The consumer revolution is forcing advisory firms to re-evaluate their business models, and the prospect of increasing the threshold levels for new and existing clients is being actively considered. However, the urgent need to serve the underserved and comprehend the unmet requirements of our target demographic is of paramount importance. The crucial priority for this group is the elevation of sustainable livelihoods over extended periods to create adequate lifetime cash flow. It is a common misconception amongst distributors and manufacturers that the solution lies in promoting savings, which is an erroneous notion, as people without wealth cannot save wealth. The question that begs attention is: how can we identify and serve the needs of the underserved, and what advanced technological solutions and innovative business models can assist us in our endeavour?

Impact of Consumer Duty Regulations

Under the UK Financial Conduct Authority’s (FCA) Consumer Duty regulations, financial firms must conduct a value-price assessment (VPA) to ensure that their products and services provide value for their customers. The VPA involves assessing the price that the customer pays for a product or service against the value that they receive from it. The assessment should consider the customer’s needs, preferences, and circumstances and whether any alternative products or services would better meet the customer’s needs.

The VPA aims to ensure financial firms provide their customers with products and services that represent good value for money and meet their needs rather than simply maximising their profits. By carrying out a VPA, financial firms can demonstrate that they are fulfilling their obligations under the Consumer Duty and putting their customers’ interests first. The FCA has stated that the VPA should be an ongoing process and that firms should regularly review their products and services to ensure they continue providing value for their customers.

As a result of the recently implemented VPA, advisory firms are contemplating the possibility of increasing the “investable asset” thresholds required for the onboarding of new clients, as well as the continuation of services for their existing clientele.

Lessons from down under

In Australia, changes to how financial advisers are paid for their services have unintended consequences for lower-income clients. In 2013, the Australian government banned financial advisers from deducting their fees from “wrap platforms,” which are investment products that allow customers to hold and manage various investments in one place. This change was intended to increase transparency and make it easier for customers to understand their fees.

However, the change had the unintended consequence of making it less profitable for financial advisers to serve lower-income clients. Instead, many financial advisers have focused on serving wealthier clients willing and able to pay for their services directly rather than using wrap platforms. This shift has left lower-income clients without access to affordable financial advice, which can be a barrier to building wealth and achieving financial security.

The Australian government has recognised this issue and is considering ways to address it. One proposal is to introduce a “scaled advice” model, which would allow financial advisers to provide more targeted advice to clients based on their specific needs rather than providing a full suite of services that may be unaffordable for some clients. The government is also considering ways to improve the accessibility and affordability of financial advice for all Australians, including technology and other innovative solutions.

Overall, the changes to how financial advisers are paid in Australia have highlighted the importance of ensuring everyone can access affordable and high-quality financial advice, regardless of their income or wealth.

Here in the UK, the VPA has a similar impact. Many regulated advisers are looking to target ultra-high net worth post-July 2023.

What impact will VPA have on access to financial planning?

Based on the Wealth and Asset Survey conducted by the Office for National Statistics covering the period of April 2018 to March 2020, it has been determined that a substantial 83% of households possessed a net financial wealth of less than £100,000. This trend was more pronounced among the demographic groups of Generations X, Y, and Z.

In the UK, the investable asset thresholds for financial advisers can vary depending on the firm or individual adviser. However, as a general guideline, many financial advisers typically require a minimum investable asset threshold of £50,000 to £100,000 to take on a new client. This criterion is because financial advisers often charge a percentage-based fee on the assets they manage. Providing their services to clients with lower levels of investable assets may not be cost-effective.

However, some financial advisers may be willing to work with clients with lower levels of investable assets if they can pay a fixed fee or provide other financial planning services, such as budgeting, debt management, or retirement planning.

It is important to note that the investable asset threshold is not the only factor financial advisers consider when taking on new clients. They also consider the client’s financial goals, risk tolerance, and overall financial situation to determine whether they are a good fit for their services.

