Why agency before advice is becoming a consumer protection necessity

A financial firm can disappear.

The harm it caused often does not.

That is the uncomfortable lesson emerging from recent analysis of Financial Ombudsman Service complaints and the wider enforcement record across UK financial services. Complaints are still being upheld against firms that are no longer trading. Some have gone into administration. Some are in liquidation. Some have dissolved. Yet the consequences of their conduct remain alive in the lives of consumers.

[Source: FT Advioser Fos complaints still being upheld years after companies went under, 11 June 2026]

This matters because financial harm rarely ends when the transaction ends. A poor pension transfer, an unsuitable investment, a hidden commission arrangement, a failed insurance process, a negligent lending decision, or a defective advice chain may not fully reveal itself for years. By the time the consumer understands what happened, the firm may have changed name, merged, failed, disappeared, or passed the problem into the redress system.

The firm exits.

The consumer remains.

The paperwork remains.

The consequences remain.

The anxiety remains.

And often, the burden of proving what happened shifts to the very person who was least equipped to understand the risk at the point of sale.

The long tail of financial harm

Financial services often presents itself as a system of regulated trust. Consumers are encouraged to rely on authorised firms, professional advisers, product providers, platforms, lenders, insurers, brokers, and complaint schemes.

But trust becomes fragile when harm is only recognised years later.

The consumer may have acted in good faith. They may have signed what they were told to sign, relied on what they were told was suitable, accepted what they were told was standard practice, and paid charges they did not fully understand. Years later, they may discover that the decision was flawed, the advice was conflicted, the charges were excessive, the disclosure was inadequate, or the product was never aligned with their real needs.

That is not simply a technical problem.

It is an agency problem.

Agency means the person’s ability to understand, question, pause, compare, document, and decide without being made dependent on someone else’s authority. Where agency is weak, the consumer is not genuinely participating in the decision. They are being processed through it.

The traditional answer has been advice.

But advice, when delivered within structurally conflicted or product-led systems, does not always restore agency. Sometimes it replaces the consumer’s judgement with professional authority. Sometimes it makes the consumer more dependent, not less. Sometimes it gives the appearance of protection while leaving the person unable to explain, challenge, or evidence what happened later.

That is why the Academy of Life Planning argues for a different starting point.

Not advice first.

Agency first.

Recidivism in financial services

The word recidivism is usually used in criminal justice. It means reoffending: a pattern where someone who has offended before offends again.

Applied carefully to financial services, it does not mean every firm, adviser, or professional is acting badly. It means the enforcement record shows repeated patterns of violation across the sector. The same types of misconduct recur. The same categories of consumer harm recur. The same institutional failure modes recur.

Violation Tracker UK provides an important window into this pattern. It records enforcement actions across UK regulators and shows financial services as one of the most heavily penalised sectors. The data includes repeated cases involving major financial institutions, alongside many smaller firms whose misconduct may be less visible but no less damaging to the people affected.

This matters because public mistrust is often treated as irrational.

It may not be.

In many cases, mistrust may be a rational response to lived experience, enforcement history, and repeated institutional failure.

The phrase “bad apples” is no longer sufficient where the pattern is systemic. If harm appears repeatedly across firms, products, advice chains, complaint routes, and regulatory cycles, the problem is not merely individual conduct. It is architecture.

A structurally untrustworthy system does not require everyone within it to behave badly. It only requires incentives, complexity, opacity, dependency, and weak accountability to combine in ways that repeatedly expose consumers to harm.

That is what makes recidivism such an important concept.

It shifts attention from isolated events to repeating patterns.

