A glossy career-change brochure can make a new life sound simple.

A clear pathway. Professional qualifications. Mentoring. Support. A respected brand. The chance to build a business. A route out of a career that no longer fits.

For someone feeling stuck, that can be powerful.

Especially if the message arrives at the right moment.

You may be tired of your current role. You may feel underused. You may want more meaning, more autonomy, more money, or more control over your working life. You may have reached the point where staying where you are feels more frightening than making a change.

That is exactly when due diligence matters most.

Because a career-change opportunity is not just a story.

It is a contract.

And the contract tells you what is really being transferred.

The brochure sells the opportunity. The contract allocates the risk.

There is nothing wrong with a financial adviser academy presenting an attractive career route. People need pathways into meaningful work. The financial planning profession needs capable, values-led people. Many career changers bring maturity, empathy, life experience, and commercial discipline that can be valuable to clients.

But the brochure and the contract do different jobs.

The brochure tells you what might be possible.

The contract tells you what you may be liable for.

The brochure may speak about support.

The contract may define repayment obligations, clawback, termination rights, restrictive covenants, ownership of client records, complaints charges, tax responsibilities, and post-exit restrictions.

The brochure may say you are becoming self-employed.

The contract may reveal whether that self-employment gives you genuine entrepreneurial freedom — or whether it mainly transfers financial and legal risk onto you while keeping commercial control elsewhere.

That distinction matters.

