The missing asset in school financial education

There is a strange imbalance at the heart of financial education.

Children are taught about money. They may learn about budgeting, saving, spending, borrowing, interest, pensions, and perhaps investing. These are useful topics. Nobody serious would argue that young people should leave school unable to understand debt, savings, tax, payslips, or the basic mechanics of money.

But there is a deeper question we rarely ask.

Why do we teach children about financial capital before we teach them about human capital?

Financial capital is money, investments, savings, pensions, property, and other financial assets. Human capital is the capacity of a person to create value through their knowledge, skills, health, relationships, creativity, judgement, adaptability, and work. It is the source from which most personal wealth is first created.

For a young person, this is not a marginal point. It is the whole story.

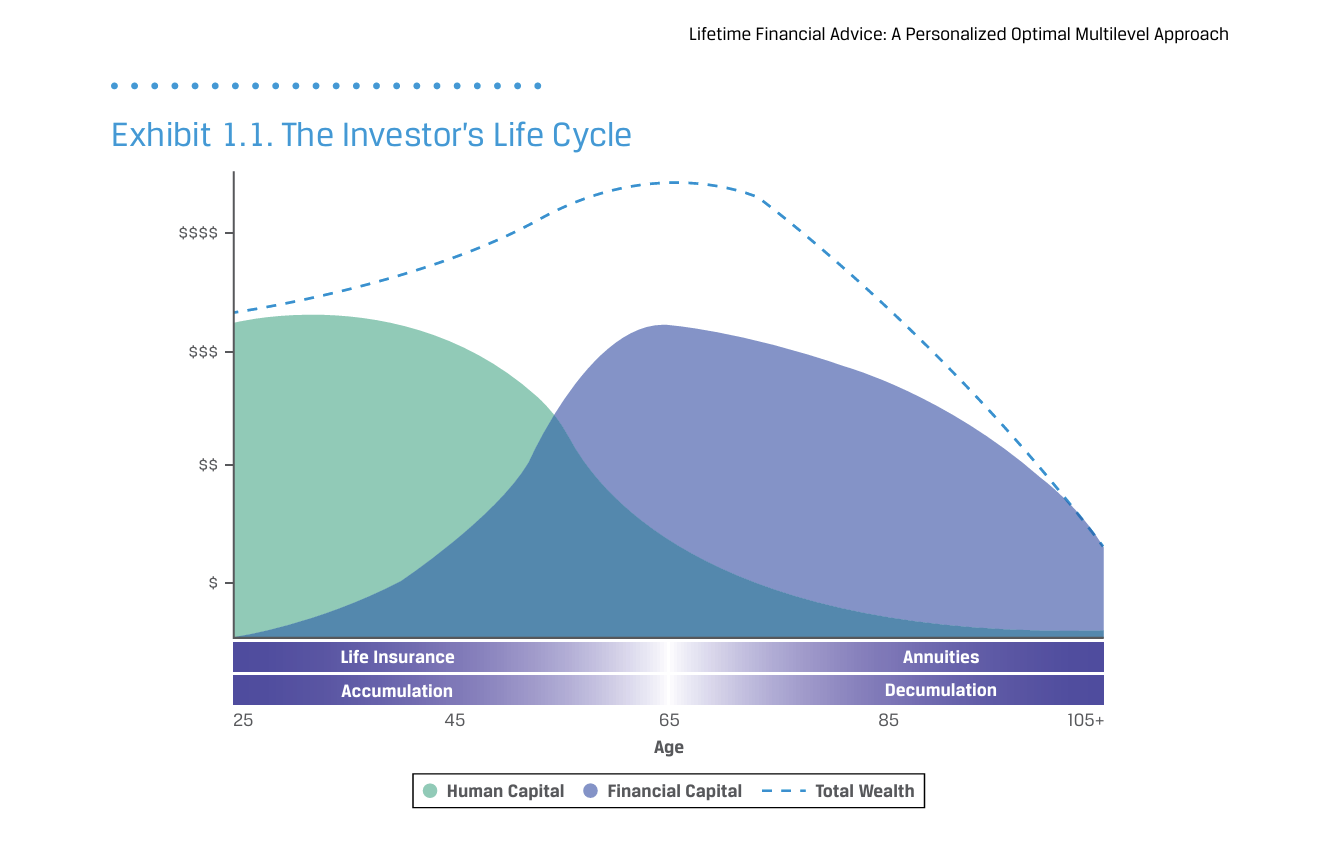

A recent CFA Institute Research Foundation monograph, Lifetime Financial Advice: A Personalized Optimal Multilevel Approach, illustrates the investor’s life cycle by showing that young people usually have very little financial capital, while their total wealth is dominated by human capital — the value of their future labour income. As people age, they convert some of that human capital into financial capital through earning, saving, and investing.

