The Twin Peaks of Financial Planning

Business Owners: Do you increase your investment in the intermediary model to dominate the market or is it time to divest the intermediary line?

There are two types of financial planners. There is the Financial Intermediary and the Non-Intermediating Financial Planner.

The Financial Intermediary is regulated by the Financial Conduct Authority on account of having undertaken regulated activity, that is making personal recommendations with a view to the buying or selling of investment products. Financial Planning is not a regulated activity, provided it does not form part of a process containing a regulated activity.

The Non-Intermediating Financial Planner sells financial plans, not products. They do not hold agency agreements with product providers, placing a wall between advice and product. NIFP’s act as an agent of the client, rather than a selling agent. NIFPs are not registered with or regulated by FCA. NIFPs are instead bound by the codes of their professional bodies and trade associations.

Here is the Financial Intermediation (FI) Process (ISO 22222):

1. Establishing client/planner relations.

2. Determining goals and gathering data.

3. Evaluating the client’s financial status.

4. Developing and presenting the financial plan.

5. Implementing recommendations.

6. Monitoring the plan recommendations.

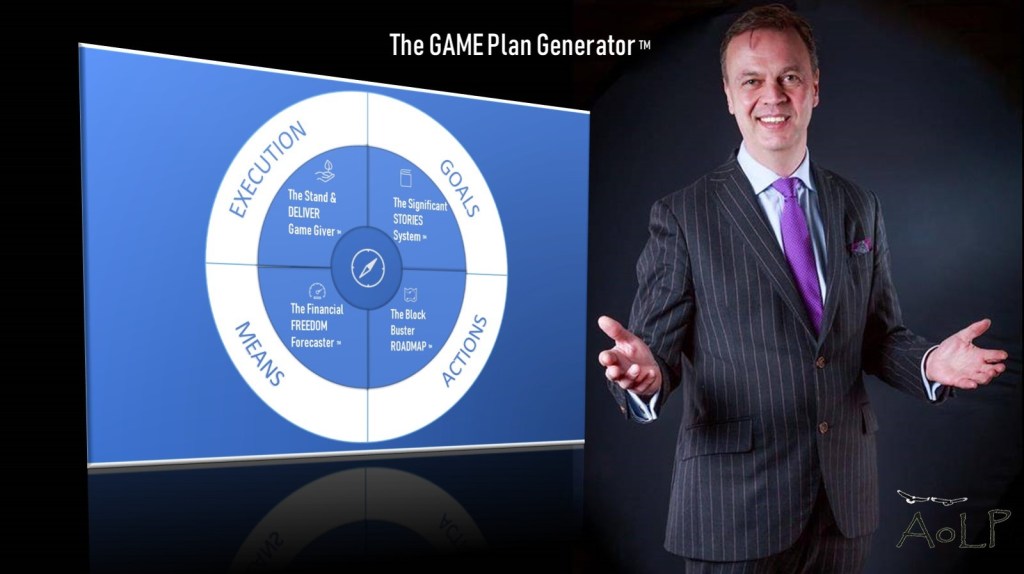

Here is the Non-Intermediating Financial Planning (NIFP) Process (The GAME Plan):

1. Goals. Listen to the client. Determine goals in every area of their life, not just financial goals.

2. Actions. Identify actions clients can take to overcome obstacles and achieve life goals. Produce an action plan. Be a life coach. Plan the client before planning the money.

3. Means. Gather data. Evaluate the client’s financial status. Develop and present the financial plan. Include wealth creation strategies, not simply wealth management/ preservation strategies. Make no product recommendations. Sell no product.

4. Execution. Be a personal coach to the client. Educate them. Show them how as far as possible to DIY on product. Repeat as and when required. Refer to Financial Intermediaries if product research, product recommendations, product implementation or ongoing product management is required.

The difference:

- The NIFP Planner acts on behalf of the client, the relationship is with the client only. No adviser relationships with product providers exist. The adviser listens to the client from the start of the first meeting, without pulling out a product brochure, and act as the agent of the client. The FI, on the other hand, is a selling agent of one or more product providers and that’s why relations need to be established with the client and brochures pulled out before listening to the client. Unfailingly, product brochures appear in the first 82 seconds of the discovery meeting, as the FI establishes client/ planner relations.

- The FI begins with the money. Goals and data gathered are financial. Missing out steps is destructive. Planning the money before the client is exhaustive. Planning the client before the money is productive. The NIFP plans the client before the money. The money conversation does not start until step 3.

- The FI financial plan is all about products. There is a shortfall analysis delivered against the adviser, and their compliance officer’s, perceived view of goals. Protection. Retirement. Investments. Savings and Mortgages. In that order. Typically, to accumulate and preserve wealth as a priority for the best part of 50 years on the bet the client can buy freedom in the last 16 years. The NIFP, on the other hand, asks the client about their life goals, includes stuff money can’t buy, plans against that, and, when planning money, talks about wealth creation as well as wealth management and protection. For it is the client who creates wealth, not any product.

