Steve Conley

There is a quiet shift underway in UK financial services.

After years of constraint following the Global Financial Crisis, banks are moving back toward wealth management—re-entering a space they were once forced to retreat from.

But they are not coming back as they were.

They are returning:

- with more advanced technology

- with more refined data segmentation

- and increasingly, with less friction in how they engage customers

To the consumer, it may feel like progress.

More access.

More support.

More “guidance.”

But it is worth pausing to ask a more important question:

What is driving this renewed interest in your financial life?

The Trigger Is Not Your Plan — It’s Your Balance

In most bank-led wealth propositions, engagement does not begin with your goals.

It begins with your profile.

A typical trigger might look like this:

- £50,000–£150,000+ held in cash

- Stable income

- Age aligned with “investment suitability”

- Low current product penetration

At that point, the system does not see a person.

It sees:

an under-optimised asset.

From there, the journey is structured.

You may be invited to:

- review your “underperforming cash”

- explore “investment opportunities”

- speak to an adviser or use a digital planning tool

All of which sounds reasonable.

Until you understand the underlying dynamic:

This is not a neutral planning conversation.

It is a commercially triggered engagement.

What the Data Shows — Not Just the Narrative

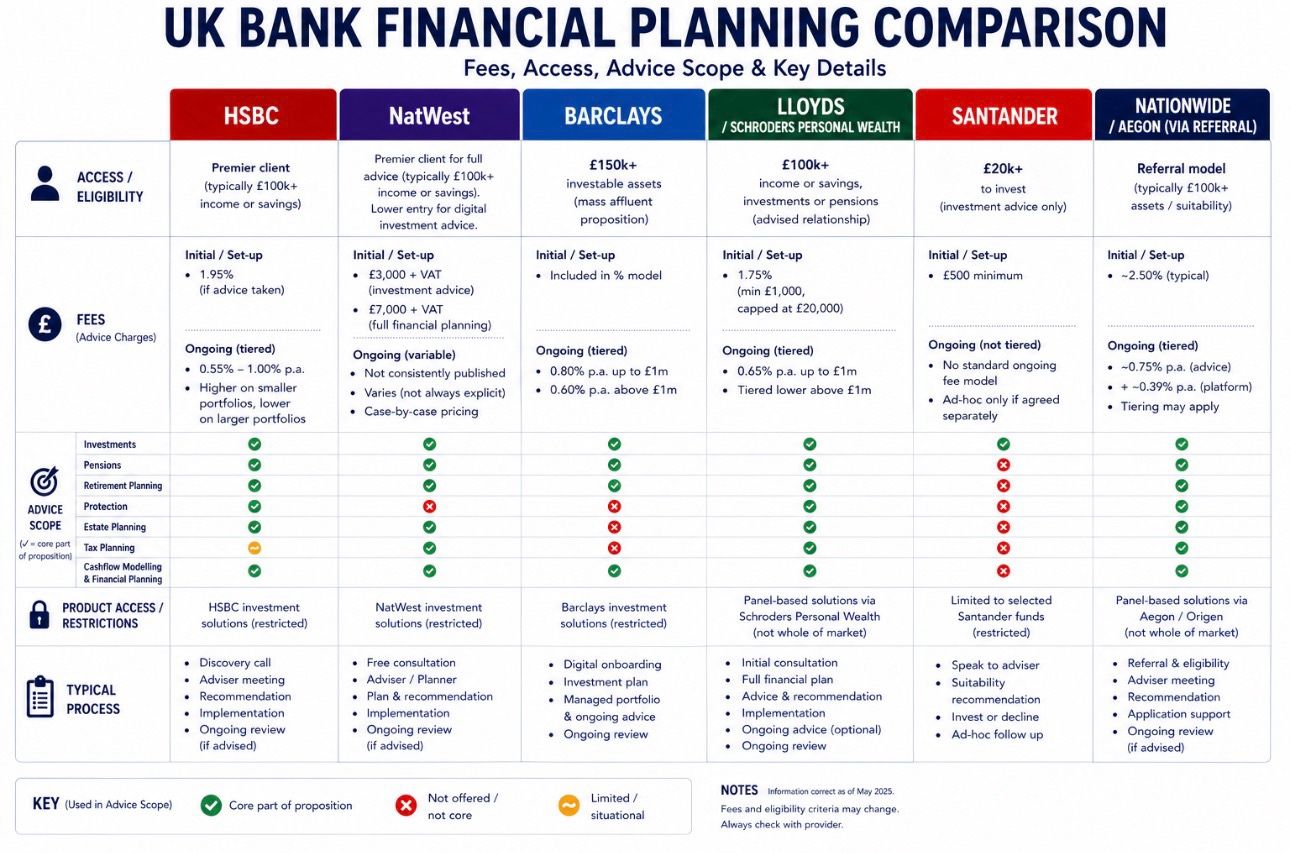

Using The Leveller™, a contract intelligence tool developed under Get SAFE, we analysed the current UK bank wealth propositions.

The findings are consistent—and concerning.

At a structural level, these models:

- Gate access behind £100k–£150k+ thresholds

- Layer multiple fees (advice, platform, product)

- Restrict product choice to in-house or panel solutions

- Limit planning scope in key areas like tax and protection

The conclusion is not subtle:

“Bank financial planning services… favour institutional interests.”

And critically:

“These bank models prioritise institutional profits over consumer outcomes.”

From Cash to Capital: The Quiet Reframing

The narrative presented to consumers is simple:

Cash is losing value.

Investing is the solution.

There is truth in that statement.

But it is incomplete.

What is often missing is context:

- why cash exists (liquidity, resilience, optionality)

- how risk behaves in real life

- what happens during market downturns

- how behaviour—not just returns—drives outcomes

Instead, the journey is designed toward a predictable outcome:

movement from lower-margin holdings (cash) to higher-margin solutions (investments).

Framed as suitability.

Delivered as guidance.

But economically:

it is asset migration.

The Hidden Layer: Cost Complexity

