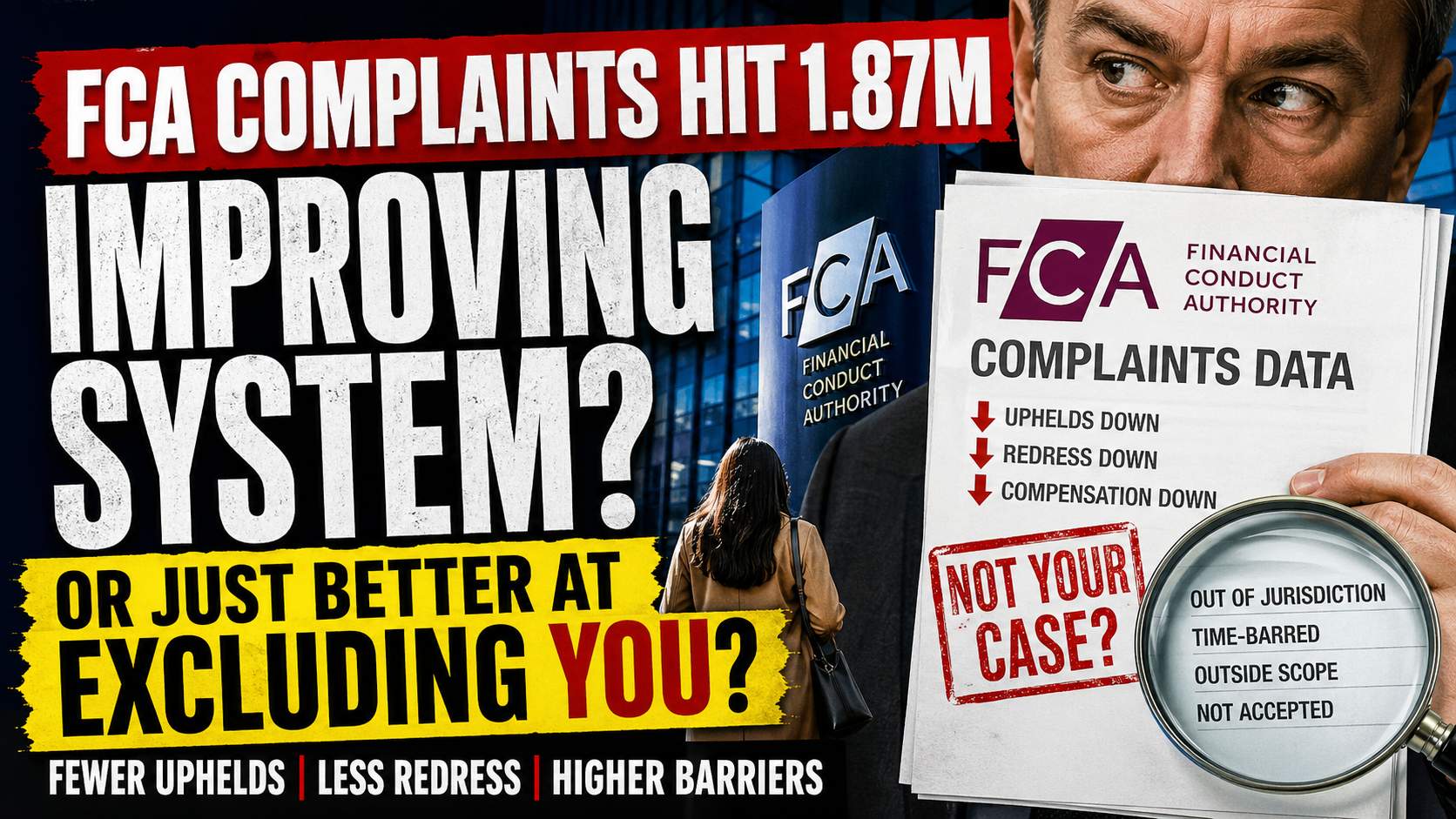

The latest complaints data from the Financial Conduct Authority presents a superficially reassuring picture. Complaint volumes remain broadly stable at 1.87 million. The proportion of complaints upheld has declined. Total redress has fallen. Average compensation per case is lower.

Taken together, these figures might suggest a system gradually improving—firms resolving issues earlier, fewer serious failings occurring, and better overall consumer outcomes.

But this interpretation deserves scrutiny.

Because when placed in context, the data may reveal less about improving conduct—and more about a system undergoing structural change in how complaints are filtered, assessed, and resolved.

