For years, consumers have been told to look for one word when choosing a financial professional:

“Fiduciary.”

The term sounds reassuring. Protective. Dependable.

It suggests the person sitting across the table is legally and ethically required to put your interests first.

And in many ways, that is true.

But there is a deeper question very few people ask:

What if the structure itself quietly influences what “best interests” looks like?

Because this is where the conversation becomes more complicated — and more important.

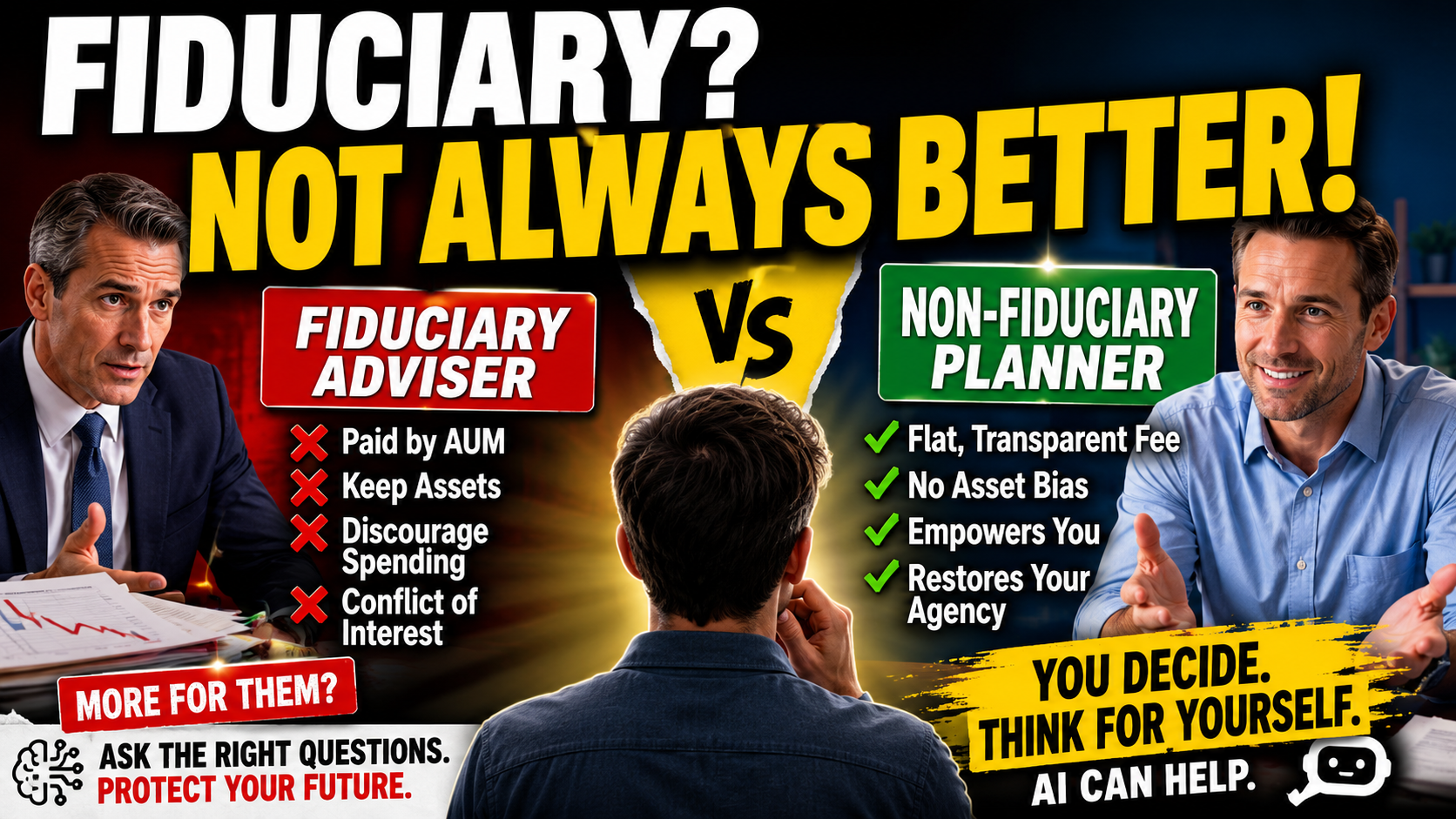

A fiduciary adviser can still operate inside a business model where their income depends on:

- gathering assets,

- retaining assets,

- discouraging spending,

- discouraging debt repayment,

- discouraging property purchases,

- discouraging annuities,

- and resisting strategies that reduce assets under management.