If the thresholds are raised significantly, the proportion of underserved communities is anticipated to surge, encompassing between 95% and 99% of the population. In such a scenario, firms will be challenged to devise a strategy to deal with unwanted clients.

Will robo-advice plug the gap?

Some online investment platforms and robo-advisers can provide investment advice and portfolio management for clients with lower levels of investable assets, often with lower fees than traditional financial advisers.

While robo-advisers have become increasingly popular in the UK in recent years, they still represent a relatively small proportion of the overall investment market. According to a report by the FCA, published in 2020, the total assets under management (AUM) held by robo-advisers in the UK were around £3.5 billion at the end of 2019. This figure represented less than 1% of the total AUM for the UK investment management industry, which was around £7.7 trillion at the same time.

However, the FCA report also noted that the robo-adviser market in the UK has been snowballing, with a 55% increase in AUM between 2018 and 2019. The report also found that robo-advisers were serving a growing number of clients, with around 2.2 million clients using robo-adviser platforms in 2019.

It is also worth noting that the use of robo-advisers varies depending on the type of investor. While robo-advisers may be more popular among younger investors or those just starting to invest, they may be less popular among established or high-net-worth investors who prefer more personalised and hands-on investment management.

Despite the modest presence of robo-advisers in the UK investment market, this segment is gradually expanding. It is anticipated to continue to do so in the foreseeable future. Until such time, however, the vast majority of underserved individuals are left with little option but to rely on informal, unsophisticated sources of advice such as pub talk or the Internet.

Will FCA plans to relax distribution rules help?

To increase access to financial products and services for consumers with limited financial capability or who are financially excluded, the FCA has proposed to relax some rules around selling simple investment products to the mass market.

Under the proposals, firms could sell certain investment products, such as stocks and shares ISAs, to customers without providing detailed information about the risks associated with the products. The FCA believes this will make it easier for consumers to access these products, particularly those with limited financial knowledge or who may be put off by complex or technical information.

However, the FCA has stressed that the proposed changes will only apply to specific investment products deemed “non-complex” and have a lower risk profile. In addition, firms will still be required to provide basic information about the products, such as their charges and the benefits of investing. They must ensure that the products suit the customers they are selling to.

The FCA has also proposed introducing a new category of investment products, known as “simple investment products,” which would be subject to even less regulation and designed specifically for consumers with limited financial capability or who are financially excluded. These products would be required to meet specific standards, such as offering a clear and transparent pricing structure and having a simple and easy-to-understand investment strategy.

Overall, the FCA’s proposals to relax rules for selling simple investment products to the mass market aim to increase access to financial products and services for underserved or excluded consumers. However, the FCA has also emphasised that consumer protection remains a top priority. The proposed changes will be subject to ongoing scrutiny and review to ensure they achieve their intended outcomes.

Lower-income clients need to build wealth and achieve financial security.

A vital issue with robo-advisers and the new regulations imposed by the FCA is that they tend to prioritise the sale of financial products. However, for the 83% of households in the UK with a net financial wealth of less than £100,000, the more pressing need is to acquire additional wealth rather than simply safeguarding existing wealth. While products are helpful for the preservation of wealth, they do not serve as a means of generating wealth in the first instance, which is fundamentally driven by the actions and decisions of individuals themselves.

Low-income customers have distinct requirements that necessitate a different and tailored approach to financial planning.

Unstainable livelihoods and living from pay cheque to pay cheque.

The proportion of the UK population living from pay cheque to pay cheque can vary depending on the source and definition.

One study by the FCA published in 2021 found that around 14.2 million adults in the UK, or 26% of the adult population, showed one or more signs of potential vulnerability in their financial situation, which could include living from pay cheque to pay cheque. The FCA’s definition of financial vulnerability includes individuals with low financial resilience, high levels of debt, or limited savings or investments.

Another study by the UK’s Money Advice Service, published in 2018, found that around 40% of UK adults have less than £100 in savings, which could indicate that they are living from pay cheque to pay cheque. This study defined living from pay cheque to pay cheque as having no or only enough savings to cover living expenses for one month.