The illusion of stability

At first glance, stability in complaint volumes over several years appears encouraging. Yet stability alone tells us little about underlying fairness.

Complaints data is not a neutral reflection of harm. It is a reflection of:

- who feels able to complain

- who persists through the process

- which cases are accepted into the system

- and how those cases are interpreted

If any of these variables shift, the data shifts with them—regardless of whether consumer outcomes have improved.

From rules to interpretation

One of the most significant changes in recent years has been the shift from rules-based regulation toward a more principles-based framework.

In theory, this allows for flexibility and better judgement. In practice, it introduces greater subjectivity into complaint handling.

Large institutions, supported by legal teams and compliance infrastructure, are structurally better equipped to operate in environments where interpretation matters. Individuals are not.

The result is subtle but important:

A decline in upheld complaints may not indicate fewer valid complaints.

It may indicate a higher threshold for what is accepted as valid.

Friction in access to redress

The introduction of fees for legally supported complaints at the Financial Ombudsman Service has added a further layer of complexity.

While framed as a measure to manage process efficiency, the practical effect is to discourage professional support—particularly in complex or high-value cases.

This creates a filtering mechanism:

- simpler cases proceed

- more complex cases are delayed, diluted, or abandoned

Those most in need of support—individuals facing sophisticated financial harm—are often the least equipped to proceed without it.

The system does not need to reject these cases explicitly. It only needs to make them harder to pursue.

The quiet impact of jurisdiction

Another under-examined factor is the growing proportion of complaints deemed:

- out of jurisdiction

- outside time limits

- beyond regulatory perimeter

Each of these outcomes removes a complaint from formal consideration.

Yet these exclusions are rarely foregrounded in headline data.

If more complaints are being filtered out before substantive assessment, then:

- uphold rates fall

- redress totals fall

- and the system appears to be improving

But what is actually improving is the system’s ability to exclude.

Redress in retreat

The decline in total redress—from over £283 million to approximately £236 million—alongside a reduction in average compensation raises further questions.

In isolation, this could suggest fewer severe cases.

In context, it may reflect something else entirely:

- tighter interpretations of loss

- more conservative redress methodologies

- regulatory positioning that aligns more closely with institutional sustainability than individual restitution

Recent approaches to large-scale issues, such as motor finance disputes, indicate a growing tendency toward controlled, system-wide outcomes rather than expansive consumer compensation.

This is not necessarily unjust—but it is not neutral.

The asymmetry at the heart of the system

At its core, the complaints landscape remains defined by a fundamental imbalance.

Institutions:

- control data

- understand process

- shape narrative

Individuals:

- lack access to information

- struggle to articulate technical arguments

- operate under stress and uncertainty

This is an information asymmetry problem, not merely a conduct problem.

And until that asymmetry is addressed, complaints data will continue to reflect capability gaps as much as it reflects fairness.

The AI inflection point

This is where the current moment becomes particularly significant.

We are entering a transitional phase—one in which artificial intelligence has not yet fully rebalanced the system, but soon will.

AI has the potential to:

- analyse contracts and disclosures in seconds

- identify inconsistencies and regulatory breaches

- structure coherent, evidence-based complaints

- quantify potential redress outcomes

In effect, it equips individuals with capabilities previously reserved for institutions.

When this shift takes hold, several outcomes become likely:

- more complaints, not fewer

- higher-quality submissions

- increased escalation of complex cases

- more consistent challenge to institutional positions

At that point, complaints data may begin to look very different.

A system not yet levelled

It would be premature to interpret current trends as evidence of a system delivering better outcomes for consumers.

What we are observing is a system that has become:

- more selective in what it admits

- more interpretive in how it judges

- more controlled in how it compensates

In short, more efficient—but not necessarily more just.

The role of the Total Wealth Planner

For the emerging Total Wealth Planner, this moment matters.

Because the future of financial planning is not simply about better products or more efficient advice. It is about restoring Decision Capital to the individual.

That means:

- helping people understand the systems they operate within

- equipping them with tools to navigate complexity

- supporting them in moments of stress, change, and dispute

- and, increasingly, enabling them to use AI as a “second brain” on their side of the table

The complaints landscape is not separate from financial planning. It is a downstream consequence of how financial decisions are made, structured, and supported.

The real question

So the question is not:

Why are complaints falling in value and uphold rate?

The more important question is:

What conditions are shaping what gets counted—and what gets left out?

Until that question is addressed, any narrative of improvement should be treated with caution.

Because a system that appears to be working better may simply be working differently.

Curious how others see this.