By Steve Conley

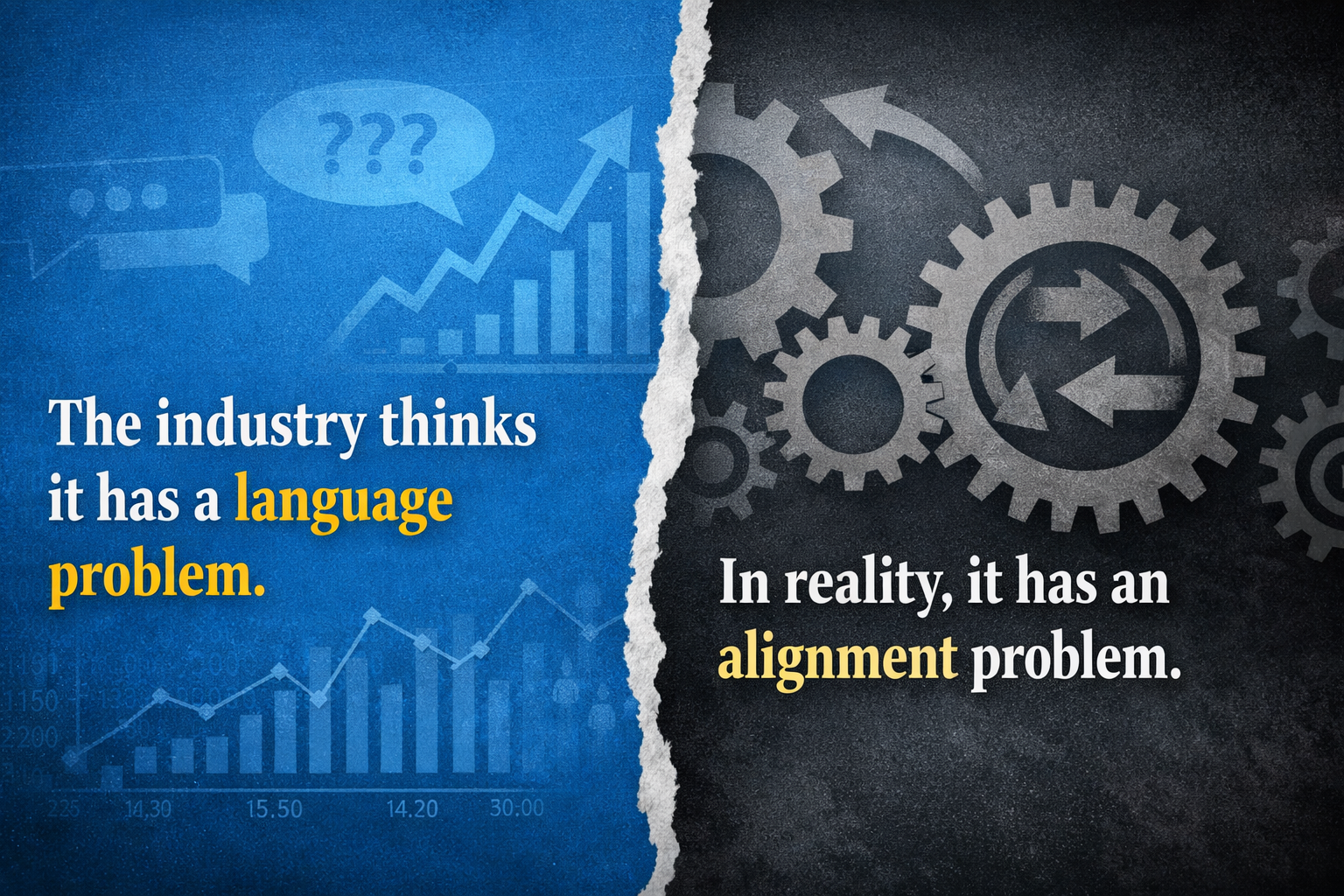

Recent research from Oxford Risk and NextWealth has drawn attention to a growing unease among retirement clients. The conclusion is clear enough: the language advisers use—phrases intended to reassure, guide, or inform—is too often doing the opposite. It is creating anxiety, eroding trust, and disengaging the very people it is meant to support.

On the surface, this appears to be a communication problem. Advisers are encouraged to adjust tone, refine phrasing, and better sequence their messaging—placing financial security before growth, and growth before flexibility. Words like “steadier” are preferred to “steady”. “We help you” lands better than “it’s important to invest”.

All sensible. All useful.

But not sufficient.