Overall, while the exact proportion of the UK population living from pay cheque to pay cheque may vary depending on the definition used, it is clear that a significant proportion of the population may be vulnerable to financial hardship or unexpected expenses. This position underscores the importance of financial education and access to affordable financial products and services to help individuals build their financial resilience and improve their overall financial well-being.

Easing regulations to facilitate the sale of more financial products to those with lower incomes may undermine their ability to manage their daily living expenses. In this regard, a financial tool is required to assist in coping with such challenges rather than just dispensing advice. In other words, we require a robocop instead of a robo-adviser.

How can financial plans create wealth?

The United Nations provides the answer to sustainable development goal number one, to end world poverty:

“Priority actions on poverty eradication include improving access to sustainable livelihoods, entrepreneurial opportunities and productive resources.”

The democratic financial plan must identify productive assets, leverage entrepreneurial opportunities, and create sustainable livelihoods.

The London Business School (LBS) defines productive assets as assets that generate income or revenue for their owner or user. These assets include physical assets, such as machinery or property, and intangible assets, such as intellectual property, mailing lists, or brands.

The LBS definition highlights the importance of productive assets in generating economic growth and increasing overall prosperity. Individuals or companies can generate income, create jobs, and contribute to developing their local or national economy by investing in productive assets.

Overall, the LBS definition of productive assets emphasises these assets’ role in driving economic growth and prosperity and underscores the importance of investing in assets that generate sustainable, long-term returns.

Additional intangible asset classes with investment potential.

In addition to productive assets, the LBS identifies two other assets that can be important for long-term economic growth: vitality and transformational.

Vitality assets support the overall health and well-being of a society or community. These include education, healthcare, and social infrastructure, such as parks or community centres. According to the LBS, investing in vitality assets can positively impact the productivity and overall well-being of a society or community, as they can help create a more skilled and healthy workforce and contribute to a community’s social cohesion and resilience.

Transformational assets, on the other hand, are assets that have the potential to fundamentally change or disrupt the way that a society or industry operates. These can include new technologies, such as artificial intelligence or blockchain, or new business models, such as the sharing economy. According to the LBS, investing in transformational assets can be risky. Still, it can also offer significant rewards for those who can successfully navigate and adapt to the changes they bring about.

Overall, the LBS definition of vitality and transformational assets highlights the importance of investing in productive assets and the underlying infrastructure, institutions, and innovations supporting long-term economic growth and prosperity. By investing in all three types of assets, individuals, companies, and governments can help to create a more dynamic, resilient, and prosperous society.

Developing financial plans incorporating all three types of intangible assets can help individuals create sustainable livelihoods over extended periods while mitigating financial risk.

Comparison with the Ikigai Framework.

The LBS asset classifications and the Ikigai framework are both models that can help individuals and organisations think about how they allocate their resources and make decisions about their investments.

The LBS asset classifications focus on three types of assets: productive assets, vitality assets, and transformational assets. These classifications highlight the importance of investing in assets that generate income or revenue, support the overall health and well-being of a society or community, and have the potential to disrupt or transform the way that a society or industry operates.

The Ikigai framework, on the other hand, is a model that helps individuals identify their life purpose by exploring the intersection of four different areas: what they love, what they are good at, what the world needs, and what they can be paid for. The framework encourages individuals to balance their passions, skills, societal needs, and financial sustainability to find meaningful work and live a fulfilling life.

While the LBS asset classifications and the Ikigai framework are both resource allocation and decision-making models, they focus on different areas and use different criteria. The LBS asset classifications primarily focus on economic development and growth, while the Ikigai framework focuses on personal fulfilment and purpose.

However, there are some similarities between the two models. Both models emphasise the importance of finding a balance between different factors, whether it is different types of assets in the case of LBS or different areas of personal passion and societal need in the case of Ikigai. In addition, both models suggest that individuals and organisations must consider multiple factors and find a balance that works for them to succeed and be fulfilled.

