In 2013, a Norfolk business owner walked into his bank with a concern.

He believed something was wrong inside his own company accounts—potential fraud, possibly involving a senior employee.

He expected support.

Instead, he says, the system turned against him.

What followed is a 12-year battle involving allegations of unauthorised payments, missing evidence, regulatory inaction, and the collapse of a once-thriving business.

The Core Allegation

At the centre of the case is a simple but serious question:

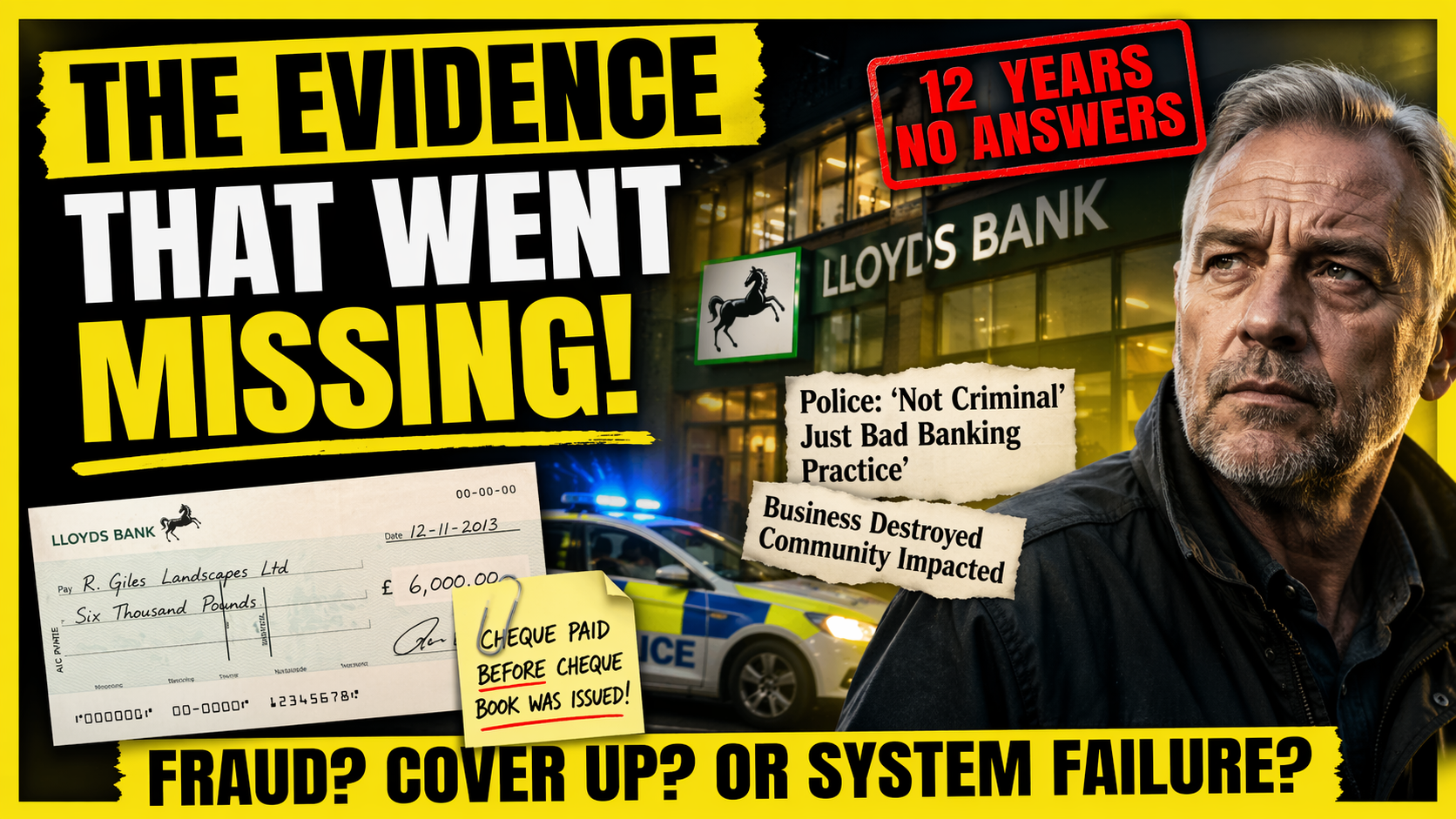

How were cheques paid from a business account before the cheque book had even been issued?

