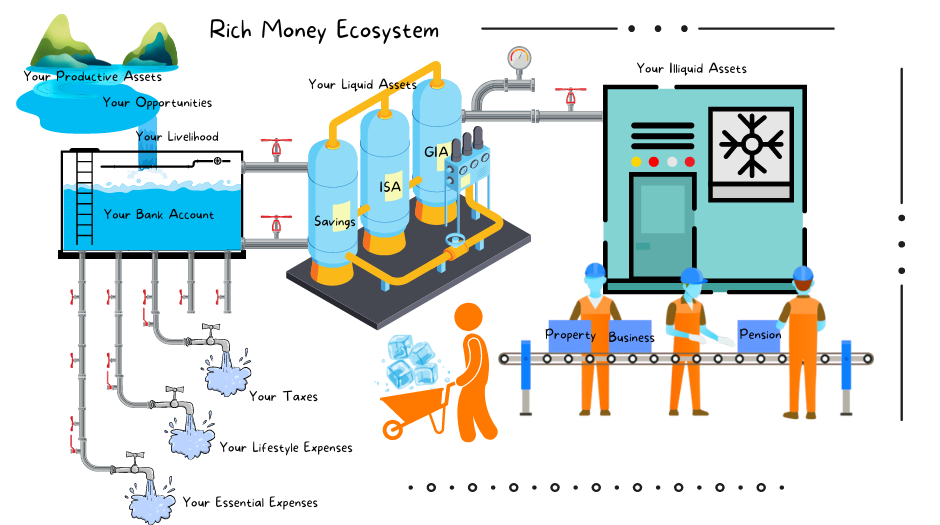

The truth is, financial service industry propositions are designed for rich people. In a rich people money ecosystem, the bucket is overflowing, the expenditure taps are full on, the financial asset well is full, and the frozen asset freezer is stocked to the hilt. Firms offer to run the well for a handsome fee that, when expressed as a percentage, looks very small indeed, or the freezer or the production line.

In reality, though, that’s not how it is for most people.

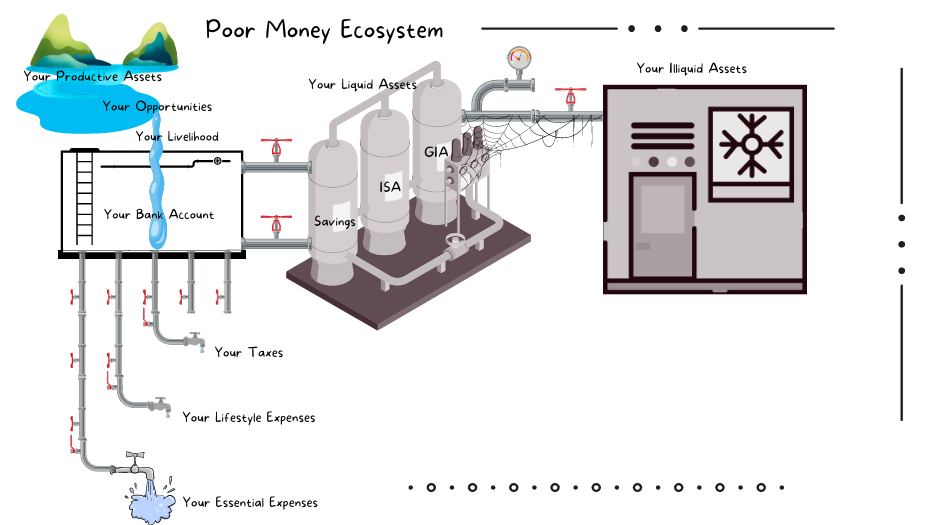

Most people have a trickling stream for a sustainable livelihood. The reservoir tank is empty. They live from pay cheque to pay cheque, funding essential expenditures only. They have little or no savings. They own little.

The commercial reality is poor people can’t afford rich people’s propositions. And firms can’t afford to serve poor communities. FCA, there is no business in offering simple savings products to this market; there is nothing in the tank to be saved. Diverting income streams to savings plunges customers into difficult essential expenditure choices, such as heating or eating.