Comparison with the 4 Ps Framework.

The 4 Ps framework, the quadruple bottom line, is a model for measuring and evaluating business performance based on four key areas: people, planet, profit, and purpose. This framework is designed to help businesses take a more comprehensive and holistic approach to their operations and recognise that success and sustainability are not just about financial performance but also social and environmental impact.

The four Ps in the framework are defined as follows:

- People: This refers to the social impact of a business and its relationship with its employees, customers, and the broader community. It includes factors such as employee well-being, labour standards, diversity and inclusion, customer satisfaction, and community engagement.

- Planet: This refers to the environmental impact of a business and its operations, including factors such as carbon footprint, energy and resource use, waste and pollution, and ecosystem health.

- Profit: This refers to the financial performance of a business, including factors such as revenue, profit margin, return on investment and shareholder value.

- Purpose: This refers to a business’s broader mission and values beyond just financial performance. It includes ethical and responsible business practices, social and environmental stewardship, and commitment to long-term sustainability.

By considering all four of these areas, the 4 Ps framework encourages businesses to take a more comprehensive and long-term view of their operations and recognise that success is not just about financial performance but also social and environmental impact. The framework can also help businesses identify areas where they may need to improve their performance or align with their values and mission. Overall, the 4 Ps framework is a useful tool for businesses committed to sustainability, responsibility, and positively impacting their stakeholders and the world.

One similarity between the 4 Ps framework and the Ikigai framework is that they both emphasise the importance of finding a balance between different factors, whether it is different types of business performance in the case of the 4 Ps framework or different areas of personal passion and societal need in the case of the Ikigai framework.

Another similarity is that both frameworks take a holistic approach to their subject matter. The 4 Ps framework emphasises the importance of considering all four key areas of business performance. In contrast, the Ikigai framework emphasises the importance of balancing different aspects of personal fulfilment.

Firms of Endearment Study

The “Firms of Endearment” (FoE) study is a research initiative that aims to identify companies that prioritise stakeholder well-being and societal impact in addition to financial performance, in other words they adopt a 4 P framework. The study identifies companies with a higher purpose beyond just making profits and prioritising the needs of all their stakeholders, including employees, customers, suppliers, and the wider community. The study suggests that these companies not only perform well financially but also create value for their stakeholders and positively impact society.

The principles of the FoE study are based on the acronym “SPICE”, which stands for:

- Stakeholder integration: These companies prioritise the needs and well-being of all their stakeholders and seek to create value for everyone, not just their shareholders.

- Purpose-driven: These companies have a higher purpose beyond just making profits and are motivated by a desire to positively impact society.

- Conscious leadership: These companies are led by leaders who prioritise the well-being of their employees, customers, and the wider community, and who lead with empathy, compassion, and a strong sense of purpose.

- Employee engagement: These companies have high levels of employee engagement and seek to create a culture of empowerment, autonomy, and meaning for their employees.

The FoE study suggests that companies that prioritise these principles and prioritise the well-being of all their stakeholders can outperform companies that focus solely on financial performance. According to the study, companies identified as FoEs outperformed the S&P 500 index by a factor of 14 from 1996 to 2011. The FoEs outperforming the market by 2% per month, effectively doubles the firm’s market value every three years relative to its peers.

The FoE study suggests that companies prioritising stakeholder well-being and societal impact can create strong relationships with their stakeholders, build trust and loyalty, and foster a culture of innovation and purpose. This strategy, in turn, can lead to long-term sustainable growth and financial success.

When financial planning, the FoE study highlights the importance of prioritising emotional well-being and societal impact in addition to financial performance and suggests that people that do so can achieve both financial success and positive impact on society.

Financial planning approaches to shifting active income to passive sources.

Top of Form

Approaches to shifting Strategies to move income from active to passive refer to ways individuals or organisations can shift their income streams. Active income is earned through work or labour, such as wages, salaries, or self-employment. In contrast, passive income is earned through investments, rental income, or other sources that require little to no ongoing effort or work.

