Today’s events brought an important lesson into sharp focus.

The greatest risk during periods of complexity, stress, or change is not always lack of information.

It is the loss of agency.

This matters deeply for Total Wealth Planners because people rarely lose agency all at once. It is often eroded gradually by complexity, professional authority, emotional pressure, institutional processes, and too many well-intentioned people trying to help.

The lesson is simple but profound:

A Total Wealth Planner does not take over. A Total Wealth Planner helps a person become capable again.

1. Consumer protection must not become professional protection

Total Wealth Planners must learn to distinguish between genuine consumer protection and professional protection dressed in consumer-protection language.

A message may sound responsible on the surface:

“Do not rely on AI.”

“Do not trust quick answers.”

“Use a professional.”

But for the majority of people who do not have access to human financial advice, that message may not protect them. It may leave them with fewer tools, less confidence, and more dependency.

The key question is not:

“Does this message defend professional standards?”

The better question is:

“Does this message increase or reduce the agency of the person with least access to support?”

A Total Wealth Planner must always look beyond the surface message and ask who benefits, who is excluded, and whether the narrative restores or restricts individual capability.

2. Human-first does not mean adviser-first

A human-first world is not one where professional authority remains at the centre.

Human-first means the individual remains at the centre.

AI should not replace human judgement. But AI can support human judgement, especially for people who otherwise have no structured support at all.

Used safely, AI can help people understand documents, prepare questions, identify inconsistencies, structure their thinking, surface options, challenge confusing narratives, and regain confidence before speaking to professionals.

The real risk is not that ordinary people use AI.

The deeper risk is that institutions, firms, advisers, platforms, and professional service providers use AI to increase their capability, while individuals are warned away from using AI to increase their own.

That creates capability asymmetry.

Total Wealth Planners must challenge that asymmetry.

3. Do not take stated intentions at face value

In contentious exchanges, a Total Wealth Planner must not read only the surface text.

People may say they are protecting consumers, improving outcomes, raising standards, or defending quality. They may sincerely believe this. But the planner must also examine commercial incentives, power relations, status threat, emotional spikes, reputational defence, what is being protected, what is being obscured, and whether the narrative increases or reduces agency.

This does not mean making reckless accusations about motive.

It means separating three things:

What is evidenced.

What can reasonably be inferred.

What remains unproven.

That discipline protects fairness while avoiding naivety.

Fair outcomes matter more than favourable outcomes.

4. Helping is not the same as restoring agency

In complex cases, there may be institutions, professionals, campaigners, investigators, journalists, experts, AI tools, friends, family members, and multiple well-intentioned helpers involved.

Every one of them may believe they are helping.

Yet the person at the centre can still become more confused, not less.

Not because nobody cares.

Because too many people may be trying to solve the problem for them.

A Total Wealth Planner must learn to distinguish between:

helping someone solve a problem,

and

helping someone remain the author of their own life while solving the problem.

The first can create dependency.

The second restores agency.

5. The planner serves the person, not the outcome

Helpers can easily become attached to outcomes.

One person may become attached to settlement.

Another may become attached to accountability.

Another may become attached to exposing wrongdoing.

Another may become attached to winning a point of principle.

Each attachment may be understandable. But each can create pressure around the person at the centre.

The Total Wealth Planner’s role is different.

The planner asks:

“What decision does this person need to make next, and how do I help them make it clearly?”

Not:

“How do I get them to choose the strategy I prefer?”

The planner serves the person.

Not the institution.

Not the campaign.

Not the strategy.

Not the preferred outcome.

Not even their own expertise.

6. Capability is often present but temporarily inaccessible

People under stress are often described as overwhelmed, confused, exhausted, emotional, or unable to cope.

Yet those same people may still be spotting contradictions, remembering key documents, identifying inconsistencies, asking intelligent questions, and sensing when something does not feel right.

Their capability has not disappeared.

It may simply be buried beneath stress.

This is a vital insight for Total Wealth Planners.

People in crisis are often treated as though they lack capability. In reality, their capability may be temporarily inaccessible because of fear, trauma, overload, complexity, or pressure.

The planner’s job is not to replace that capability.

It is to uncover it.