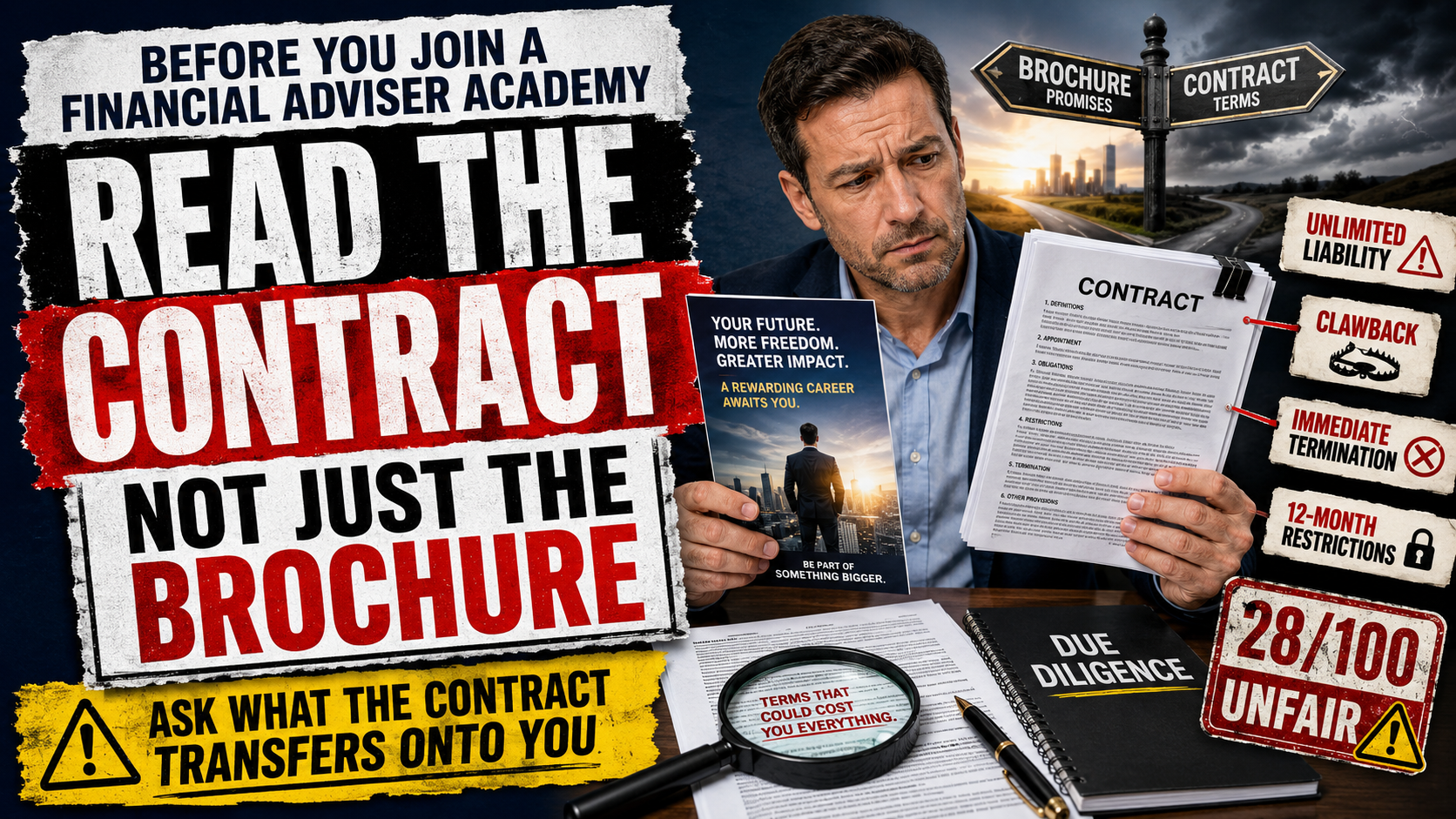

The public SJP adviser agreement raises serious due diligence questions

A publicly available adviser agreement, described as an agreement between an SJP Partner as “Appointor” and an individual “Adviser”, sets out a self-employed arrangement for introducing SJP business through the Appointor.

The exact current terms offered to any individual recruit may differ. Anyone considering the route should ask for the current adviser agreement, Letter of Appointment, SJP Handbook, remuneration schedule, clawback rules, complaint-cost rules, and exit provisions before relying on any external commentary.

But as a due-diligence exercise, the agreement is instructive.

When the contract text was analysed by The Leveller, it returned a score of 28/100 and categorised the agreement as “Unfair”. The Leveller identified a heavily imbalanced structure in favour of the Appointor, with extensive liability exposure, punitive clawback provisions, restrictive post-termination constraints, and immediate termination rights.

The central issue is not whether a person can build a successful career through such a route.

Some may.

The issue is whether they understand, before joining, what risks they may be accepting.

Self-employed does not automatically mean free

The agreement describes the adviser as self-employed, not an employee. On the face of it, that may sound attractive. Many career changers want independence. They want to build something of their own.

But self-employment can mean very different things depending on the contract.

In a genuinely entrepreneurial model, self-employment may mean autonomy, client ownership, pricing freedom, control over business direction, and the ability to build transferable value.

In a controlled distribution model, self-employment may mean something else. It may mean no employee protections, no holiday pay, no sick pay, no pension rights, responsibility for tax and expenses, exposure to business risk, and limited control over the rulebook.

So the right question is not simply:

“Will I be self-employed?”

The better question is:

“What kind of self-employment is this?”

Do I control the client relationship?

Do I own the business I am building?

Can I leave without being financially trapped?

Can I continue working in my profession if the relationship ends?

Are my liabilities capped?

Can I challenge termination or deductions?

Do I know all the documents that govern me?

If the answer to those questions is unclear, the career opportunity is unclear.

The first red flag: unlimited indemnity

One of the most serious issues identified in the agreement is the indemnity clause.

In plain English, an indemnity is a promise to reimburse another party for losses or liabilities.

The agreement includes wording requiring the adviser to indemnify and hold harmless the Appointor against all liabilities, costs, expenses, damages and losses arising from relevant breaches, claims, negligence, failure, or delay.

That is not a minor administrative clause.

That is a potential wealth-transfer clause.

If there is no clear cap, no proportionality test, no exclusion for indirect losses, and no fair process for determining responsibility, the adviser may be taking on very substantial downside risk.

A prospective adviser should ask:

Is my liability capped?

Does the indemnity cover only my proven wrongdoing?

Does it include loss of profit or reputational damage?

Who decides whether a loss has arisen?

Can sums be deducted before liability is independently established?

What professional indemnity insurance is required?