One common strategy for moving income from active to passive is to invest in income-producing assets, such as dividend-paying stocks, bonds, or property. Individuals or organisations can earn regular income by investing in these assets without actively working for it. This strategy can help create a more stable and predictable income stream and provide long-term growth and wealth accumulation opportunities.

Another strategy for moving income from active to passive is to create and monetise productive assets, such as intellectual property, patents, trademarks, or copyrights. Individuals or organisations can earn passive income without actively working for it by creating and licensing these productive assets.

In addition to these strategies, other ways to move income from active to passive may include creating and selling digital products, such as e-books or online courses, or participating in affiliate marketing programs.

Overall, strategies to move income from active to passive are designed to help individuals or organisations create more stable and predictable income streams while providing opportunities for long-term growth and wealth accumulation. Individuals and organisations can achieve greater financial stability, flexibility, and freedom by diversifying their income sources and investing in passive income-generating assets.

One such strategy is for individuals to change their economic activity from being an employee to becoming an investor:

- Employees: You don’t own the job. You can’t sell your job. The income generated is shared with your employer. Next step, self-employed.

- Self-employed: You own your job. You retain profits. Still your business has no market value. Next step, business owner.

- Business owner: You hire people to work for you. You earn from your employee’s activity. You create recurring revenue. Your business has a market value. Next step, investor.

- Investor: You hire people to run your business, step back and enjoy the passive revenue.

Consider a scenario where an individual creates a sustainable source of income, derived from work that feels rewarding and fulfilling, or via a passive revenue stream. This income continues uninterrupted into their retirement years, effectively covering any potential shortfall in pension funds. Moreover, it can be a legacy asset passed on to future generations.

How do we deliver the democratic financial plan to the masses?

A low-cost white-label solution is readily available, enabling financial planning firms to offer customised and branded financial products to their existing clientele and to nurture relationships with potential future clients.

This forward-thinking business model is modelled on the NHS principle of Patient Activation. This healthcare service also confronts a comparable predicament with an overwhelming demand for one-on-one assistance.

The NHS Patient Activation Measure (PAM) project is a research initiative to develop and test a tool for measuring patients’ knowledge, skills, and confidence in managing their health and healthcare. The PAM tool is designed to help healthcare providers and organisations better understand and support patients’ needs and preferences, and to promote patient-centred care and self-management.

The PAM tool consists of a questionnaire that assesses patients’ level of activation, knowledge, skills, and confidence in managing their health and healthcare. The questionnaire includes 13 items measuring different aspects of patient activation, such as understanding health conditions, confidence in managing medications, and ability to communicate with healthcare providers.

The PAM project involves several research studies and initiatives aimed at testing and validating the PAM tool, as well as exploring its use in clinical practice. Some of the key goals of the PAM project include:

- Developing a more comprehensive understanding of patient activation and its relationship to health outcomes, such as health status, quality of life, and healthcare utilisation.

- Identifying strategies for improving patient activation and promoting patient-centred care and self-management.

- Evaluating the effectiveness of the PAM tool in clinical practice and exploring its potential for improving patient outcomes and experiences.

The PAM project is part of a broader effort to promote patient-centred care and support patients in managing their health and healthcare. By providing healthcare providers and organisations with a tool for measuring and supporting patient activation, the PAM project aims to improve the quality of care and outcomes for patients while promoting greater patient engagement and self-management.

The foundational premise of the PAM project is based on the notion that most individuals can manage their health effectively in most instances. One-to-one support is typically only necessary during transitional phases or when encountering significant stress or change periods.

Introducing the financial activation measure (FAM).

Financial activation refers to developing the knowledge, skills, and confidence necessary to manage one’s finances effectively. This process involves understanding key financial concepts, such as budgeting, saving, investing, and debt management, and developing the skills and habits necessary to make informed financial decisions and take action to achieve one’s financial goals.

