[A reflection on Citywire’s article, How SJP advisers are using Policy Services to pitch independent advice 14 May 2026]

By Steve Conley

The financial advice profession has spent decades arguing over a question that, from a genuine life planning perspective, may matter far less than the industry would like to believe.

Restricted or independent?

Whole of market or vertically integrated?

Our products or someone else’s products?

To many within the profession, these distinctions are presented as fundamental. Existential, even. Entire business models, regulatory narratives, and marketing campaigns are built around them.

But step back from the rhetoric for a moment and ask a more uncomfortable question:

How much difference does it actually make to a person’s life?

The answer, in most cases, is surprisingly little.

That is not because investment products are irrelevant. Investments have a role. Tax wrappers matter. Asset allocation matters. Costs matter. Good governance matters.

But the reality is that most retail investment products are now heavily commoditised.

A globally diversified portfolio is no longer difficult to construct. Platforms have converged. Managed portfolio services have converged. Centralised investment propositions have converged. Risk profiling has converged. Even the language used across the market increasingly sounds the same.

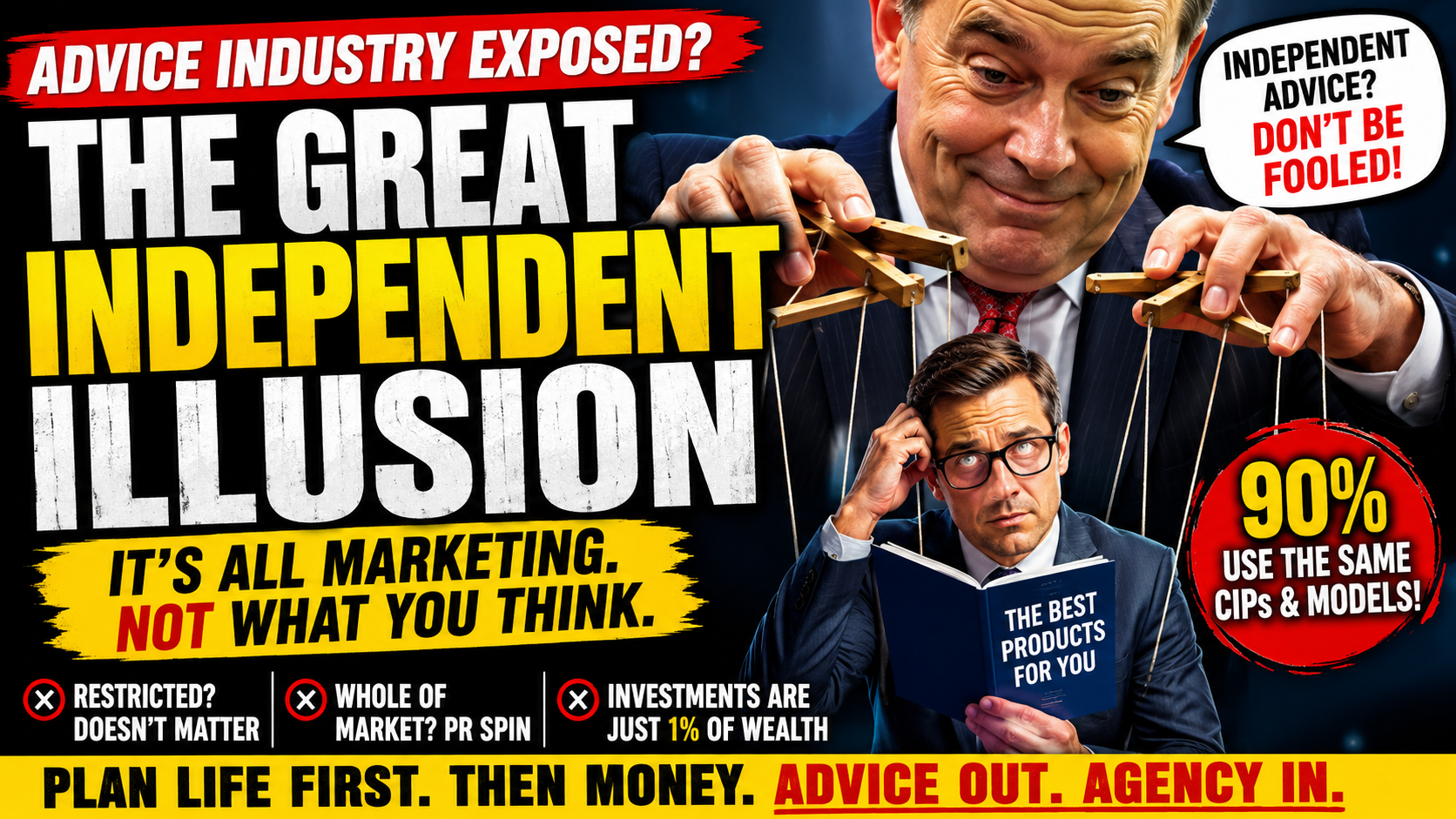

Meanwhile, many firms operating under the banner of “independent advice” are, in practice, functioning through tightly controlled proposition architecture anyway.

They may legally access the whole market, but operationally:

- they use a small number of platforms,

- a centralised investment proposition,

- outsourced discretionary fund managers,

- model portfolios,

- standardised suitability frameworks,

- and repeatable client segmentation processes.

That is not necessarily a criticism. Standardisation can improve consistency and reduce operational risk.

But it does challenge the mythology.

The image often projected to consumers is one of a planner tirelessly searching the entire market for a uniquely tailored solution. In reality, many clients end up in one of several broadly similar portfolios inside one of several broadly similar operating systems.

The practical distinction between “restricted” and “independent” is often far narrower than the marketing suggests.

And from a life planning perspective, the distinction narrows further still.

Because retail investments are not the centre of most people’s lives.