This does not automatically make the adviser dishonest.

In fact, many advisers genuinely care deeply about their clients.

But behavioural science has repeatedly shown that incentives influence judgement — often subconsciously.

Human beings naturally tend to:

- rationalise existing incentives,

- normalise prevailing industry models,

- interpret ambiguous situations favourably,

- and sincerely believe their conclusions are objective.

That is not corruption.

It is human psychology.

And it means something very important for consumers:

A “fiduciary” label does not necessarily mean the system itself is free from structural conflicts.

The adviser may still be operating within an environment where:

- keeping assets invested,

- retaining client dependency,

- and preserving recurring revenue

quietly shape the recommendations that feel “reasonable.”

Now compare that to a different type of planner.

Imagine someone who:

- charges a transparent flat fee,

- does not manage your investments,

- does not earn more if you keep assets invested,

- does not lose income if you buy property,

- does not benefit from retaining control over your money,

- and focuses instead on helping you think clearly.

This planner may not legally qualify for the same fiduciary badge.

Why?

Because the regulatory system often defines fiduciary status around regulated investment activity — not around whether the underlying business model is structurally aligned with human agency.

And this creates an uncomfortable possibility:

The consumer’s real-world interests could absolutely be better served by the non-fiduciary planner than by the fiduciary adviser.

Especially if the consumer’s goals involve:

- freedom,

- autonomy,

- life design,

- family priorities,

- reducing stress,

- buying a home,

- starting a business,

- paying off debt,

- helping children,

- or simply living more fully.

Because sometimes the best outcome for a human being is not:

“maximise investable assets.”

Sometimes it is:

“maximise life.”

This is one of the biggest blind spots in modern financial services.

The system often assumes that protecting consumers means:

- regulating products,

- regulating transactions,

- regulating advice processes,

- and enforcing disclosures.

But far less attention is given to:

- whether the system increases dependency,

- whether incentives distort judgement,

- whether consumers are becoming more capable,

- and whether human agency itself is being strengthened or weakened.

At the Academy of Life Planning, we believe this distinction matters.

A trustworthy system is not simply one where disclosures are made correctly.

A trustworthy system is one designed to:

- minimise extraction,

- reduce hidden incentives,

- increase transparency,

- restore independent thinking,

- and help people make conscious decisions aligned with their own lives.

That does not mean fiduciary advisers are “bad.”

Nor does it mean non-fiduciary planners are automatically “good.”

It simply means consumers should look deeper than labels.

Ask:

- How is this person paid?

- What incentives exist in the model?

- Does this framework increase my agency or reduce it?

- Am I being educated or managed?

- Is the goal to help me think — or to keep me invested?

Because in the age of AI, behavioural governance, and increasingly complex financial systems, the real question may no longer be:

“Is this person a fiduciary?”

But rather:

“Does this system help me remain the author of my own life?”

That is a very different standard of trust.

Before accepting any recommendation — fiduciary or otherwise — pause and think independently.

In the age of AI, consumers now have something previous generations never had:

A neutral thinking companion available on demand.

That does not mean AI is always right.

It is not.

But it does mean you no longer have to process complex financial recommendations alone.

For the first time in history, ordinary people can:

- upload documents,

- analyse suitability reports,

- compare reasoning,

- explore alternative viewpoints,

- and interrogate assumptions

without immediately depending on another institution.

You might even ask AI questions such as:

- How is this person paid?

- What incentives exist in this model?

- Does this framework increase my agency or reduce it?

- Am I being educated or managed?

- Is the goal to help me think — or to keep me invested?

- What alternative options might exist outside the recommended structure?

- What assumptions is this recommendation making about my priorities and future?

Not because advisers are bad.

But because independent thinking matters.

The future of consumer protection may not come solely from more regulation.

It may also come from restoring the individual’s ability to think clearly inside increasingly complex systems.

That changes the balance of power.

And perhaps that is the most important shift of all.

Because the real goal is not replacing one authority with another.

It is helping people become more conscious participants in decisions that shape their lives.