The UK financial advice sector may be approaching another quiet inflection point.

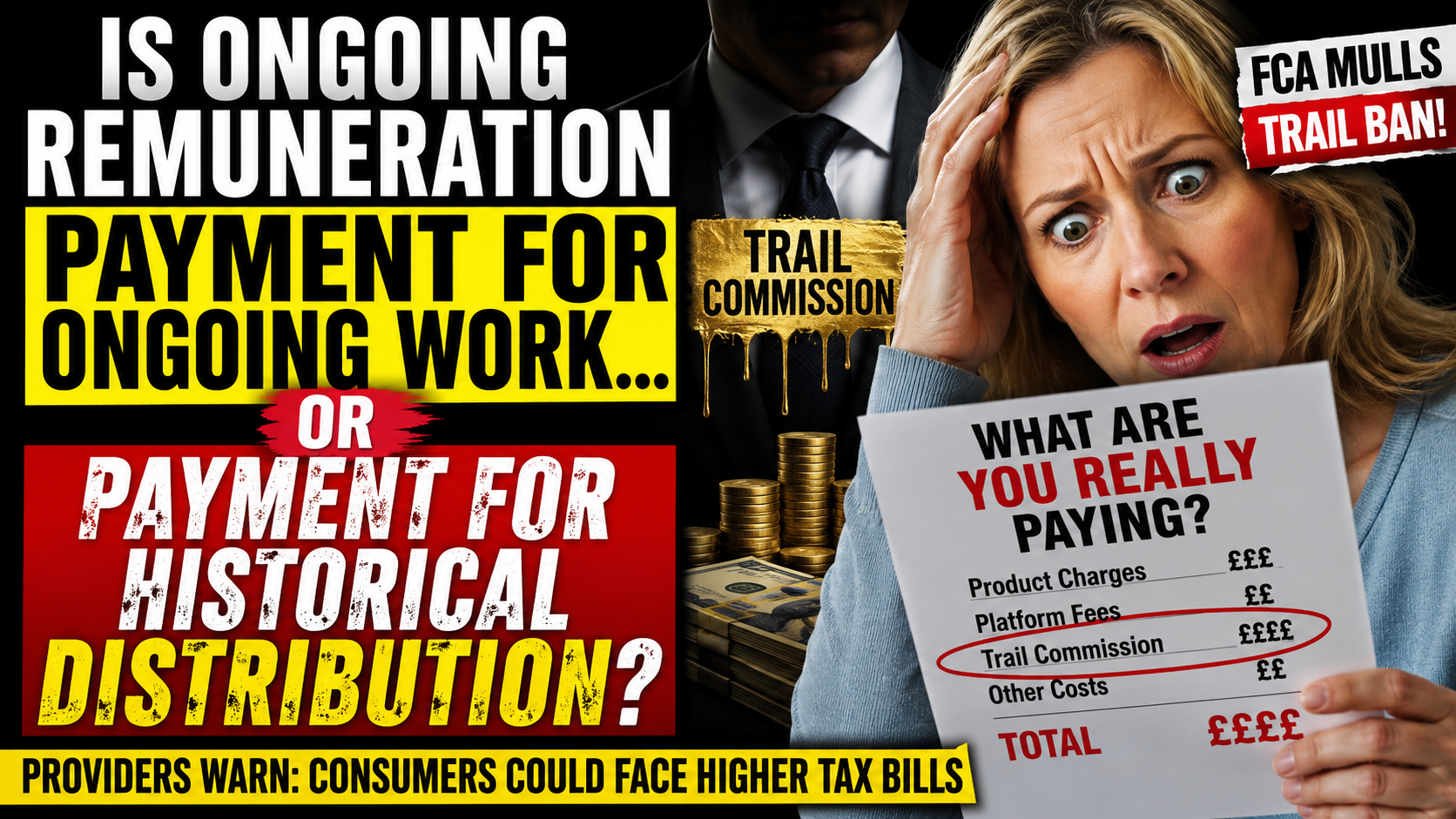

Recent reports suggest the FCA is examining the future of trail commission as part of its broader review of simplified advice and targeted support. Industry responses have been swift. Some providers and commentators warn that banning trail commission could create unintended consequences for consumers, including potential Capital Gains Tax or income tax implications where existing arrangements inside GIAs or investment bonds are disrupted.