Financial activation is important because it can help individuals achieve greater financial stability and security, reduce financial stress, and improve their overall well-being. By developing the knowledge and skills necessary to manage their finances effectively, individuals can make more informed financial decisions, avoid costly mistakes, and take advantage of opportunities to save, invest, and build wealth.

Some of the key components of financial activation include:

- Financial education: Developing an understanding of key financial concepts and principles and how to apply them in practice.

- Goal setting: Identifying specific financial goals and creating a plan to achieve them.

- Budgeting: Developing a budget and tracking expenses to ensure that spending is aligned with financial goals.

- Saving: Establish a savings plan and regularly set aside money to build an emergency fund and work towards long-term goals.

- Investing: Learning about different investment options and strategies and investing in assets that align with one’s financial goals and risk tolerance.

- Debt management: Developing a plan to manage and pay off debts and avoiding high-interest debt where possible.

Financial activation is a process of developing the knowledge, skills, and habits necessary to manage one’s finances effectively and achieve greater financial stability and security. Individuals can improve their financial well-being and achieve their financial goals by taking an active and informed approach to their finances.

Why we must split financial planning and financial advice.

To begin with, regulated financial advice cannot be democratised, as it necessitates a personalised, one-on-one approach customised to the individual’s specific financial circumstances. In this context, the financial adviser must devote adequate time and attention to the client, which often commands a fee beyond the mass market’s financial means.

The Financial Conduct Authority’s (FCA) Perimeter Guidance (PERG) defines financial advice for regulatory purposes. The definition is important as it determines which activities require authorisation from the FCA and which do not.

Financial planning provided either during or in advance of regulated financial advice constitutes an integral aspect of the advice provided. As such, it cannot be made more widely available to the public unless a clear separation is maintained between the planning and advisory functions, a practice commonly known as the “Chinese wall”.

According to the PERG, financial advice is defined as “advising on investments” or “giving personal recommendations.” The definition clarifies that advising on investments is “advising a person on the merits of buying, selling, subscribing for, exchanging, redeeming, or holding a particular investment.” Meanwhile, giving personal recommendations refers to “advising a person on a course of action that is tailored to the person’s circumstances and involves a recommendation concerning a particular investment.”

In instances where an individual is provided with advice specifically tailored to their unique financial situation, and where no explicit recommendation is made concerning any particular investment vehicle, the guidance provided may fall outside the FCA’s PERG manual. However, general recommendations about investment opportunities may still be subject to regulatory oversight in certain situations, such as when given as part of a financial promotion.

In practical terms, this means that if an individual or company provides advice to another person that is tailored to their specific circumstances and involves a recommendation to buy, sell, or hold a particular investment, then they are likely to be considered as giving financial advice and will require authorisation from the FCA.

However, the PERG also clarifies that some activities may fall outside the definition of financial advice, such as providing general information about investments or making introductions to authorised firms. The key factor is whether the activity involves giving tailored advice or recommendations about a particular investment.

Overall, the definition of financial advice in the FCA PERG is an important regulatory concept that helps to determine which activities require authorisation from the FCA and which do not. Individuals and companies in the financial services industry need to be aware of this definition and ensure that they comply with regulatory requirements concerning the provision of financial advice.

What we need is a democratic financial planning.

Individuals who aspire to create sustainable livelihoods do not require investment products until they have accumulated wealth. It is only at that point that investment products become relevant. Therefore, in financial planning, it is advisable to initially prioritise creating tangible assets derived from productive assets, rather than selling investment products.

Once tangible assets have been established, educating the general public about managing smaller financial assets through Direct-to-Consumer (D2C) platforms becomes possible.

Under the FCA Handbook PERG 8.26, financial planning is regarded as generic advice. The isolation of financial planning from financial product intermediation is commonly known as “advice-only financial planning,” where a distinct boundary is established between financial planning and regulated financial advice per FCA guidelines. The primary objective of advice-only financial planning is the creation of wealth, and it does not involve any personalised recommendations for specific investment products. Rather, the emphasis is on client activation through education and comprehensive planning.