The claimant alleges:

- Payments were processed using cheque details not yet assigned to his account

- Key banking records contradict the bank’s position that all payments were “on mandate”

- Requests for clarification were blocked or limited

If proven, this would raise fundamental questions about:

- Banking controls

- Internal oversight

- Potential fraud or system failure

The Turning Point (2013)

On 27 November 2013, the business owner formally alerted Lloyds Bank to suspected irregularities.

According to his account:

- He expected the bank to investigate possible fraud

- Instead, the case was escalated internally to the Business Support Unit (BSU)

- The relationship with the bank deteriorated rapidly

Within eight months, his business collapsed.

He maintains that:

Earlier transparency or intervention could have changed the outcome.

The Evidence Dispute

A defining feature of the case is what happened next.

The claimant says he provided:

- Boxes of documents

- Digital files containing scanned evidence

- Records relating to multiple accounts and transactions

However:

- Police later stated only limited relevant material was received

- A USB device was allegedly returned wiped

- Some submitted files were not accounted for

The police position has remained consistent:

The matter does not meet the threshold for criminal investigation and is more appropriate for civil or regulatory routes.

Police and Regulatory Response

Norfolk Police reviewed the case multiple times.

Their conclusion:

- No criminal investigation would proceed

- The issues were classified as “bad banking practice”, not criminal conduct

The claimant challenged this through:

- The Independent Office for Police Conduct (IOPC)

- Political representatives

- Direct engagement with regulators

No formal investigation has been reopened.

A Wider Pattern?

The case does not exist in isolation.

The claimant has connected his experience to:

- The RBS GRG scandal, where businesses were mistreated by restructuring units

- The Post Office Horizon scandal, where faulty systems and missing data led to wrongful prosecutions

He has also engaged with campaigners and MPs raising concerns about:

- The balance of power between banks and SMEs

- The difficulty of pursuing accountability through official channels

While these parallels remain unproven, they raise a broader question:

Are existing systems equipped to investigate complex financial disputes involving major institutions?

Human and Community Impact

Before its collapse, the business:

- Supported local employment

- Delivered community projects

- Contributed to regional initiatives and events

Its failure had ripple effects:

- Loss of jobs

- Disruption to local supply chains

- Decline in community activity

Over time, some economic recovery has occurred in the area—but the original business was never restored.

The Unresolved Questions

More than a decade on, key issues remain unanswered:

- Were payments processed outside authorised mandate controls?

- What happened to the full body of submitted evidence?

- Were opportunities for early intervention missed?

- Should the case have met the threshold for criminal investigation?

Why This Matters Now

At a time when:

- Trust in financial institutions is under scrutiny

- Past scandals are still being revisited

- Technology and data integrity are central to accountability

Cases like this raise important questions about:

Transparency, evidence handling, and the real-world ability of individuals to challenge large institutions.

For the claimant, this is not just about financial loss.

It is about whether the system designed to protect individuals is capable of investigating itself when something goes wrong.

For further details visit: My Banking Fraud Allegations, by Roger Giles – Welney, Norfolk.

When the Evidence Feels Out of Reach: A Real Case and What You Can Do Next

Sometimes people come forward with a story that is hard to follow at first.

Not because it isn’t real.

But because it is too much, too fast, and too painful.

This is one of those cases.

A business owner raised concerns with his bank about unusual activity in his company accounts. He expected support. Instead, the situation escalated. His business later collapsed, and over time he came to believe that key evidence had been overlooked, misunderstood, or lost.

Whether every detail is proven or not is not the starting point here.