That should change the way we think about financial education.

If a 15-year-old has £50 in a savings account but millions of pounds of potential lifetime productive capacity ahead of them, why is the curriculum so heavily tilted toward managing the £50 rather than developing the person who may create the millions?

The old model: human capital as “bond-like”

Traditional life-cycle finance often treated human capital as “bond-like”. In simple terms, that meant future earnings were assumed to behave more like a relatively stable income stream than a volatile equity investment. A salaried professional, for example, might be assumed to have reasonably predictable earnings, allowing their financial capital to be invested differently.

The CFA paper acknowledges this tradition while also recognising that human capital varies in risk. A tenured academic may have safer, more bond-like human capital; a stockbroker may have riskier, more equity-like human capital; most people sit somewhere between those poles.

But the artificial intelligence era changes the assumptions.

Human capital is no longer simply a predictable stream of future earnings. It can now be rapidly devalued, displaced, amplified, repackaged, or multiplied. A skill that once created income security may become commoditised. Another skill, combined intelligently with AI, may become dramatically more productive.

This means human capital is not merely bond-like. In many cases, it is becoming option-like.

It can expire if neglected. It can collapse if disrupted. It can compound if developed. It can be multiplied through technology, networks, reputation, creativity, entrepreneurship, and adaptive learning.

That is the curriculum gap.

What schools currently mean by financial education

In England, financial education has historically sat mainly within secondary citizenship and mathematics. Parliamentary and House of Lords briefings describe it as covering areas such as budgeting, credit and debt, insurance, savings, and pensions, with primary schools not previously required to teach financial education beyond some money-related maths contexts.

The Government has now announced plans to strengthen the curriculum, including making citizenship compulsory in primary schools and ensuring pupils learn financial literacy earlier. The same announcement also refers to media literacy, law and rights, democracy, climate education, and a broader computing curriculum with exploration of data science and AI for 16–18-year-olds.

That is progress. But it still risks framing financial literacy as the management of money, not the development of the person who creates value.

Young Enterprise’s summary of the curriculum direction refers to primary pupils learning about the purpose of money, budgeting, saving, spending, needs and wants, risks, core financial concepts, responsible practice, and digital tools. At secondary level, the emphasis deepens into budgeting, debt, interest, mortgages, pensions, and real-world maths applications.

Again, all useful. But still incomplete.

Where is the structured education on personal agency? Where is the curriculum on earning capacity, adaptability, enterprise, value creation, AI leverage, human strengths, wellbeing, relational capital, reputation, creativity, and purposeful work?

Where is the conversation about the asset that a young person actually possesses?

Is this what happens when financial capital designs the curriculum?

This is the uncomfortable question.

When financial education is shaped by institutions built around financial capital, it naturally focuses on financial capital. Banks teach saving. Pension firms teach pensions. Investment firms teach investing. Insurers teach risk products. Wealth managers teach long-term accumulation.

Some of this is sincere. Some of it is socially useful. But the gravitational pull is obvious.

The child is slowly prepared to become a future consumer of financial products.

They are less often prepared to become the active creator, protector, and steward of their own total wealth.

This is not necessarily a conspiracy. It is an institutional lens. Financial capital institutions see the world through financial capital. So when they are invited to help design financial education, they tend to reproduce the worldview they already inhabit.

The result is not false education. It is partial education.

And partial education can still be harmful when it leaves out the most important part.

In the AI age, human capital can be lost or multiplied

The OECD’s work on AI and skills highlights that AI is changing the tasks people perform and the skills they require, even where workers do not need specialist AI skills such as machine learning or natural language processing.

The OECD also identifies skills as a major barrier to AI adoption, second only to cost in its employer surveys, and stresses the need for collaboration between industry, education, and government to prepare people for changing digital demands.

This should be central to financial education.

A young person’s future financial wellbeing will not be determined only by whether they understand compound interest. It will be shaped by whether they can compound themselves.

Can they learn? Can they adapt? Can they use AI safely and intelligently? Can they ask better questions? Can they create value others recognise? Can they organise their thoughts, solve problems, communicate clearly, build trust, work with others, recover from setbacks, and make wise choices under uncertainty?

These are not soft extras. They are wealth-forming capabilities.

In the Academy of Life Planning language, this is not just about financial literacy. It is about restored human agency.

The curriculum should start with the person, not the product

A Total Wealth curriculum would not ignore money. It would put money in its proper place.

