By Steve Conley

What if the problem was never access… but activation?

For decades, financial services has framed its central challenge as an “advice gap.”

Not enough advisers.

Not enough access.

Not enough affordability.

But the NHS—facing far greater scale, complexity, and pressure—took a different view.

They asked a more fundamental question:

What if most people don’t need more intervention…

but better support to manage things themselves?

The NHS Insight That Changed Everything

Within the NHS, a concept emerged that quietly reshaped how care is delivered:

The Patient Activation Measure (PAM)

PAM is a simple but powerful tool.

It assesses a person’s:

- Knowledge

- Skills

- Confidence

…to manage their own health and wellbeing.

Rather than assuming everyone needs the same level of care, PAM recognises something critical:

People are at different levels of readiness.

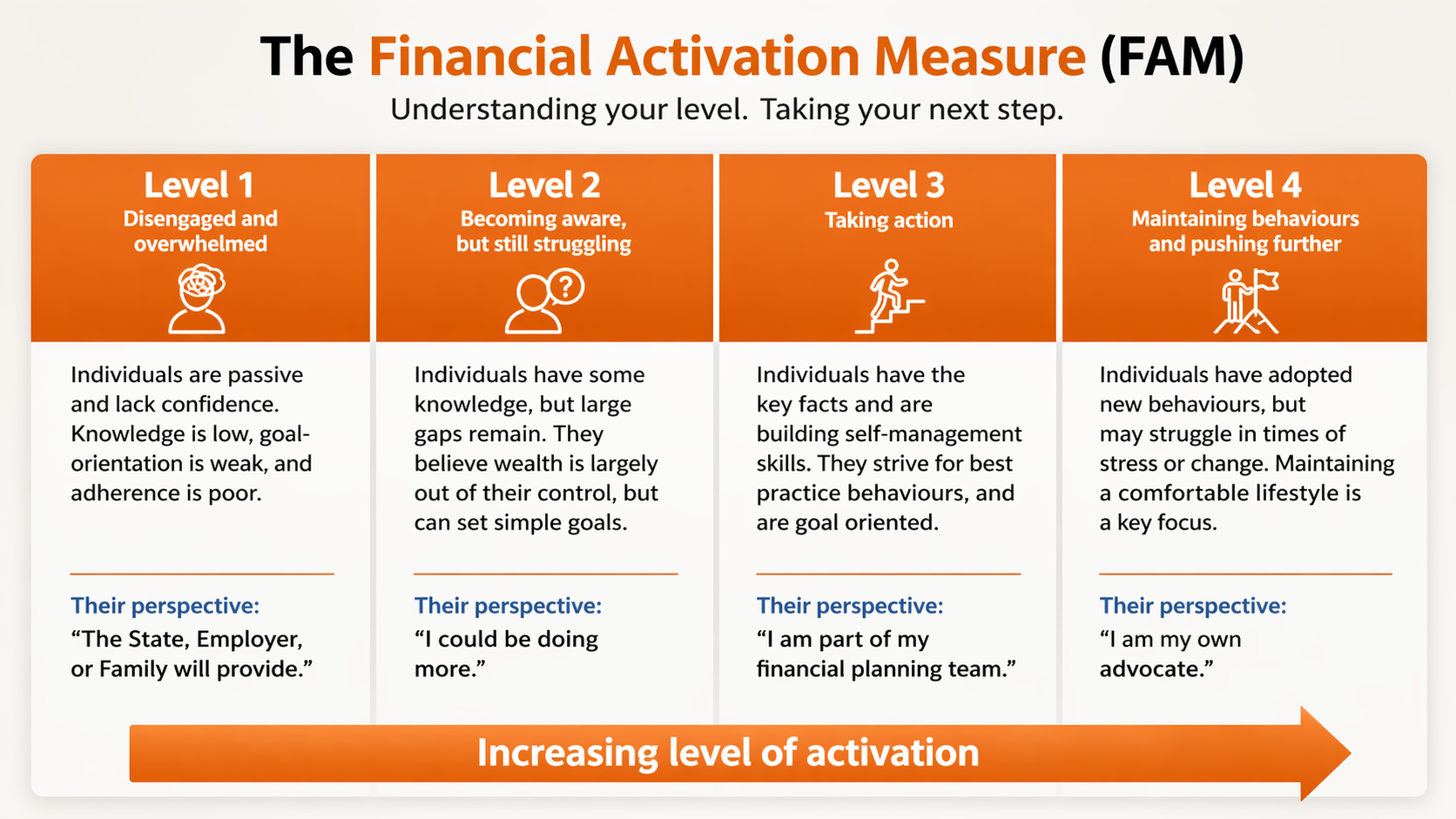

The Four Levels of Activation

The NHS identified a clear progression:

- Level 1: Passive, overwhelmed

- Level 2: Lacking knowledge and confidence

- Level 3: Taking action

- Level 4: Maintaining behaviours and progressing further

This wasn’t just theory.

It transformed how care is delivered.

A Radical Shift: From Treatment to Activation

The NHS began to move away from a “one-size-fits-all” model.

Instead, they used PAM to:

- Tailor support to the individual

- Avoid over-servicing those who are capable

- Focus resources on those who truly need help

Because without this:

The capable are over-supported

The vulnerable are under-supported

The Hidden Truth: Most People Can Self-Manage

At the heart of this approach is a simple but powerful belief:

With the right support, most people can manage their own health most of the time.

And the evidence backs this up.

More activated individuals:

- Make better decisions

- Adopt healthier behaviours

- Require fewer interventions

- Experience better outcomes

Activation isn’t fixed.

It can be developed.

So Why Has Financial Planning Not Followed?

Now consider the financial world.

We have:

- More tools than ever

- Instant access to information

- AI capable of modelling almost anything

And yet:

- People still feel overwhelmed

- Decisions are delayed or outsourced

- Dependency remains the default

The industry response?

More advice.

More complexity.

More intermediation.