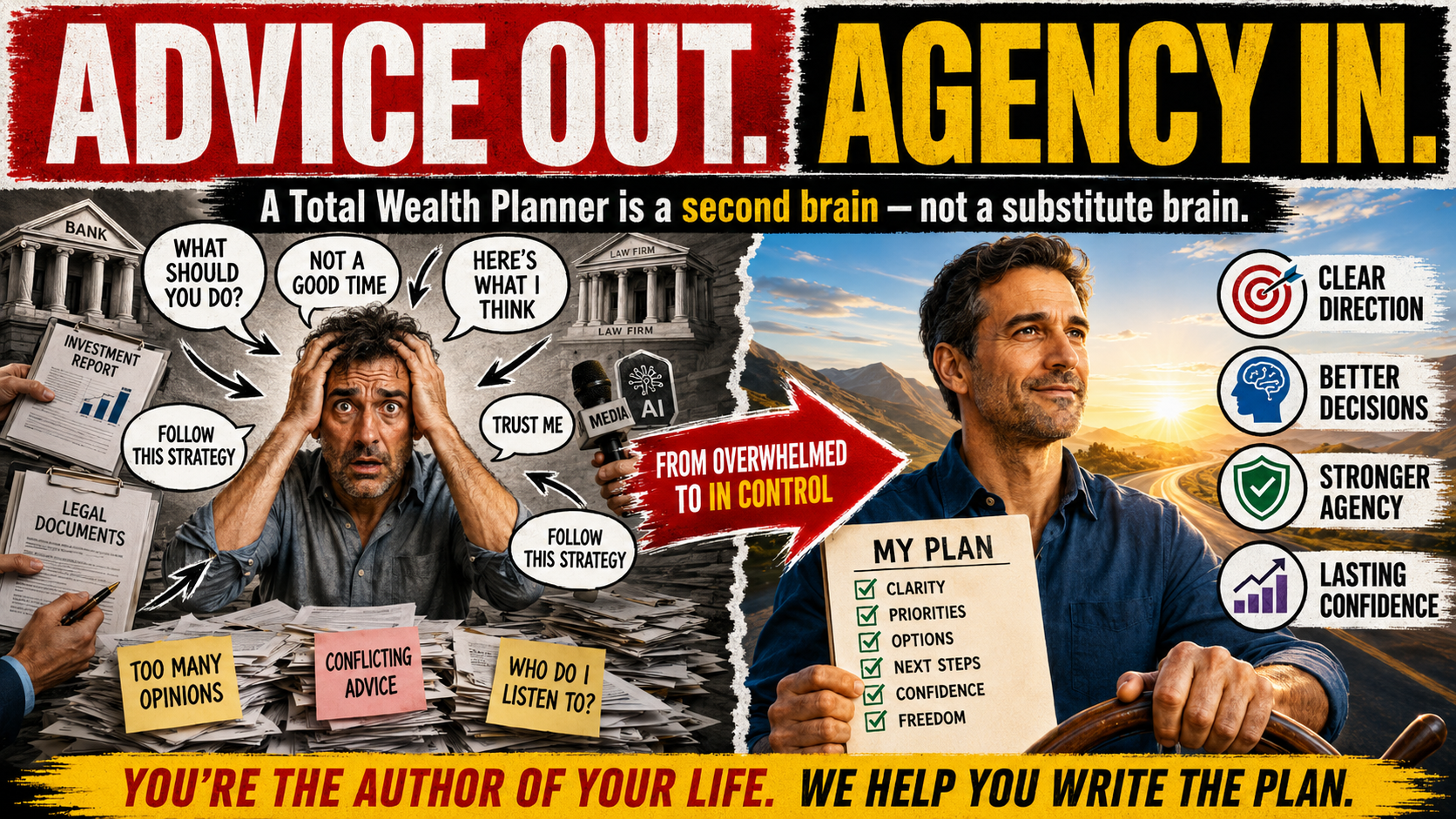

7. A Total Wealth Planner is a second brain, not a substitute brain

This may become one of the defining principles of the profession.

A Total Wealth Planner is a second brain.

Not a substitute brain.

The role is to help someone stabilise, structure, and surface options so they can think clearly again.

The planner crosses a line when they start directing, deciding, negotiating on behalf of, controlling the narrative, becoming emotionally attached to outcomes, or measuring success by whether their preferred strategy wins.

The proper measure of success is simpler:

“Is this person becoming more capable of navigating their own life?”

If the answer is yes, agency is being restored.

If the answer is no, dependency may be being created.

8. Advice out. Agency in.

Together, today’s lessons reinforce the Academy’s central philosophy:

Advice out. Agency in.

This does not mean people should be abandoned to work everything out alone.

It means support should be designed to return authority to the individual, not transfer authority away from them.

The Total Wealth Planner does not take the wheel.

The Total Wealth Planner helps the individual regain the confidence, clarity, and capability to drive their own life again.

That is the distinction.

That is the profession.

And that is why Total Wealth Planning matters.