It would begin with the young person as an asset-bearing human being.

It would teach that wealth is not only what sits in a bank account. Wealth is also health, skills, confidence, clarity, relationships, purpose, resilience, creativity, trustworthiness, contribution, and the capacity to meet life’s needs over time.

It would help young people understand that their future does not begin with a pension product. It begins with questions like:

What can I do?

What can I learn?

What problems can I solve?

What do people need?

What strengths do I already have?

How can technology multiply my contribution rather than replace it?

How do I convert capability into income without losing myself in the process?

That is financial education at the level of human agency.

From financial literacy to total wealth literacy

The term “financial literacy” is too narrow for the world young people are entering.

They need total wealth literacy.

That means understanding how different forms of wealth interact:

- Human capital: skills, knowledge, health, energy, creativity, adaptability, judgement.

- Social capital: relationships, trust, networks, community, reputation.

- Environmental capital: the conditions that support life, wellbeing, and sustainable work.

- Spiritual or meaning capital: purpose, values, identity, belonging, coherence.

- Financial capital: money, savings, investments, pensions, property, and financial resources.

Financial capital matters. But it is often the downstream result of the other capitals.

A young person who understands budgeting but has no sense of their own capability may remain dependent. A young person who understands investing but cannot create income may be vulnerable. A young person who understands pensions but cannot navigate AI disruption may be exposed.

The missing lesson is not “how money works”.

The missing lesson is “how I create, protect, and direct value in my life”.

The Academy’s challenge

At the Academy of Life Planning, we should be clear about the imbalance.

We do not need less financial education. We need better financial education.

We need education that is not designed primarily around future product engagement, but around present and future human agency. We need children to understand money, but also to understand themselves as the primary source of their own total wealth.

In the pre-AI era, it may have been possible to treat human capital as a background assumption.

In the AI era, that is no longer credible.

Human capital is now the front line. It is where inequality will widen or narrow. It is where exploitation will deepen or be resisted. It is where young people will either become passive consumers of systems they do not understand, or active participants in shaping lives aligned with their values.

The curriculum should reflect that.

It is time to rebalance financial education.

Not money first.

Not products first.

Not institutions first.

Human capital first.

Because before a child can manage wealth, they need to know they can create it.

A Practical First Step: Get Secure

This is where the argument becomes practical.

If schools, financial education programmes, and policy systems have largely missed human capital, then we need simple tools that help fill the gap.

That is one reason we created Get Secure.

Get Secure is a free AI-assisted planning app designed to help people identify the human capital they already have and explore how it could be strengthened, protected, or leveraged in the age of AI.

It includes a dedicated section that helps users reflect on their skills, strengths, interests, experience, relationships, creativity, adaptability, and practical capabilities. It then helps them consider how AI might multiply those assets.

Could AI help them learn faster?

Communicate more clearly?

Build a portfolio?

Explore self-employment?

Prepare for interviews?

Develop a service?

Turn lived experience into useful insight?

Find a route back into education, training, work, enterprise, volunteering, or purposeful activity?

This matters because human capital is no longer a static assumption. In the AI era, it can be lost, ignored, weakened, or multiplied. The difference often begins with whether someone can see what they already have within them.

Get Secure takes under an hour to complete.

It is free.

It is accessible at:

It will not replace schools, teachers, youth workers, careers advisers, employers, families, or public policy. Nor should it. Young people need real human support, trusted relationships, and proper pathways.

But it may provide something that is often missing.

A first structured conversation about agency.

That is why this matters in the context of nearly one million young people in the UK being outside education, employment, or training. The NEET label may be administratively convenient, but it can flatten a human reality. Many of these young people are not lacking potential. They may be lacking structure, confidence, opportunity, encouragement, and a believable first step.

A Total Wealth curriculum would not begin by asking a young person to manage £50 better.

It would begin by helping them recognise the much larger source of future wealth already present in their life: their human capital.

Their ability to learn.

Their capacity to create value.

Their judgement.

Their relationships.

Their health.

Their confidence.

Their imagination.

Their adaptability.

Their ability to use AI as a multiplier rather than be displaced by it.

That is the missing bridge between financial education and real financial wellbeing.

We should still teach budgeting, saving, debt, pensions, and investing.

But not before we teach young people how value is created.

Not before we help them understand that they are not merely future consumers of financial products.

They are creators of wealth, meaning, contribution, and possibility.

Get Secure has been built to help start that conversation.

It is a small tool for a large gap.

But when someone feels stuck, small first steps matter.

And for many young people, the most important first step may not be opening a savings account.

It may be discovering that they are the asset.