But what if the NHS is right?

Introducing the Financial Activation Measure (FAM™)

At the Academy of Life Planning, we asked:

What if financial planning has the same problem healthcare had?

Not a lack of expertise.

But a lack of activation.

FAM™ is the financial equivalent of PAM

It measures a person’s:

- Ability to earn, save, invest and protect

- Confidence to make decisions

- Readiness to take control

Not their wealth.

Not their portfolio.

But:

Their capacity to manage their financial life.

From Advice Gap to Activation Gap

The traditional model assumes:

People need experts to take control.

The activation model recognises:

People need support to take control.

That’s a fundamental shift.

Why This Matters in the Age of AI

In 2026, the landscape has changed.

AI can:

- Analyse portfolios

- Model outcomes

- Explain financial concepts

So the constraint is no longer:

Access to information

It is:

The ability to decide and act

The Role of FAM™

FAM™ does three critical things:

1. It identifies where someone is

Not financially—but behaviourally.

2. It prevents premature advice

Not everyone is ready for complex planning.

3. It enables tailored support

Just like PAM, it allows support to be:

- Proportionate

- Personalised

- Effective

The 90/10 Reality

The NHS operates on a simple truth:

Most people can manage most of their health most of the time.

Financial planning is no different.

At AoLP, we believe:

- Most people can manage their finances

- With the right structure

- And the right support at the right time

Some will need one-to-one help.

But not all.

And not always.

From Dependency to Agency

This is not about removing support.

It’s about placing it where it belongs:

- After activation, not before

- In support of decisions, not in place of them

What Comes Next

Understanding your level of financial activation is the starting point.

From there:

- You build your Total Wealth Plan

- You develop your decision-making capability

- You move from passenger → pilot

Final Thought

The NHS didn’t scale by treating everyone.

It scaled by activating people.

Financial planning now faces the same choice.

The future of financial wellbeing will not be built on advice alone.

It will be built on activation.

Ready to begin?

Discover your Financial Activation Level—and take the first step towards building your Total Wealth Plan.