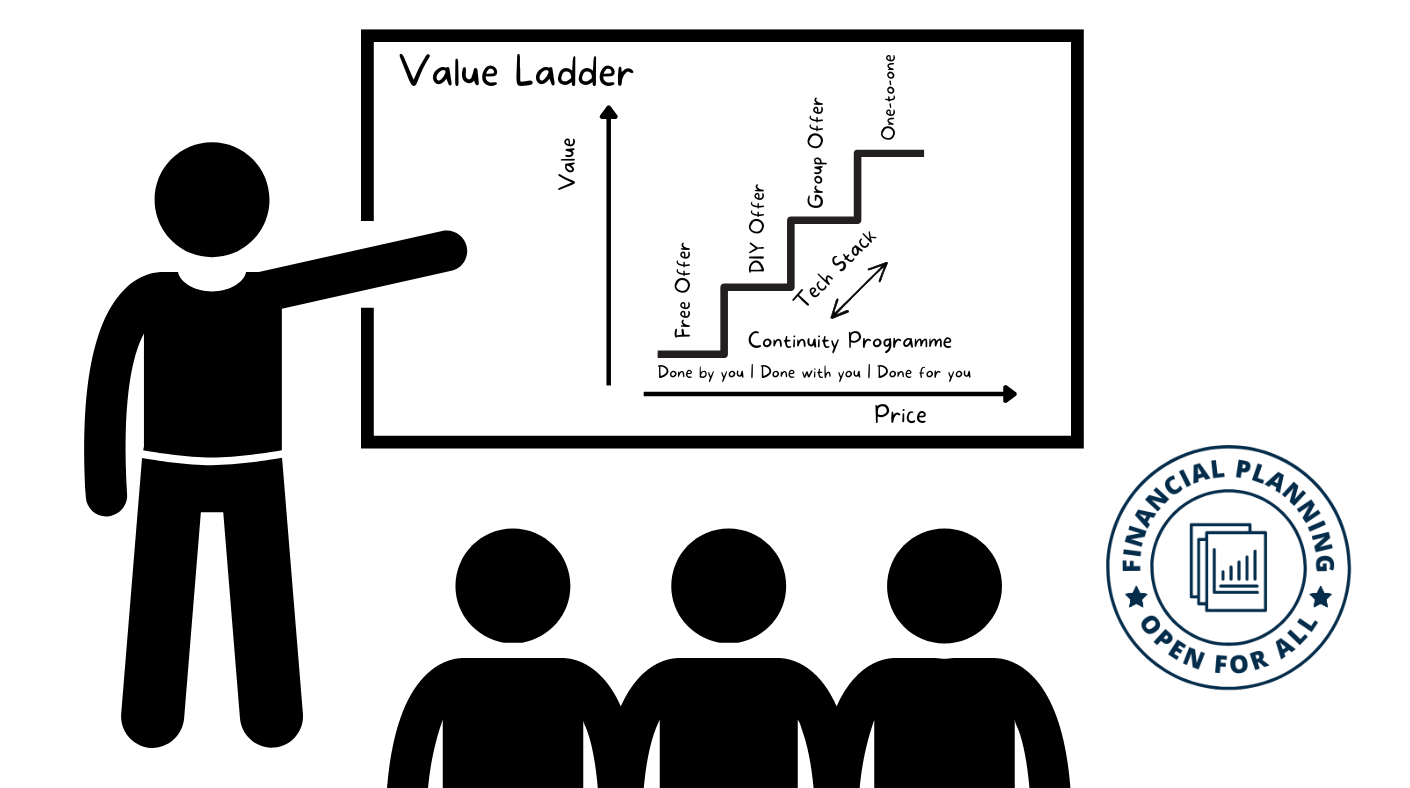

The Value Ladder: Sequencing servicing propositions for enhanced client engagement

The value ladder is a marketing term that describes a sequence of products or services a business offers, with each product or service providing increasing levels of value and price. By providing a ladder of products or services, businesses can capture customers at various stages of the buying journey and offer them different levels of value and investment.