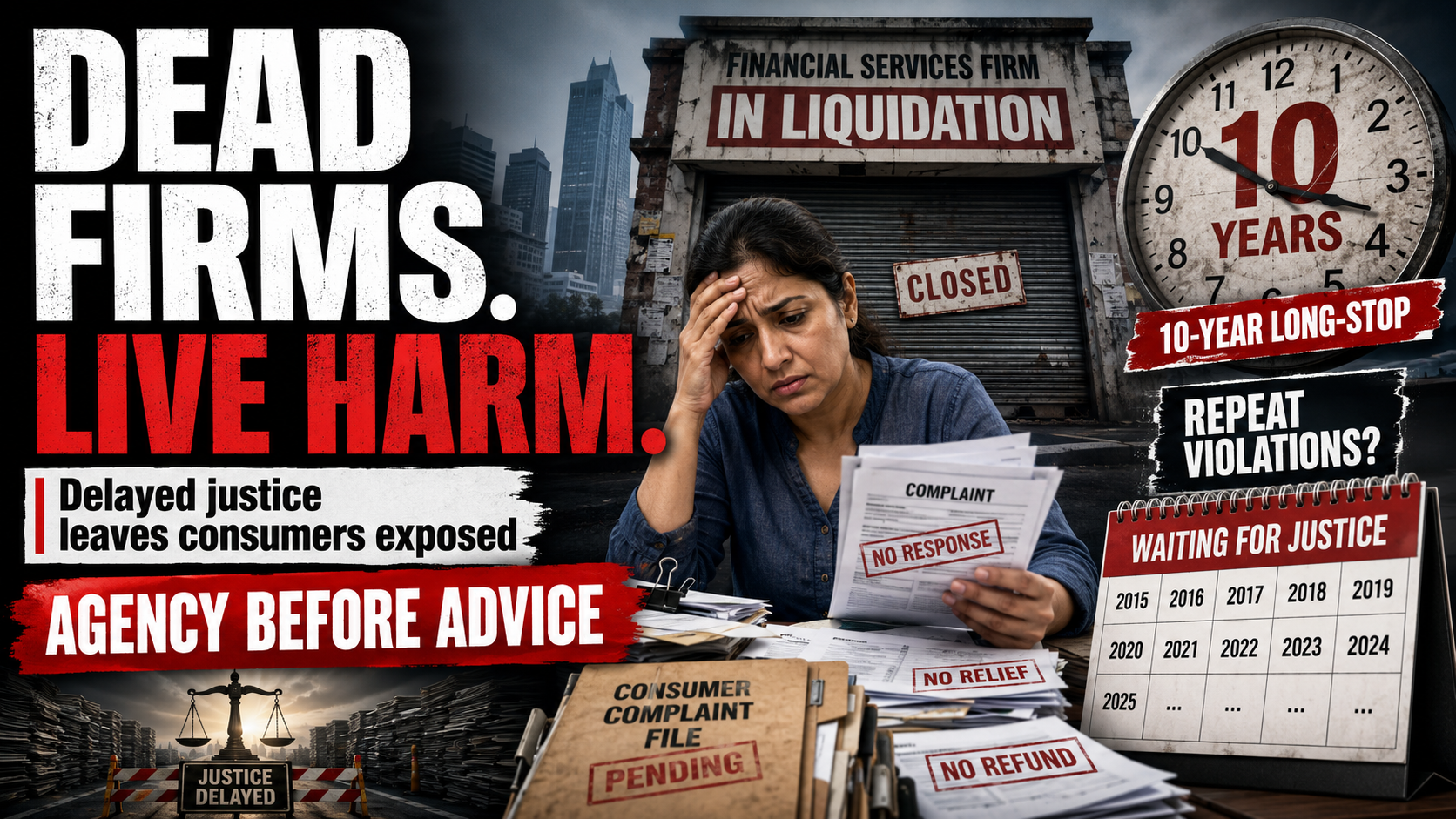

Dead firms, live harm

When complaints are upheld against firms that no longer trade, the weakness of after-the-event redress becomes obvious.

A consumer may win the argument but still face delay.

They may receive an Ombudsman decision but then need to pursue compensation elsewhere.

They may discover that the responsible firm has no remaining practical capacity to compensate them.

They may be passed to the Financial Services Compensation Scheme, where eligibility, limits, evidence, and process create further hurdles.

This is not a criticism of individual people working within redress bodies. Many are trying to resolve difficult cases in a complex environment.

The deeper issue is that redress comes late.

Too late for the person who lost a pension.

Too late for the family who lost security.

Too late for the widow trying to reconstruct financial decisions after bereavement.

Too late for the small business owner who acted on unsuitable guidance.

Too late for the consumer whose complaint depends on documents that no longer exist.

A redress system can compensate.

It cannot give back lost years.

It cannot fully restore peace of mind.

It cannot reverse the stress, shame, conflict, illness, or family breakdown that financial harm may cause.

This is why prevention and agency matter so much.

The 10-year long-stop changes the risk equation

The proposed 10-year long-stop for Financial Ombudsman Service complaints makes this issue more urgent.

At present, complaints are generally subject to a six-year rule, with a further three-year window from when the consumer became aware, or ought reasonably to have become aware, that they had cause to complain. That recognition point matters because many forms of financial harm are latent. They are not obvious at the time.

A pension transfer may look acceptable for years.

An investment may appear to be underperforming for reasons that seem normal.