DWP and pension providers, raising auto-enrolment contribution rates, and dropping age or income thresholds will not cut it. The poor people’s money ecosystem has nothing for your cups and buckets.

The issue is livelihood.

The livelihood needs to be fast flowing and sustainable for a lifetime.

The problems are getting worse. We see more dried-out ecosystems than ever before. Yes, the rich are getting richer, and market averages disguise that the poor are getting poorer. Loss of defined benefit occupational pension schemes, struggles to get on the property ladder, student debt, dwindling adviser populations, and advice focus on the rich. The underserved are scratching for info on the internet or down the pub. The wealth gap is widening.

The United Nations and London Business School show us how to manage poor people’s ecosystems.

United Nations say to eradicate poverty identify productive assets, leverage entrepreneurial opportunities, and create sustainable livelihoods.

LBS define productive assets to create livelihoods. They add two further asset classes: vitality assets to extend the lifetime and transformational assets to sustain livelihood.

The financial planner determines the required outflows to support the customer’s favourite future and fill reservoirs and freezers. The output is a lifetime liability forecast. The financial planner then plans to create a sustainable livelihood for a lifetime.

For this, we use an Ikigai proposition development framework:

Entrepreneurial opportunity = What you’re good at (productive assets) + love to do + world needs + will pay for!

We optimise it by creating a firm of endearment; evidence suggests that such firms double in value relative to market peers every three years.

We make livelihood sustainable by making income streams passive or creating work that doesn’t feel like work and from which our clients never wish to retire. An excellent solution for unpensioned masses that pleases DWP and the Treasury!!!

We drop our asset strategies, and the income and asset value they produce, into a lifetime asset forecast. Combined with the liability forecast, this determines a lifetime cash flow forecast and a plan to achieve your favourite future.

Remember, for the average Brit, like tech firms, market-book ratios near 50. What we mean by that is that the economic value we place on productive, vitality, and transformational assets (the reservoir feeding the system) is 98% of the whole ecosystem of the client. And according to ONS, regulated investments are 5% of tangible assets.

If you are in the business of distributing or manufacturing the 0.1% of the money ecosystem, your financial plan can’t just be about which particular product to put the 0.1% in. This is mind-blowing, given everything experts have told you your entire life. Here’s the thing, for whole ecosystem planning, your choice is irrelevant. On the whole ecosystem lifetime cash flow forecast, your decision doesn’t register on the gauge!

Also, the average Brit with nothing in the tank isn’t going to pay the fee you’re asking for.

And FCA, consumers won’t pay £100 to £200 for advice on the 0.1% they haven’t got!

Because whole-ecosystem financial planning is generic (without opinion on particular investments), the benefits are:

- We financially activate the client to make their own decisions on particular investment choices – more informed clients result in better outcomes. We do this with low-cost end-user financial planning apps and financial education content libraries.

- We offer a value ladder – a choice of:

- One-to-one/ done for you (from £2,950 – £4,950)

- One-to-many/ done with you (from £295 – £495)

- None-to-one/ done by you (from £0 – £49)

- People can be on-board for free and move up and down the ladder. So avoiding lazy income traps and meeting consumer duty obligations.

- Each channel is equally profitable for the firm.

- Fintech works seamlessly across the value ladder.

- Margins are better without nonsensical regulatory costs.

- The business model is entirely scalable without headcount limitations.

If you want a future-ready whole-ecosystem financial planning business in a box, ready to go, with all the licenses, training, tools, peer group support network, and anything else you can think of to run a business on a day-to-day basis… at exceptionally low cost. We have that no-brainer just for you.

We could even have you up and running by Summer 2023, just before that Consumer Duty deadline! Count to 5 and do it! Contact steve.conley@aolp.co.uk today.

For more information visit The Academy of Life Planning.

One thought on “The Harsh Reality: The Financial Industry’s Blindness to the Non-Rich Majority”