Who pays for it?

Does the insurance actually cover the indemnity I am being asked to give?

A career-change brochure is unlikely to answer these questions.

The contract might.

The second red flag: clawback that survives termination

Clawback is common in financial services. If initial remuneration is paid and the underlying business later unwinds, firms may seek recovery.

But the question is not whether clawback exists.

The question is how far it goes.

The agreement contains provisions allowing clawback to be deducted from the adviser’s financing account. It also states that clawback provisions may continue during the term of the agreement and after termination.

That is significant.

It means the adviser may not have finality over earnings already received. They may leave the arrangement and still face deductions or repayment demands linked to business written earlier.

A prospective adviser should ask:

What exactly can be clawed back?

For how long?

Is there a long-stop date?

Does clawback apply after I leave?

Can interest be charged?

Can it exceed the amount I originally received?

What happens if the client leaves for reasons outside my control?

Can deductions be made from future payments without agreement?

Is there an appeal or dispute process?

Without answers, the adviser may be entering a career path where income that looks earned is not truly secure.

The third red flag: immediate termination

The agreement also contains immediate termination rights in favour of the Appointor.

One clause allows termination where the Appointor determines, in absolute discretion, that the adviser has not complied with the SJP Handbook or other guidelines. Other triggers include regulatory investigation, insolvency concerns, reputational concerns, negligence, bad faith, repeated breaches, or failure to comply with regulatory obligations.

Some of these may be reasonable in principle.

Financial services is regulated. Firms need to protect clients, comply with rules, and act quickly where there is genuine misconduct.

But the due-diligence question is whether the clause includes objective criteria, procedural fairness, notice, an opportunity to respond, and an independent review process.

If not, the adviser may face sudden loss of income and business continuity without the protections normally associated with employment.

A prospective adviser should ask:

Who decides whether I have breached the Handbook?

Will I receive written reasons?

Will I have a chance to remedy minor breaches?

Is there an appeal process?

What happens to my pipeline business if I am terminated?

What happens to unpaid fees?

What happens to clients I introduced?

What happens to my debt or financing account?

Immediate termination is not just a legal mechanism.

It can be a life event.

The fourth red flag: post-termination restrictions

The agreement includes 12-month post-termination restrictions relating to clients and competing activity.

Again, restrictive covenants are not unusual in commercial contracts. Firms may have legitimate interests to protect.

But a career changer needs to understand the practical effect.

If you leave, can you continue earning a living in your chosen profession?

Can you advise people you introduced?

Can you contact clients who trusted you?

Can you work for another firm?

Can you start your own practice?

Can you use the relationships you built?

Can you move from restricted advice into a different planning model?

If the answer is “not easily”, then the academy route may not be a bridge to independence. It may be a route into economic dependency.

That may still be acceptable to some people.

But it should be known in advance.

The fifth red flag: the rulebook may sit outside the visible contract

Perhaps the most important due-diligence point is the document hierarchy.

The agreement states that, if there is a conflict between the agreement and the SJP Handbook or Letter of Appointment, the SJP Handbook and Letter of Appointment prevail.

That means the visible contract may not be the full contract.

A prospective adviser should not sign any agreement unless they have seen and understood all documents that bind them.

That includes:

The adviser agreement.

The Letter of Appointment.

The SJP Handbook.

The remuneration schedule.

The clawback rules.

The complaints cost provisions.

The financing account terms.

Any transition payment or advance terms.

Any restrictive covenant or exit provisions.

Any practice-specific agreement.

Any client ownership or data provisions.

Any professional indemnity requirements.

Any target, production, supervision, or conduct rules.

If another document overrides the agreement, you need that document before you can give informed consent.

Otherwise, you may be agreeing to a legal relationship you have not fully seen.

“Fully funded” does not mean free of risk

Recruitment material often emphasises that training is funded or supported.

That may be true.

But “fully funded training” is not the same as “risk-free career change”.

The real questions are wider.

Do I have to repay anything if I leave?

Are transition payments repayable?

Are advances repayable?

What happens if I do not hit production thresholds?