- The FI researches the market – putting out that their stock selection and market timing will add value to the service. The FI makes a recommendation, calling upon their crystal ball. The FI implements the recommendation, as though implementation was difficult. The FI monitors the wealth management solution as if the product needed monitoring.

- According to Which? 90% of FIs take fees on a percentage of assets under influence. The accumulation strategy the FI proposes therefore serves the FI’s interest, and the interest of the product providers they hold selling agencies with. There lies the conflict in interest. The poor old client must place their life on hold whilst working for the best part of 50 years on the treadmill of work existence, and 9 in 10 lose the bet of buying happiness in later life.

- The NIFP simply educates the client that in most cases intermediation, after charges, fails to beat markets and DIY solutions can be set up in minutes to deliver better outcomes as simply as online banking, and held for the duration without the need for ongoing actions. Behavioural economics is general advice and forms part of the education process. Saving the client, a third to a half of their life savings in unnecessary fees and charges.

Does this sound like a harsh view? The FCA who regulate FIs agree. The FCA, according to its latest report Policy Statement PS20/6, is placing its cross-hairs on ongoing charges levied by FIs, which it described as among ‘substantial conflicts of interest’ advisers face. But the FCA goes further. ‘Our view’ it said, ‘is that many consumers would not benefit from ongoing advice, as their circumstances are unlikely to change significantly from year to year.’

An old Cherokee is teaching his grandson about life:

“A fight is going on inside me,” he said to the boy.

“It is a terrible fight and it is between two wolves. One is evil – he is anger, envy, sorrow, regret, greed, arrogance, self-pity, guilt, resentment, inferiority, lies, false pride, superiority, and ego.”

He continued, “The other is good – he is joy, peace, love, hope, serenity, humility, kindness, benevolence, empathy, generosity, truth, compassion, and faith. The same fight is going on inside you – and inside every other person, too.”

The grandson thought about it for a minute and then asked his grandfather: “Which wolf will win?”

The old Cherokee simply replied, “The one you feed.”

Do you increase your investment in the FI model to dominate the FI market or do you divest the FI line?

As financial planners, virtually all of us have been financial intermediaries. The Non-intermediating Financial Planner is something we had never even heard of before now. It is the same for consumers too. As consumers, we buy hundreds of thousands of products every month. When we talk to a financial planner we expect to be sold a product. That is just the way it is.

Financial Intermediation is itself a service. And just like us, this service has a life cycle. Older, long-established services eventually become less popular, while in contrast, the demand for new, more modern services usually increases quite rapidly after they are launched.

Because most companies understand the different proposition life cycle stages, and that the services they sell all have a limited lifespan, the majority of them will invest heavily in new proposition development in order to make sure that their businesses continue to grow.

I was the lead proposition architect for wealth in the banks for over a decade, and here is what I can tell you.

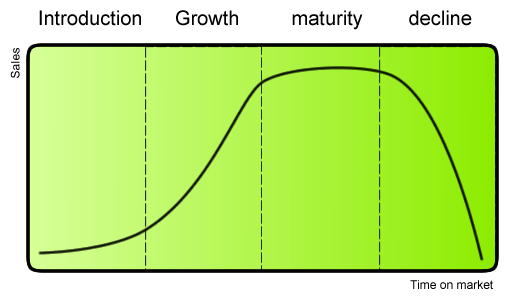

Proposition Life Cycle Stages Explained

The proposition life cycle has four very clearly defined stages, each with its own characteristics that mean different things for business that are trying to manage the life cycle of their proposition.

Introduction Stage: This stage of the cycle could be the most expensive for a company launching a new service. The size of the market for the service is small, which means sales are low, although they will be increasing. On the other hand, the cost of things like research and development, consumer testing, and the marketing needed to launch the service can be remarkably high, especially if it is a competitive sector.

Growth Stage: The growth stage is typically characterised by a strong growth in sales and profits, and because the company can start to benefit from economies of scale in production, the profit margins, as well as the overall amount of profit, will increase. This makes it possible for businesses to invest more money in the promotional activity to maximise the potential of this stage.

Maturity Stage: During the maturity stage, the service is established and the aim for the service provider is now to maintain the market share they have built up. This is probably the most competitive time for most services and businesses need to invest wisely in any marketing they undertake. They also need to consider any service modifications or improvements to the delivery process which might give them a competitive advantage.

Decline Stage: Eventually, the market for a service will start to shrink, and this is what is known as the decline stage. This shrinkage could be due to the market becoming saturated (i.e. all the customers who will buy the service have already purchased it), or because the consumers are switching to a different type of service. While this decline may be inevitable, it may still be possible for companies to make some profit by switching to less-expensive distribution methods (i.e. robo-advisers) and cheaper markets.

PESTLE on Financial Planning: What are the Market Drivers?

Market drivers are the underlying forces that compel consumers to purchase products and services. When market drivers are positive they signify opportunities for market growth and development. When they are negative they signify trends of market decline and threats to business operation.

Market drivers come in seven distinct types. A PESTLE analysis is a framework to analyse these seven drivers (Political, Economic, Sociological, Technological, Legal and Environmental) influencing an organisation from the outside. See footnotes for details.

