There are 8.6 million UK adults who “need financial advice.”

That’s the headline.

But what if that diagnosis is wrong?

What if we’re not looking at an advice gap…

but a mislabelled system failure?

The uncomfortable truth

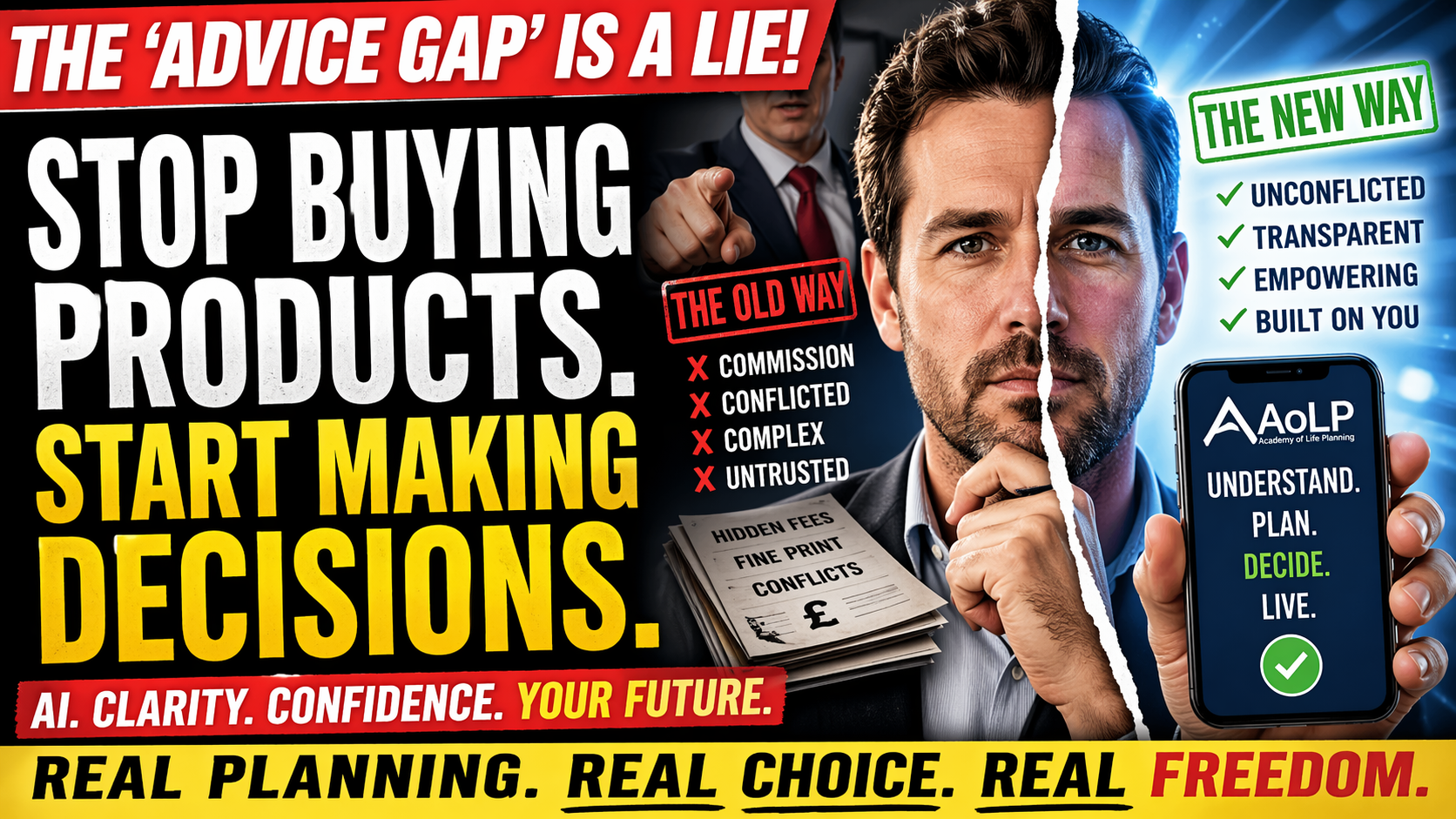

For decades, “financial advice” has often meant one thing in practice:

The distribution of financial products through intermediaries

That doesn’t make it inherently bad.

But it does mean we’ve blurred three very different things:

- Planning

- Advice

- Product sales

And when those are combined, something subtle—but important—happens:

The consumer is no longer the decision-maker.

They become the recipient of decisions.

The real gap

The industry says people lack access to advice.

But look more closely, and a different picture emerges.

Most people today already have:

- Access to information

- Access to products

- Access to tools

What they often lack is:

- Clarity — what actually matters in their life

- Confidence — to make decisions without deferring

- Structure — to connect choices into a coherent plan

That’s not an advice gap.

That’s a capability gap.

Why this matters now

Because AI has changed the game.

Not in the way it’s often described—but in a deeper way.

AI doesn’t just make advice more efficient.

It removes the need for someone else to interpret the system on your behalf.

For the first time, individuals can:

- Read complex documents in plain English

- Test scenarios instantly

- Ask unlimited questions without pressure or bias

- See how decisions connect across their whole life

This is not incremental change.

It is the collapse of information asymmetry.

The risk nobody is talking about

The current response is:

“Let’s scale advice using AI.”

But that carries a hidden danger.

If we simply replace:

- human intermediaries

with - algorithmic intermediaries

…we haven’t solved the problem.

We’ve just changed the interface.

Dependency remains.

Only the form changes.

The trust question

Trust in financial services has been fragile for years.

Not because individuals lack integrity—but because systems create pressure:

- Revenue linked to product

- Incentives tied to assets

- Complexity that obscures true cost and risk

Regulation has worked hard to improve outcomes.

But it operates within the same structural model.

So the question isn’t:

“Can we regulate advice better?”

It’s:

“What happens when people no longer need to rely on it in the same way?”

A different direction

What if the goal isn’t to scale advice…

…but to reduce dependence on it altogether?

That doesn’t mean removing support.

It means redefining it.

From advice → to agency

- Not “What should I do?”

- But “How do I decide well?”

From intermediation → to understanding

- Not “Trust me”

- But “Let me show you how this works”

From delivery → to capability

- Not “Here’s your plan”

- But “Here’s how to build and evolve your own”

Where this leads

In this emerging model:

- AI becomes a tool for thinking, not authority

- Humans become partners in judgement, not gatekeepers

- Planning becomes something you do, not something done to you

And something important happens:

The consumer regains their role as decision-maker.

So what is the real solution?

Not:

- More product access

- More automated recommendations

- More layers of delivery

But:

Better decision-making capability, supported by transparent tools and unconflicted guidance

That’s how we:

- reduce harm

- increase confidence

- and restore trust

A quiet shift is already happening

People are already:

- Asking AI before they ask advisers

- Reading documents before signing them

- Questioning recommendations more deeply

The direction of travel is clear.

The question is not whether this shift will happen.

It’s whether we design for it intentionally—or react to it defensively.

Final thought

The future of financial planning is not about replacing humans with machines.

And it’s not about scaling the old model with new technology.

It’s about something simpler—and more profound:

Helping people become capable of making their own decisions,

with the right support at the right time.

Not all the time.

Just when it’s needed.

If we get that right, we won’t just close an “advice gap.”

We’ll build something far more valuable:

a society that can plan, decide, and act with confidence.