Transitioning from financial planner to non-intermediating financial planner is not about simply removing intermediation. Successful firms offer services 100-times greater than before. Here are eleven changes a financial planner needs to consider to succeed.

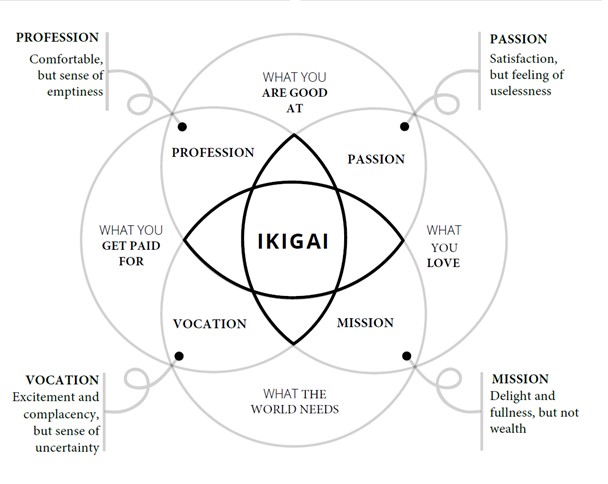

Firstly, members of the Academy ask their clients what an ideal life would look like. We then put in place the financial architecture to support it. We use a framework called the Ikigai. It is a Japanese concept with four elements representing the whole of you. It is referred to in the West as a whole-person paradigm (Mind-Body-Heart-Spirit, ref Stephen R. Covey, The 8th Habit). In the East, we simply ask:

What are you good at?

What do you love?

What does the world need?

What will you get paid for?

Your Ikigai is the meaningful project that arises from the nexus of your responses.

If I was to ask a financial adviser these questions, they might give me an answer that closely aligns with the life planner. I’m good with people. I’ve got good technical knowledge. I love helping others. The build back better world needs help with their lives and finances and is willing to pay where value is demonstrated.

If a financial adviser is where you are and a life planner is where you want to be, then I’m sure you would agree, you need a vehicle, system, or solution to get you there. Well, that’s the Academy and its Game Plan methodology. Here I lay out the eleven steps for a transition that we teach to our members

Let’s take what a financial adviser does, then deconstruct it and rebuild a future-ready framework and system for the life planner of tomorrow.

What financial advisers do:

The standard defines six steps of the personal financial planning process:

1. Establishing and defining the client and personal financial planner relationship.

2. Gathering client data and determining goals and expectations.

3. Analysing and evaluating the client’s financial status.

4. Developing and presenting the financial plan.

5. Implementing the financial planning recommendations.

6. Monitoring the financial plan and the financial planning relationship.

Step 1: Inspiration

The first step is to consider your values and gifts. The inspiration comes when you decide to live true to your own values an authentic and conscientious life. You choose the path of integrity. You choose to live a life true to yourself, and not as others expect you to live. You also choose to use your gifts and do what you are good at. According to ancient traditions from East and West, your gifts are given to you, and your life purpose is to use those gifts in the service of others. This is the path of purpose; the combination of integrity (divine wisdom) and purpose (divine will).

If your Ikigai more closely aligns with the life planner, your path of inspiration is revealed. This is self-knowledge. What is the inspiring meaningful project that falls out of your Ikigai?

Following the path is a choice. The Talmud states, “Do not be daunted by the enormity of the world’s grief. Do justly now, love mercy now, walk humbly now. You are not obligated to complete the work, but neither are you free to abandon it.”

Step 2: Intention

We set the intention to be a life planner, or whatever your Ikigai tells you is your favourite future. We decide to do it. We look at our planning process and change it, by adding to the “personal financial” piece and taking some things away.

More Than Financial

According to the Office for National Statistics Wealth and Asset surveys, regulated investments form less than 4% of wealth and assets of the average Brit (and that excludes business assets from the surveys). With whole person planning, we look at 100% total wealth, which is therefore at least 25 times larger than simply advising on regulated investments.

More Than Wealth Management

We are not just going to advise clients on how to manage wealth, we are going to show them how to create wealth in the first place. Our intention is to produce plans for wealth creation.

People create wealth, not financial products.

How Do I Create Wealth?

Wealth is what we own as an asset value.

Created via the voluntary exchange between people who can benefit from the thing the other has produced, through barter or using money as a medium of exchange. Exchange of time, skill, know-how, favours, or owned produce to which you have added value.

If we trade our time for money we receive an income. Our economic activity creates wealth. If we consume less than we receive we have surplus income or savings. If we consume less than we earn we own wealth. We can invest wealth to grow it. But the wealth itself was born of our labour.

If we add value to something we create wealth. We add value when the cost of production is less than the price the end consumer is willing to pay. The cost of supply is less than the price payable on demand. The difference is the wealth gained.

If we borrow money to pay for the cost of production. What we own may be more than what we owe. The difference is the wealth gained.

If the law gives us ownership of an asset, wealth is created. If there is demand from others to use our assets, others must pay rent to use what we own. For example, I could lend money and charge interest until the capital is repaid. Passive income adds to wealth.

Some definitions

“Asset” is something containing economic value and/or future benefit that you own. Strategies to achieve your financial life goals may also involve the creating, maintaining, exchanging, buying, or selling of assets. Assets can be tangible or intangible. Tangible assets include property, pensions, financial assets, business assets, and physical assets. Intangible assets include intellectual property, social network, reputation, health, time, and vitality.

“Financial Assets” are positive cash bank balances, savings, or financial products, such as shares, bonds, funds, some types of insurance, and personal pensions.

“Financial Product” is an instrument in which a person can either: make a financial investment (for example, a share); borrow money (for example, credit cards, loans, or bonds); or save money (for example, term deposits).