They are not even close.

The average person’s long-term wellbeing is shaped far more profoundly by:

- health,

- relationships,

- purpose,

- resilience,

- career decisions,

- housing,

- debt,

- behavioural habits,

- family stability,

- skills,

- time,

- community,

- and emotional capability,

than by whether they were placed into Fund A or Fund B.

Indeed, regulated retail investments may represent only a tiny fraction of total lived wealth for the average Brit.

Human capital alone — the ability to earn, adapt, create, relate, and contribute — vastly outweighs most investment portfolios in both economic and existential significance.

Yet the industry continues to behave as though product architecture is the primary battleground of financial wellbeing.

Why?

Because products are where the commercial economics traditionally sit.

That is the uncomfortable truth beneath much of the noise.

The “independent versus restricted” debate is often less about human flourishing and more about distribution models competing for legitimacy.

This is why the emerging AI era matters so much.

Artificial intelligence is rapidly eroding information asymmetry — the historic advantage institutions held through complexity, technical language, fragmented access to knowledge, and consumer dependence on intermediaries.

For the first time, ordinary individuals can:

- interrogate charging structures,

- compare propositions,

- understand conflicts,

- learn financial concepts,

- challenge assumptions,

- and model scenarios,

without needing to defer entirely to institutional authority.

That does not eliminate the value of planners.

But it changes what valuable planning actually is.

The future planner is unlikely to win because they have access to a marginally different investment shelf.

They will win because they help people:

- think clearly,

- navigate complexity,

- maintain emotional stability,

- structure decisions,

- align money with meaning,

- and preserve agency in an increasingly confusing world.

That is a fundamentally different proposition.

Not product superiority.

Human capability development.

The irony is that the industry may have spent decades arguing over the least important part of the planning equation.

Because in the end, most people do not need more product access nearly as much as they need more clarity, confidence, coherence, and control over their own lives.

Perhaps the real future of planning is not independent advice.

Perhaps it is independent thinking.