Because what this research reveals—perhaps unintentionally—is something deeper. The issue is not simply how advisers speak. It is why they are speaking in this way in the first place.

A Symptom Mistaken for the Cause

When clients react negatively to phrases such as “you’re not locked in” or “higher risk”, it is easy to assume the wording is at fault. That the solution lies in softer language, better framing, or more emotionally intelligent delivery.

Yet clients are not responding to words in isolation. They are responding to what those words represent.

A conversation that begins with products—however carefully explained—carries a different emotional weight from one that begins with a person’s life. Clients feel this instinctively. They may not articulate it in technical terms, but they recognise when a discussion is leading somewhere predefined rather than emerging from their own circumstances.

The discomfort is not linguistic. It is structural.

Advisers are often trained within a system that is built around solutions first and understanding second. Compliance frameworks reinforce this. Product architectures depend on it. Revenue models frequently rely upon it.

In such an environment, language becomes performative. It is required to soften, translate, and humanise a process that is not, at its core, designed around the individual.

No amount of refinement can fully resolve that tension.

The Limits of Better Communication

The industry has, for decades, invested heavily in improving communication skills. Relationship-building workshops, behavioural finance insights, and client engagement frameworks have all contributed to more thoughtful interactions.

And yet, the findings of this latest research suggest that mistrust persists.

This should prompt a more fundamental question.

If advisers are communicating more carefully than ever before, why do clients still feel misunderstood?

The answer may lie in the distinction between explaining a solution and co-creating a plan.

In the former, the adviser’s role is to guide the client toward an outcome, however well-intentioned. In the latter, the outcome emerges from the client’s own goals, constraints, and evolving life context.

One requires better language.

The other requires a different starting point.

Planning Before Product

At the Academy of Life Planning, we have long argued that financial planning must begin not with investments, but with the individual.

This is not a semantic shift. It is a structural one.

A planning-led conversation starts with questions such as:

- What does your life look like over the next decade?

- What matters most to you now—and what might change?

- Where are the points of uncertainty, pressure, or transition?

Only once these are understood do financial strategies enter the discussion. And even then, they are framed as tools in service of a broader life architecture, not as ends in themselves.

In this context, communication changes naturally.

There is no need to reassure a client that they are “not locked in” if they have been involved in shaping the plan from the outset. Flexibility is implicit. Ownership is shared.

There is no need to carefully reframe “risk” if the client understands the trade-offs within the context of their own goals. The language becomes grounded in their reality, not abstract market concepts.

When the starting point is human, the language follows.

Trust Is an Outcome, Not a Technique

One of the most important insights from the research is that communication is not a “soft extra” in retirement planning. It is integral to outcomes.

This is correct.

But it is worth extending the idea further.

Trust is not built through communication techniques alone. It is the by-product of alignment—between what the client needs, what the adviser is incentivised to deliver, and how the process unfolds.

Where that alignment exists, trust tends to emerge organically.

Where it does not, even the most carefully crafted language can feel hollow.

This is why some of the strongest client relationships are often found among advisers who operate outside heavily product-driven environments. They are not necessarily better communicators in a technical sense. They are working within structures that allow for genuine client-first engagement.

The language reflects that freedom.

A Bridge, Not a Rejection

It would be a mistake to dismiss the findings of Oxford Risk and NextWealth. On the contrary, they provide valuable evidence of how clients experience financial advice in practice. They highlight nuances of tone, sequencing, and emotional response that should not be ignored.

For many advisers, improving communication will lead to better outcomes in the short term. It may reduce anxiety, increase engagement, and strengthen relationships.

But there is also an opportunity here to go further.

Rather than asking, “How can we say this better?”, the industry might ask, “Why are we saying this at all?”

That question opens the door to a different model—one where advice is not something delivered to clients, but something developed with them.

The Future of Advice

As artificial intelligence continues to reshape the financial landscape, the role of the adviser is already evolving. Information is no longer scarce. Technical explanations are no longer a differentiator. Clients can model scenarios, compare options, and access guidance at unprecedented speed.

In this environment, the value of advice shifts.

It moves away from product selection and toward life integration. Away from transactions and toward transformation. Away from persuasion and toward partnership.

This is where trust is rebuilt—not through better wording, but through a clearer alignment of purpose.

The research has identified a problem that many clients feel but struggle to articulate. It has shown that language matters, that tone matters, and that sequencing matters.

All true.

But the deeper insight is this:

When advice starts with products, it needs better words.

When it starts with people, it needs fewer of them.

That is not a communication strategy.

It is a different way of thinking about the role of financial planning itself.

And it is here that the next chapter of the profession will be written.