The value ladder typically starts with a low-cost or free product or service that serves as an entry point for customers, such as a free trial, sample, or introductory product. This facility helps to attract new customers and build a relationship with them.

As customers become more invested, the value ladder offers products or services that provide greater value and are priced higher, such as an upgraded product, subscription service, or more comprehensive offering. These products or services may require a greater investment from the customer but also provide greater value regarding features, benefits, or results.

The value ladder can help businesses to increase customer lifetime value by providing a sequence of products or services that build on each other and offer increasing levels of value and investment. By offering various products or services at different prices, businesses can capture customers at various stages of the buying journey and provide options that meet their needs and budget.

Overall, the value ladder is a useful marketing tool for businesses that want to attract and retain customers by providing a range of products or services that offer increasing levels of value and investment. By designing a value ladder that meets the needs of their customers, businesses can build a loyal customer base and achieve greater revenue and profitability.

The Democratic Financial Planning model

To democratise financial planning we need a free entry point, and a range of offerings from low-ticket to higher ticket. Clients move up and down the ladder at different price points according to their needs.

In times of stress or change they access the one-to-one service. Between stress events, they work in groups (one-to-many) or on their own (none-to-one).

The conventional approach of one-to-one service can be replaced by one-to-many, and none-to-one approaches for greater efficiency and democratisation of financial planning. Instead of serving individual clients one at a time, it becomes possible to cater to groups of 100 or even 1,000 clients simultaneously. By adopting this method, clients can potentially be charged significantly lower fees, such as £100 or even £10, making financial planning more accessible to a wider audience. Overall, these novel approaches pave the way for democratising financial planning.

Where to go for further information…

Democratised financial planning is facilitated by a fintech stack that spans across the entire value ladder, and this system is already in place. The Academy of Life Planning has recently introduced HapNav, the first-ever customer-directed Open Banking powered financial planning application that can accommodate any client service level. Additionally, MoneyFitt, a financial education content library, enhances client financial activation. The technology employed in this process should be capable of accommodating any level of service, while being supported by an advice-only financial planner facilitator who provides expert guidance and knowledge for fees instead of time.

Our initial assumption, like the NHS, is that most people most of the time can manage their own finances with the right support. They only need to see the planner one-to-one in times of stress or change.

This future-proof model complies with the value-price assessment (VPA) criteria established by the Consumer Duty regulation, at each stage of the customer journey, as the client is at liberty to adjust the level of service to meet their specific requirements. When the done-for-you service may not represent an optimal value proposition, the financial planner can switch the client to a done-with-you or done-by-you service more tailored to their needs.

In conclusion, for individuals who seek to create sustainable livelihoods, it is vital to adopt a comprehensive and inclusive financial planning approach, which emphasises the creation of tangible assets through productive assets, supported by sound investment strategies. This methodology entails using financial activation technology and a customised end-user financial planning application, alongside training and accreditation of facilitators on The Game Plan model.

The Game Plan is a comprehensive and inclusive financial planning approach encompassing the whole-person paradigm framework described in this article. This innovative system is delivered through wealth-generating financial planning workbooks, complemented by a versatile tech stack and support desk. It is designed to cater to the diverse needs of individuals seeking to create sustainable livelihoods. In situations where individuals encounter stress or other transitional challenges, Game Plan practitioners may provide an Accident & Emergency facility, which offers personalised one-on-one support as required.

We express our gratitude for taking the time to read this article and trust that it has provided you with valuable insights into the potential for democratising financial planning in the future.

For further information, please visit our website: http://www.AcademyofLifePlanning.com.

2 thoughts on “Transforming Financial Planning with Fintech: Embracing a New Business Model to Serve All Consumers”