A mortgage or credit arrangement may only reveal its full cost over time.

A commission structure may remain hidden.

A long-term product may only show its unsuitability when life changes.

A vulnerable consumer may not realise they were exploited until someone helps them reconstruct the events.

A hard 10-year long-stop changes the balance. It risks turning delay itself into a consumer risk. Once the clock expires, the issue may become procedurally dead even if the harm is still very much alive.

The policy argument for a long-stop is certainty. Firms want finality. Evidence degrades. Records disappear. Historic liabilities are difficult to manage. Complaint systems can become overloaded.

Those concerns are not trivial.

But they must be weighed against the lived reality of financial harm. The people least able to detect misconduct early are often the people most likely to be harmed by an absolute time limit. Complexity protects the system before it protects the consumer.

That is why the long-stop is not merely a technical reform.

It is a shift in risk.

It moves more responsibility onto consumers to understand, document, and challenge financial decisions earlier. If consumers do not know what to look for, or are discouraged from questioning professional authority, they may lose access to redress before they even understand that something went wrong.

In a sector with documented recidivist tendencies, that makes agency before advice not just desirable, but protective.

Redress after damage is not enough

The financial services sector often talks about consumer protection as if it begins with regulation and ends with redress.

But for the person affected, that is too narrow.

True protection must begin before the point of harm.

It begins when people know what questions to ask.

It begins when they understand the difference between guidance, advice, sales, intermediation, and genuine planning.

It begins when they can identify conflicts of interest.

It begins when they keep records.

It begins when they understand what they are signing.

It begins when they can pause before committing.

It begins when they can use AI and structured tools as a second brain, not to replace judgement, but to strengthen it.

It begins when the person is treated not as a passive consumer, but as the primary authority in their own life.

That is the purpose of agency restoration.

The goal is not to make everyone an expert in pensions, investments, insurance, mortgages, tax, law, or regulation. That would be unrealistic and unfair.

The goal is to make people less dependent on experts before they surrender authority.

A person does not need to know everything to ask better questions.

They do not need to become a financial adviser to recognise when something feels unclear.

They do not need to master regulation to keep good records.

They do not need to be combative to pause, reflect, compare, and seek a second view.

They do not need to reject advice.

They need enough agency to engage with advice safely.

Advice out. Agency in.

The Academy of Life Planning’s position is not anti-advice. It is anti-dependency.

There will always be situations where regulated financial advice is necessary, valuable, and appropriate. Complex pensions, tax, estate planning, long-term care, investment risk, protection needs, and regulated transactions may all require specialist expertise.

But the person should not disappear inside the process.

The test of good support is not whether the consumer complies with the adviser’s recommendation. It is whether the person becomes clearer, safer, more confident, and more capable of making sense of their own life and choices.

That is the distinction between advice and agency.

Advice tells.

Agency equips.

Advice may solve a transaction.

Agency strengthens the person.

Advice can be useful.

Agency is foundational.

If the industry’s enforcement record shows repeated violation, and the complaint system may soon impose a harder long-stop, the public need more than reassurance. They need capability.

They need tools that help them read documents.

They need systems that help them organise evidence.

They need plain-English explanations.

They need structured decision support.

They need confidence to question authority without feeling foolish.

They need support before they are in crisis, not only after the damage is done.

The future of consumer protection is capability

The old consumer protection model assumed that regulated firms, professional advice, disclosure documents, complaint systems, and compensation schemes would be enough.

Experience suggests otherwise.

A system that repeatedly produces harm, then asks consumers to complain years later, is not fully protective. It is reactive. It waits for the injury and then asks the injured person to prove the wound.

That may be necessary.

It is not sufficient.

The future must include personal capability, AI-assisted understanding, transparent records, independent planning tools, and a culture in which ordinary people are encouraged to think, question, and decide for themselves.

This is where Total Wealth Planning becomes more than a planning method.

It becomes a consumer protection philosophy.

Plan life before money.

Understand the person before the product.

Understand the product before signing.

Restore agency before advice.

Use technology to strengthen judgement, not replace it.

Make expertise progressively less necessary, not more.

The aim is not to abandon redress. Redress remains vital. But redress should be the safety net, not the operating model.

When dead firms leave live harm, delayed justice becomes part of the injury.

When delay itself becomes a procedural risk, people need the means to act earlier.

And when a sector shows repeated patterns of violation, the public should not be asked simply to trust harder.

They should be helped to stand stronger.

Dead firms. Live harm. Delayed justice.

This is why we need agency before advice, not redress after damage.