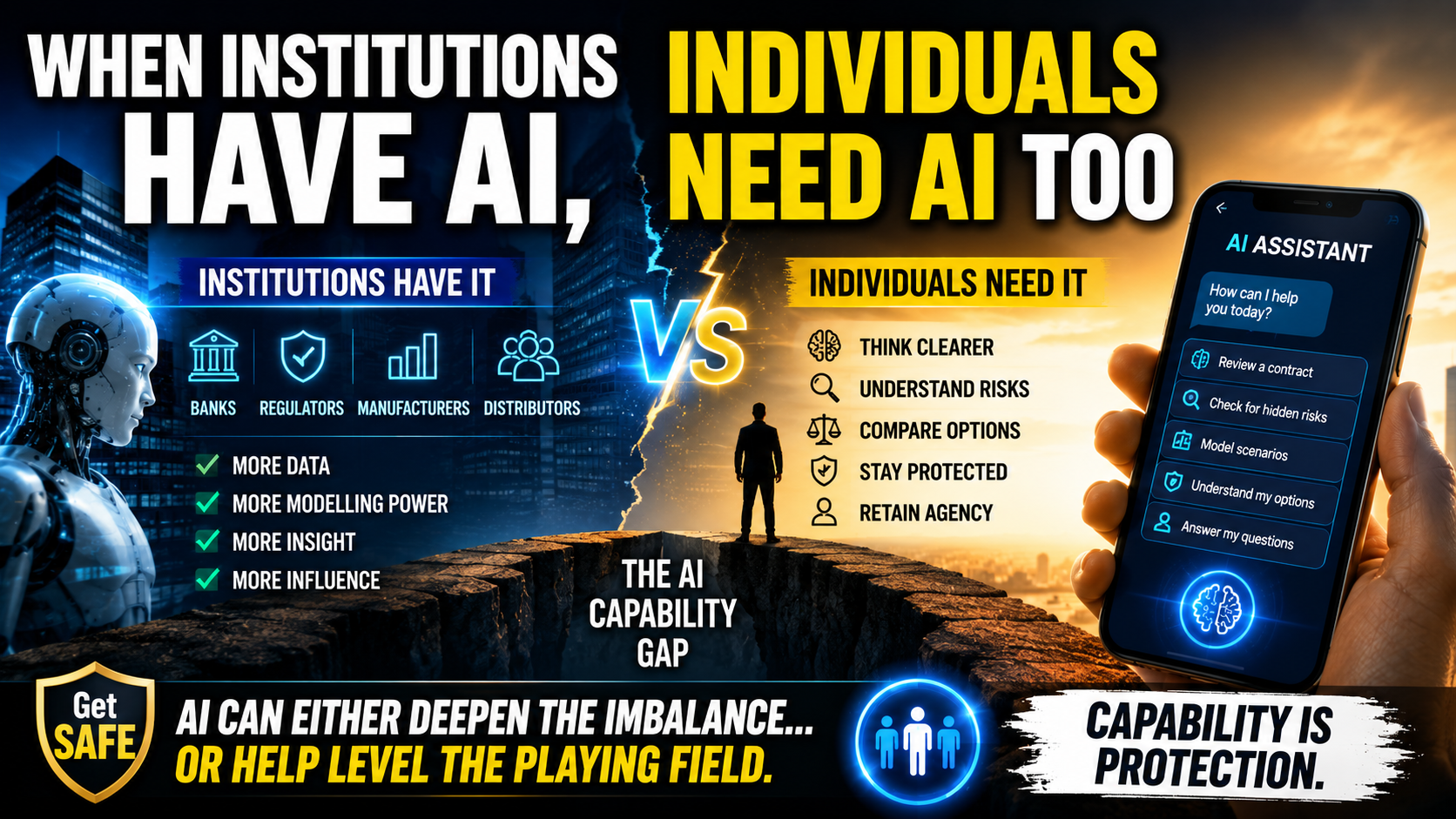

What we are likely witnessing is the rapid institutionalisation of AI capability across financial services.

If “hundreds” of firms are applying to the Financial Conduct Authority AI sandbox, that suggests:

- distributors,

- manufacturers,

- platforms,

- insurers,

- wealth managers,

- banks,

- and fintechs

are all racing to build AI-enhanced operational and decision systems.

And importantly, they are not doing this for philosophical reasons.

They are doing it because AI potentially gives them:

- faster scalability,

- behavioural insight,

- lower servicing costs,

- enhanced client retention,

- predictive analytics,

- automated nudging,

- personalised persuasion,

- and institutional leverage.

In other words: institutional capability is being supercharged.

That creates a very important societal question.

If institutions have AI… regulators have AI… manufacturers have AI… scammers have AI…

…should individuals also have AI capability?

I would argue yes.

Not merely for convenience. But for balance.

Here’s a simple way to think about this:

Historically, institutions possessed asymmetrical capability:

- more information,

- more processing power,

- more modelling capability,

- more legal understanding,

- more behavioural insight.

AI potentially widens that gap dramatically unless individuals also gain access to structured capability systems.

That does not necessarily mean everyone needs “AI advice.”

It means people increasingly need:

- cognitive support,

- structured thinking tools,

- scenario exploration,

- pattern recognition,

- document interpretation,

- decision support,

- and systems that help them remain capable under stress.

That is very aligned with the underlying logic of AoLP & Get SAFE.

Because many victims of financial harm do not primarily suffer from lack of intelligence.

They suffer from:

- cognitive overload,

- asymmetry,

- complexity,

- intimidation,

- fragmented information,

- emotional exhaustion,

- and institutional process advantage.

AI can either deepen that imbalance…

…or help level it.

That is why your framing around: “The AI leveller” is strategically powerful.

The key issue then becomes: what kind of AI?

If AI simply channels people back into institutional dependency, little changes.

But if AI helps people:

- organise evidence,

- understand contracts,

- model options,

- ask better questions,

- identify risks,

- improve clarity,

- and maintain agency under pressure,

then AI becomes a capability amplifier rather than merely a sales or optimisation engine.

I suspect this is where AoLP and Get SAFE become increasingly differentiated over the next few years.

Not because they are “anti-institution.”

But because they are asking a deeper question:

How do we help human beings stay capable inside increasingly intelligent systems?

That feels like one of the defining social questions of the AI era.

Curious how others in financial services are thinking about this balance between institutional AI capability and individual AI capability.