There is a quiet assumption shaping much of modern financial regulation:

If institutions behave better, outcomes will improve.

It’s a reasonable assumption. But it is incomplete—and increasingly insufficient.

Because while institutional development has advanced—more rules, more oversight, more compliance infrastructure—the lived experience on the ground tells a different story:

- Harm continues

- Redress remains partial

- And the gap between the two persists

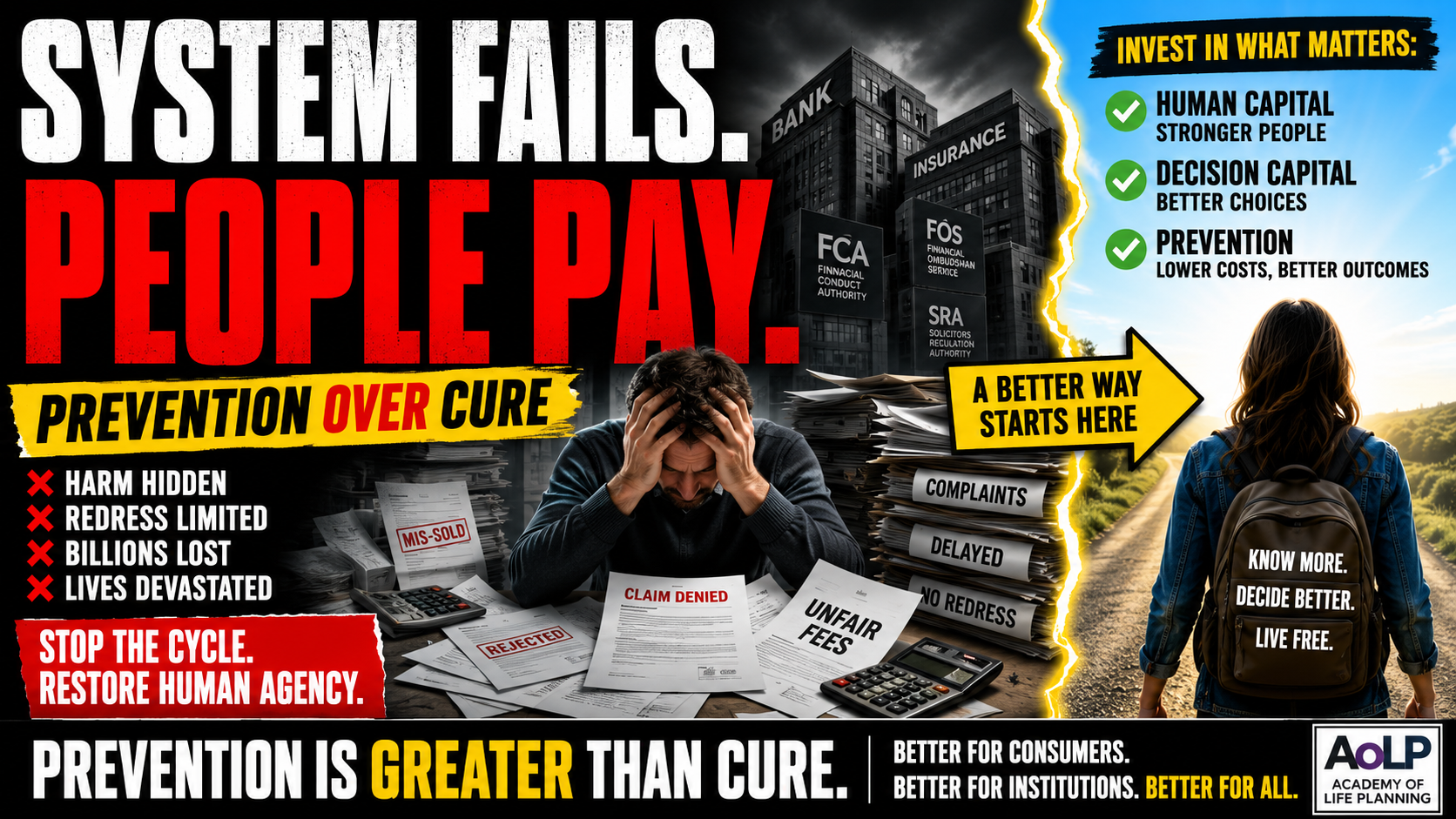

We are investing heavily in the system.