One of the most significant findings from The Leveller is not just the level of fees—but how they are structured.

- Initial advice fees can reach £7,000+

- Ongoing costs sit around 0.5%–1.0% annually

- Additional platform and fund charges apply

But more importantly:

“Multiple fee structures obscure true costs… not always explicit.”

This creates a situation where:

consumers cannot easily see what they are paying—

or what they are giving up over time.

And over decades, that matters.

Because the real cost is not the fee you see today.

It is the lifetime extraction from your capital.

Restricted Choice — By Design

Another consistent pattern:

“All providers limit access to own investment solutions.”

This is not incidental.

It is structural.

It means:

- recommendations are shaped within a controlled environment

- alternatives may not be presented

- “best” is defined within a restricted universe

Which raises a fundamental question:

Can advice be fully aligned if choice is pre-limited?

This Is Not Financial Planning

True financial planning begins with:

- your life

- your goals

- your constraints

- your preferences

And only then considers:

- whether investing is appropriate

- how much

- in what form

- and at what cost

What many bank propositions offer instead is:

a pathway to product—with planning wrapped around it.

What You Should Do Before You Proceed

This is not about avoiding your bank.

It is about engaging with clarity and control.

Before acting:

1. Run the Terms Through The Leveller

Understand:

- what you’re being offered

- what’s not being said

- where the risks and restrictions sit

2. Ask the Questions That Matter

The Leveller highlights five critical ones:

- What are the total costs, including platform and fund charges?

- Am I restricted to your products?

- What happens if my balance falls below thresholds?

- How are you paid?

- Can I leave without penalty?

3. Separate Thinking From Product

The key decision is not:

“What should I invest in?”

It is:

“Why am I being encouraged to invest—and does it serve my life?”

4. Explore Direct Routes to Investment

In many cases, similar outcomes can be achieved via:

- direct-to-consumer platforms

- lower-cost structures

- unbundled decision-making

Without:

- layered distribution costs

- or embedded commercial bias

Final Thought

Banks are not doing anything unusual.

They are doing what they are designed to do:

- grow assets

- increase revenue

- improve client retention

But you need to understand:

their incentives are not the same as your outcomes.

So when the invitation comes—

and it will—

pause.

Because once you see the system clearly, the question changes.

It is no longer:

“Should I invest?”

It becomes:

“Who benefits most from this decision—and is that aligned with me?”