What happens if I need to pause for illness, caring responsibilities, bereavement, or family reasons?

What happens if the model does not suit me ethically or commercially?

What happens if clients do not arrive as expected?

What happens if I cannot convert enough prospects into business?

What happens if the economic conditions change?

Career-change decisions are not made in a spreadsheet alone. They are made inside real lives.

Mortgage payments. Children. Partners. Health. Confidence. Savings. Age. Energy. Reputation. Identity.

That is why the contract matters.

It shows what happens when things do not go to plan.

This is not a case for fear. It is a case for agency.

The answer is not to tell people never to join a financial adviser academy.

That would be too simple.

For some people, a structured academy may be the right route. They may value the brand, support, technical training, compliance infrastructure, and practice environment. They may understand the trade-offs and still decide the opportunity is worthwhile.

That is agency.

But agency requires a clear view of both promise and risk.

A person cannot make an informed decision if they only see the brochure.

They need the contract.

They need the rulebook.

They need the numbers.

They need the exit terms.

They need to know what happens if they succeed, and what happens if they do not.

Questions to ask before joining any financial adviser academy

Before joining any academy, ask these questions in writing.

What is the total cost of joining, qualifying, launching, and operating?

What financial support is available, and is any of it repayable?

What are the realistic first-year, second-year, and third-year earnings?

What percentage of academy entrants complete the programme?

What percentage are still active after one, three, and five years?

What client acquisition expectations apply?

Will I be expected to approach personal contacts?

Am I an employee, worker, self-employed contractor, appointed representative, or something else?

What legal protections do I lose because of that status?

Who owns the clients?

Who owns the client records?

What happens to clients if I leave?

What clawback applies, and for how long?

Are liabilities capped?

What indemnities am I giving?

What insurance must I hold?

Who pays complaint costs?

Can the firm deduct sums from money owed to me?

What restrictions apply after termination?

Can I continue working as a financial adviser elsewhere?

Can I build a genuinely transferable business?

Which documents override the agreement?

Can I take independent legal advice before signing?

A fair opportunity should survive fair questions.

Read the contract before you believe the story

Career change can be one of the most important decisions a person makes.

Done well, it can restore confidence, purpose, income, and direction.

Done badly, it can deepen dependency, increase debt, damage confidence, and leave people trapped in a model they did not fully understand.

So by all means read the brochure.

Attend the webinar.

Speak to the academy.

Take the quiz.

Explore the possibility.

But before you sign, read the contract.

Not just the headline terms.

Not just the friendly summary.

Not just the recruitment promise.

Read the clauses that explain liability, repayment, clawback, termination, client ownership, restrictions, deductions, and document hierarchy.

That is where the real story sits.

Before entering any financial adviser academy, ask not only what the opportunity promises, but what the contract transfers onto you.

The right career path should not depend on learned helplessness.

It should build learned agency.

And learned agency begins with knowing what you are agreeing to.

Before you sign any adviser agreement, run it through The Leveller™. Available now on the iOS App Store and coming soon to Google Play, The Leveller helps you spot hidden risks, unfair terms, and clauses that may transfer more risk onto you than the brochure suggests. In this case, the warning is clear: do not sign this agreement without major amendments. The combination of unlimited liability, immediate termination rights, and extensive post-termination restrictions creates an extremely risky arrangement. Seek legal advice to negotiate liability caps, fair termination procedures, and reduced restrictive covenants. Consider carefully whether the financial opportunity justifies the substantial legal and financial risks. The current terms appear heavily skewed against the adviser’s interests and raise serious questions of fair dealing.

The Leveller™ is an educational tool. It does not provide legal or financial advice. All outputs are used at your discretion. Visit get-safe.org.uk — Get SAFE, Support After Financial Exploitation.

“The Leveller is pure genius. I used it on complex financial documents and terms and conditions — the kind of deliberate small print most people do not bother to read. In seconds, it provided a red-flag analysis and highlighted the questions I should ask before signing. It is a brilliant product and a genuine game changer. The best £4.99 I’ve ever spent.”

— John Galajsza, Director, John Galajsza Limited