But underinvesting in the individual.

The structural imbalance

Today’s model is weighted toward institutional control:

- More regulatory frameworks from bodies like the Financial Conduct Authority

- Expanded dispute resolution through the Financial Ombudsman Service

- Oversight of legal and claims activity via the Solicitors Regulation Authority

Each layer is designed to correct problems after they emerge.

But this creates a system that is:

- Reactive rather than preventive

- Complex rather than accessible

- Dependent rather than empowering

And crucially:

It assumes the individual remains a passive participant.

The missing layer: human capital and decision capital

If we step back, most financial harm does not begin with misconduct.

It begins earlier—with decisions made under:

- incomplete understanding

- asymmetry of information

- time pressure or emotional stress

This is where human capital and decision capital come in.

- Human capital: the individual’s capacity to think, act, earn, and adapt

- Decision capital: the ability to make informed, structured choices over time

These are not abstract ideas. They are practical capabilities.

And right now, they are underdeveloped relative to the complexity of the system people are expected to navigate.

The cost of underinvestment

When human and decision capital are weak, the system compensates by expanding:

- Claims management companies and legal services step in after harm

- Regulatory bodies scale oversight and enforcement

- Institutions absorb fines and redress costs

- Consumers absorb stress, delay, and often irreversible loss

This creates a cycle:

Weak agency → poor decisions → harm → claims → regulation → cost → repeat

Even when it works, it is expensive.

When it fails, it is devastating.

And in most cases, it only addresses a fraction of the original harm.

A different starting point: prevention through agency

What if we inverted the model?

Instead of asking:

“How do we fix harm after it happens?”

We ask:

“How do we reduce the likelihood and impact of harm before it crystallises?”

This is where restoring human agency becomes practical, not philosophical.

In simple terms, it means equipping individuals to:

- understand what they are entering into

- test decisions before committing

- navigate complexity with structure and clarity

- recognise risk early, not retrospectively

The AoLP approach: before, during, after

The Academy of Life Planning has been developing this as a layered approach:

Before harm

- Improve understanding of contracts, incentives, and trade-offs

- Reduce information asymmetry at the point of decision

During decision-making

- Provide structured planning tools to test scenarios and consequences

- Strengthen clarity, control, and confidence

After harm

- Stabilise individuals

- Organise information and evidence

- Support clear, grounded next steps without dependency

The intention is not to replace regulation or redress.

It is to reduce unnecessary reliance on them.

Why this benefits everyone

A system built on stronger individual agency does not weaken institutions.

It strengthens the entire ecosystem.

For consumers:

- fewer harmful decisions

- greater confidence and independence

- reduced need for reactive support

For institutions:

- lower redress costs

- fewer complaints and disputes

- improved trust and long-term relationships

For regulators:

- reduced enforcement burden

- more targeted intervention

- lower systemic friction

In short:

Prevention reduces cost, complexity, and conflict across the system.

From institutional optimisation to human development

We are approaching the limits of what institutional optimisation alone can achieve.

More rules will not fully solve a capability gap.

More enforcement will not eliminate poor decisions made under pressure or confusion.

The next phase of development is not just better systems.

It is better-equipped individuals within those systems.

A shift in investment

If we accept that prevention is greater than cure, then the implication is clear:

We need to rebalance investment toward:

- human capital development

- decision capability

- accessible planning infrastructure

Not as a replacement for regulation—but as its foundation.

A simple reflection

If the majority of financial harm begins before a complaint is ever made…

Where should the majority of our effort sit?

The answer may shape the next generation of financial planning—not as advice, not as intervention, but as restored human agency at scale.

Curious how others see this.