“Regulated Financial Products” in the UK are financial products regulated by the Financial Conduct Authority (FCA) intended for retail consumers.

“Unregulated Financial Products” are not regulated by the FCA. In general, unregulated financial products are unsuitable for retail consumers. They are designed for institutional and sophisticated private investors. FCA rules prohibit the sale of unregulated financial products to retail investors.

Step 3: Awareness

When we have set our sights on a new pathway we learn more about it. We upskill. We are aware that to be a life planner we must plan the client’s life and then put in place the financial architecture to support it.

So far, we have considered tangible assets.

More Than Tangible Assets

The holistic planner also plans intangible assets. Intangible assets include intellectual property, social network, reputation, health, time, and vitality.

We see the Mind-Body-Heart-Spirit whole person paradigm start to emerge. When determining goals and expectations we consider wealth in every area of the client’s life, which is far greater than just a consideration of tangible assets.

For example, you can have all the money you desire, but without health, it can count for nothing. We wish to plan to create wealth whilst maintaining good health. The result is wellbeing.

Total assets could be at least four times bigger than just tangible assets. Already we are advising on an area at least 100 times bigger than the traditional regulated financial adviser.

Are you now aware of the size of the task? It’s 100 times bigger than when we started!

Step 4: Sowing

We take the seed of the new business idea. We plant the seed. We now begin to sow the seeds by planning, acting and amending our process.

The six steps of the holistic life planning process:

1. Establishing and defining the client and life planner relationship.

2. Gathering client data and determining holistic goals and expectations.

3. Analysing and evaluating the client’s total wealth status.

4. Developing and presenting the life plan (including the total wealth plan).

5. Implementing the life planning recommendations.

6. Monitoring the life plan and the life planning relationship.

The seed we plant to create wealth is the business idea, the skills we use are project planning, business planning and coaching. The business plan includes a forecast of profit that we add to the lifetime wealth forecast. We model various “what-if” scenarios from which we select our favourite future. We satisfy ourselves that if all goes to plan we navigate happiness.

Step 5: Waiting

In the execution, we wait. We observe, monitor, and review our results. We adjust. We do more of what works, and less of what doesn’t.

Observe, monitor, and review the success of your project.

Our clients tell us these things add great value for them:

What Adds Value?

General advice:

Tax planning. Obtaining tax deductions, credits, tax-free investing opportunities. Tax bracket arbitrage – tax-sensitive liquidation.

Investment education. Picking lower-cost investments (expense ratios). Asset allocation using broadly diversified funds. Investment selection for alpha: small, value, momentum, profitability, etc. Rebalancing. Diversification. Behavioural coaching. Risk reduction.

Financial planning. Retirement planning strategies and withdrawal. Setting spending policies (withdrawal order) and budgeting. Confirming when you can stop working. Cashflow modelling becomes central to your proposition because it allows clients to see for themselves live on screen the impact of their choices or decisions.

Time management. Enhance the value of your time. Spend money to free up your time. Ensure things get done. Keep your interests in focus with unbiased advice. Doing the right thing by clients in all situations. Annual meetings and ongoing confirmation of the plan.

Wellbeing enhancement. Keeping clients focused on what really matters and helping them achieve their life goals as best you can.

And these things don’t.

Regulated advice:

Managing money for clients: In the era of passive auto-rebalancing low-cost well-diversified retail multi-asset funds. Does this add value in the commoditised investment market? Where Vanguard can do in 15 seconds, what a financial adviser/ intermediary takes 15 hours to complete?

Legendary investors Warren Buffett and John C. “Jack” Bogle, agreed on the key to successful investing. Buy and hold the stock market for the long term.

Advice with a view to buying or selling an investment does not add value.

If you try to trade in and out of the market, “your emotions will defeat you totally,” Bogle said, “Short-term betting is not a good way to go.”

Step 6: Germinating

The business start-up. Build it. Make it live. Don’t wait for perfection, launch before you are ready.

Just do it!

Step 7: Bursting Forth

Business growth period.

One-to-one advice is not fully scalable. Your time is limited, so your business is limited. If your solution is to hire more people, you end up being an HR manager instead of doing your Ikigai project. However, this could be a useful step to preparing your regulated business for exit. But you have to ask, what impact does working all hours have on your health and happiness?

General advice can be delivered to groups, and even made available on a Netflix-style subscription basis. You can earn while you sleep. The general advice model is fully scalable. The potential for growth is unlimited.

Step 8: Weeding

What is adding a great deal of cost to your business, but little in the way of value, is regulated activity.

You need to extract it like a weed.

Regularly detox your programme.

There are still consolidators out there willing to pay a handsome multiple for your recurring revenue stream. Cash-out now, before Consumer Duty bites on fee decency.

Step 9: Feeding

Keep learning. Working out what works best. Try it. If it works keep it. Build it into your business model. If not, discard it and try again.

Working for others creates income for you – and wealth for your boss.

Working for yourself creates income and wealth for you. Here you shift from employed to self-employed.

Step 9: Watering

You need to stop exchanging your time for money and start exchanging your know-how for money.

Sell your know-how. A shift from being self-employed by productising your service. What I mean by that is to create a vehicle, system, or solution and have others deliver it for you.

You shift from self-employed to business owner and your asset valuation increases.

Step 10: Harvesting

This is where you step out of the business. Others run it for you. You shift from being a business owner to an investor.

Your time is your own. You have created wealth and a nocturnal income stream.

Keep it or sell it. Retire from work, but never retire from meaningful projects. What’s your next Ikigai?

The Game Plan is a cyclic process for increasing your wealth and wellbeing.