Those concerns should not be dismissed lightly.

But beneath the technical arguments sits a much deeper question — one the profession may increasingly struggle to avoid:

Is ongoing remuneration genuinely payment for ongoing work…

or is it, in some cases, residual payment for historical distribution?

That distinction matters.

For many years, trail commission was normalised as part of the architecture of financial services. Products paid advisers ongoing income. Consumers rarely saw explicit invoices. The economic model sat quietly in the background.

And to be fair, many advisers using trail commission have provided enormous value to clients over long periods:

- reassurance during market crashes,

- behavioural coaching,

- retirement planning,

- intergenerational support,

- vulnerability management,

- tax planning,

- and trusted long-term relationships.

The issue is not whether good advisers exist.

The issue is whether the remuneration structure itself creates the right incentives.

Because structurally, trail commission can blur several important lines.

First, it weakens visibility.

Many consumers still struggle to explain precisely what they pay, what they receive in return, and how those charges evolve over time. Percentage-based charging often feels psychologically distant compared to explicit pound-note pricing.

Second, it rewards asset retention more than demonstrable human value.

If remuneration continues regardless of whether meaningful planning work is occurring, consumers may reasonably ask what exactly the ongoing payment represents.

Third, it embeds inertia.

Consumers frequently remain inside arrangements not because they have consciously re-evaluated value, but because changing course feels administratively difficult, emotionally uncomfortable, or financially unclear.

This is where the industry’s defence becomes revealing.

The strongest defence of ongoing remuneration is not:

“We need recurring income.”

It is:

“Clients need recurring support.”

Those are not the same argument.

One centres the business model.

The other centres the human being.

And AI may accelerate this distinction dramatically.

Large parts of traditional advisory infrastructure are already becoming automatable:

- report writing,

- data gathering,

- portfolio analysis,

- annual review preparation,

- suitability drafting,

- compliance checking,

- and information retrieval.

As these functions become cheaper and faster, consumers are likely to ask harder questions about what remains uniquely valuable.

The answer will not simply be product access.

Nor administrative processing.

Nor information asymmetry.

The future value of human planners may increasingly rest in areas machines struggle to replicate:

- judgement under uncertainty,

- emotional regulation,

- accountability,

- behavioural coaching,

- family dynamics,

- ethical interpretation,

- life transition support,

- meaning-making,

- and helping people navigate complexity without losing agency.

In other words: human capability development.

This is where the Academy of Life Planning believes the conversation becomes important.

Because the industry may be entering a transition from:

invisible extraction…

towards visible, intentional partnership.

That transition will feel uncomfortable for some firms because it exposes a difficult truth:

Technology is reducing the value of distribution while increasing the value of trust, judgement, and human relational work.

Historically, distribution itself held enormous economic power. Advisers controlled access to products, platforms, information, and implementation pathways.

But in an AI-enabled world, access becomes increasingly commoditised.

What remains scarce is clarity.

What remains scarce is wisdom.

What remains scarce is trusted human interpretation.

And this may explain why the debate around trail commission feels emotionally charged.

Because it is not merely a pricing debate.

It is a debate about what financial planning actually is.

Is it primarily:

- a distribution function attached to financial products?

Or:

- a human developmental profession focused on helping people navigate life, money, complexity, and uncertainty?

Those are profoundly different futures.

From an AoLP perspective, the answer is unlikely to be found in simplistic slogans like “commission bad” or “fees good.”

The more important principle is conscious, informed agency.

Consumers should clearly understand:

- what they are paying,

- why they are paying it,

- what work is being performed,

- what outcomes are realistic,

- and where human value genuinely exists.

Because trust built on clarity is far more durable than trust built on opacity.

And perhaps that is the deeper issue the FCA is now circling around — even if indirectly.

Not whether advisers should be paid.

But what, exactly, society believes they are being paid for.