The starting point is this:

What do you do when something feels wrong, but the system doesn’t respond in the way you expected?

Why Cases Like This Become Overwhelming

When financial harm and stress combine, a pattern often emerges:

- You notice something that doesn’t make sense

- You try to get answers

- You are passed between organisations

- The language becomes technical or dismissive

- You start gathering more and more information

- Over time, everything becomes harder to explain clearly

At that point, even strong cases can lose traction.

Not because there is no substance.

But because:

The structure breaks down before the story is understood

What This Case Highlights

Without making legal conclusions, this situation raises three common challenges we see:

1. Complex financial evidence

Questions about transactions, mandates, or account activity can be difficult to explain without clear documentation and sequencing.

2. Different interpretations of the same facts

- One side may see potential wrongdoing

- Another may classify it as poor practice or a civil matter

Both positions can exist at the same time.

3. Evidence handling concerns

When people feel that documents are missing, incomplete, or not considered, it can create a deep sense of injustice and loss of trust.

A Calm Way Forward

If you recognise any part of this pattern in your own situation, the priority is not to push harder.

It is to slow things down and regain clarity.

Step 1: Stabilise your position

Before anything else:

- Take a pause from chasing multiple organisations

- Reduce exposure to distressing back-and-forth communication

- Focus on what you can control today

You don’t need to solve everything at once.

Step 2: Rebuild your evidence into a simple structure

Instead of large volumes of material, aim for:

- A timeline (what happened, in order)

- Key events only (5–10 maximum)

- Supporting documents linked to each event

For example:

- Date → What happened → What evidence supports this

Clarity is more powerful than volume.

Step 3: Separate facts from interpretation

This is one of the most important steps.

Try to distinguish between:

- What you know (documents, dates, actions)

- What you believe (interpretations or conclusions)

Both matter—but they serve different purposes.

Step 4: Understand the possible pathways

In situations like this, outcomes usually sit in one of three areas:

- Criminal (requires a high evidential threshold)

- Regulatory (focuses on standards and process)

- Civil (focuses on loss and remedy)

Knowing which path is realistic helps avoid unnecessary frustration.

Step 5: Protect your energy

Long-running cases can take a toll.

It is okay to:

- Step back

- Take breaks

- Focus on your wellbeing

Your recovery matters as much as the outcome.

A Wider Reflection

Cases like this often leave people asking:

- “Why wasn’t this taken further?”

- “Did anyone really look at the full picture?”

- “What could I have done differently?”

These are valid questions.

But they are also heavy ones.

At Get SAFE, we don’t try to answer everything at once.

We help you:

Regain clarity → organise what matters → and move forward safely

You Are Not Alone

If you are dealing with something similar:

- Confusion is normal

- Frustration is normal

- Feeling unheard is normal

What matters is what you do next.

And that doesn’t have to be rushed.

A Gentle Next Step

If you need support to:

- Organise your situation

- Make sense of what you have

- Understand your options

You can take a simple first step:

👉 Start by writing down your timeline. Just the key moments.

That alone can change everything.

If You’d Like to Help This Work Continue

Get SAFE exists because people choose to stand quietly alongside those facing financial harm.

There is no pressure to give.There is no “target thermometer.”There is no guilt-based appeal.

But if this story resonates with you — and you believe no one should have to face financial trauma alone — your support helps keep this work available to the next person who reaches out in panic, confusion, or despair.

Every £50 provides a bursary for one person to access:

• Trauma-informed recovery support

• Guided self-advocacy tools

• Evidence-structuring templates

• Life-stabilisation planning

• Fellowship peer support

• Secure testimony preservation

That support can mean the difference between someone breaking down in isolation — and someone finding clarity, steadiness, and dignity again.

If you’d like to contribute, you can do so here:

[Scan for the Support Get SAFE on Crowdfunder]

Whether you give, share, or simply hold this work in goodwill — thank you for being part of a more humane response to financial harm.

For further details visit: https://www.get-safe.org.uk/