By understanding these external environments, firms can maximise the opportunities and minimise the threats to their operations. Let us look at the drivers in more detail in the context of Financial Planning.

Financial Intermediary (FI)

This market is well established and mature. We are seeing reducing numbers of regulated individuals, to just over 25,000, from 400,000 some 20 years ago. Boutique firms are selling out to consolidators and we now have just over 5,000 larger firms. Adviser numbers and firm numbers are dwindling. Big firms dominate. Smaller firms are fast disappearing.

There is a growing compliance burden for market participants. Professional Indemnity Insurance costs are skyrocketing. Barriers to market entry are high. The regulators are placing a downward pressure on margins. Renewal income has come under threat as firms milk for cash while they can. Liabilities chase business owners to the grave. Services retract accordingly, as unprofitable higher risk customer groups are dropped (i.e. DB pension transfers).

The largest unprofitable customer segments to be dropped is mass affluent. Adviser thresholds have increased from £100k to £250k of investible assets. Now, 95% to 98% of the market have been disintermediated. There is a growing advice gap for the British public, which in turn leads to growing wealth inequality.

Whilst international intermediary groups exist, the regulators increasingly restrict operations to UK.

The FI Market is in decline stage.

Non-Intermediating Financial Planning (NIFP)

The NIFP market is in its infancy and in its introduction stage.

There are 400,000 ex financial advisers in UK, many not yet retired who could potentially enter this market. Barriers for market entry are low. Potential for future growth is substantial. Most current market participants are just starting up. Or, are setting up side line NIFP firms.

There is little to no compliance burden for market participants. Professional Indemnity Insurance costs are low, less than £100 per annum. There is truly little price pressure. All the client value lies in the planning not the intermediation. Clients trust this model. Referrals are more easily obtained. Retainer income is more easily established.

There are few, if any, legal liabilities following business owners to the grave.

Market participants can afford to pass on cost savings from little to no compliance, of up to 50% of revenue, passed on to the client. This lowers adviser charges, whilst maintaining adviser margins. This is a more profitable business model. And, a more accessible service for most.

The service is relatively easy to deliver. Businesses can deliver the service relatively quickly. Due to lower price points, NIFP services are more accessible for mass affluent. Plugs the advice gap.

Due to cv-19, people are more inclined to use ZOOM online services. Due to the absence of wet signatures and the handling of client money, NIFP services lend themselves well to online delivery.

The world finds itself in a global money or your life emergency and people need money and life plans. There is a high demand for this service.

Due to lower levels of regulation NIFP services translate across borders, enabling business owners to make global offerings available. NIFP can be delivered from anywhere, to anywhere.

Conclusion

Business Owners: It is time to innovate!

Consider setting up a hybrid financial planning business model. One firm FI, the other NIFP. This diversifies your business portfolio and reduces the risk of interruption to business operations. Keep a wall between the two.

There is still plenty of revenue to be earned from the FI model. But that is not going to last for ever. It is only a matter of time before the increasingly negative outlook for Financial Intermediation is going to be reflected in exit valuations.

The FCA is placing its crosshairs on ongoing charges levied by FIs.

Consider having a foot in both camps.

Footnotes: What is PESTLE?

Political Factors

Political factors relates to the pressures and opportunities brought by political institutions and to what degree the government policies impact the business.

– Government policies

– Government term and change

– Trading policies

– Funding, grants and initiatives

– Lobbying and pressure groups

– Wars, terrorism and conflicts

– Elections and political trends

– Internal political issues

– Inter-country relationships

– Local commissioning processes

– Corruption

– Bureaucracy

Economic Factors

Economic factors relates to economic policies, economic structures and to what degree the economy impacts the business.

– Local economy

– Taxation

– Inflation

– Interest

– Economy trends

– Seasonality issues

– Industry growth

– Import/export ratios

– International trade

– International exchange rates

Social Factors

Social factors relates to the cultural aspects, attitudes, beliefs, that will affect the demand for a company’s products and how the business operates.

– Demographics

– Media views of the industry

– Work ethic

– Brand, company, technology image

– Lifestyle trends

– Cultural Taboos

– Consumer attitudes and opinions

– Consumer buying patterns

– Ethical issues

– Consumer role models

– Major events and influences

– Buying access and trends

– Advertising and publicity

Technological Factors

Technological factors relates to the technological aspects, innovations, barriers and incentives, and to what degree these impact the business.

– Emerging technologies

– Maturity of technology

– Technology legislation

– Research and Innovation

– Information and communications

– Competitor technology development

– Intellectual property issues

Legal Factors

Legal factors relates to the laws, regulation and legislation that will affect the way the business operates.

– Current legislation

– Future legislation

– International legislation

– Regulatory bodies and processes

– Employment law

– Consumer protection

– Health and safety regulations

– Money laundering regulations

– Tax regulations

– Competitive regulations

– Industry-specific regulations

Environmental Factors

Environmental factors relates to the ecological and environmental aspects that will affect the demand for a company’s products and how that business operates.

– Environmental regulations

– Ecological regulations

– Reduction of carbon footprint

– Sustainability

– Impact of adverse weather