“When it comes to your finances, some professionals position themselves between you and your decisions. Others position themselves beside you. The difference is agency — and it matters.”

For years, citizens have been conditioned to believe a simple equation:

regulated = safer

unregulated = riskier

It sounds sensible. It feels reassuring.

But in today’s financial landscape, that assumption is not just outdated — it can be actively misleading.

This isn’t a philosophical claim. It’s a structural one.

The Reality Shift Most People Haven’t Noticed

Financial services evolved in an era when:

- information was scarce

- access was restricted

- execution required specialists

In that world, intermediaries made sense.

In 2026:

- information is universal

- products are commoditised

- platforms enable direct execution

- AI explains decisions instantly

The original justification for product intermediation — informational advantage — has disappeared.

Yet behaviour hasn’t caught up.

Many people still assume they are safer using an intermediary simply because that intermediary is authorised.

That assumption deserves examination.

Regulation Does Not Measure Safety — It Measures Activity Type

Regulation is not applied randomly. It is imposed where activities can directly cause financial loss.

Typically, that means services that:

- recommend specific products

- arrange transactions

- control assets

- exercise discretion

In other words:

Regulation tends to exist where risk already exists.

So the presence of regulation does not prove safety.

It often signals that the underlying activity carries enough risk to require supervision.

The Critical Distinction Most Consumers Miss

There are two fundamentally different professional roles (that is individuals professionally qualified, registered with a professional body and subject to their codes of conducct) in personal finance:

| Role | Function | Risk Source |

|---|---|---|

| Intermediary | Executes financial transactions | Outcome liability |

| Planner | Supports decisions | Communication clarity |

One controls financial outcomes.

The other supports thinking.

That structural difference matters more than authorisation status (registered and authorised to carry out a permitted risky activity) .

Because professional risk is driven primarily by one factor:

The ability to directly cause financial loss.

Where Real Financial Harm Historically Occurs

Major compensation scandals in financial history have overwhelmingly arisen in sectors that were:

- authorised

- supervised

- compliant

- regulated

Why?

Because those sectors involve transaction authority.

Losses that are measurable, attributable, and traceable are the ones that generate claims. And those only occur where someone has the power to implement decisions — not merely discuss them.

Claims arise where money moves.

Not where plans are discussed.

The Regulation Illusion

Many professionals and consumers instinctively think:

“If it’s regulated, my risk is lower.”

Insurers, courts, and professional risk assessors don’t judge safety by labels or titles. They evaluate tangible risk drivers:

- who controls the assets

- who has the power to cause financial loss

- how clearly responsibility can be traced

- what the historical claims data shows

Regulatory status is only relevant if it materially alters one of those factors.

In many cases, it doesn’t.

Why Intermediation Can Increase Risk

When an intermediary is inserted into a decision chain, three new variables appear:

- execution authority

- incentive structures

- transactional liability

Each introduces potential failure points.

By contrast, a professionally qualified, registered planner who does not intermediate:

- cannot transact on your behalf

- cannot move your money

- cannot select products for you

- cannot execute decisions

Which means structurally they cannot cause transactional loss.

They can only influence thinking.

That is a fundamentally lower-risk position.

The Psychological Trap

Humans often equate familiarity with safety.

Older models feel safer because they are familiar.

Newer models feel riskier because they are unfamiliar.

But risk is not determined by familiarity.

It is determined by mechanics.

And mechanically:

removing transactional authority reduces risk.

The Question Citizens Should Be Asking in 2026

Not:

“Is this person authorised?”

But:

“What power do they actually have over my money?”

That question reveals more about real safety than any regulatory label.

What Structurally Trustworthy Financial Systems Look Like

A trustworthy financial system is not built on reassurance. It is built on architecture.

It has:

Transparency — you can see how it works

Alignment — incentives don’t distort outcomes

Autonomy — you remain in control

When those exist, trust is built into the design itself.

That is the standard modern citizens should expect.

Why the Old Model Still Exists

Intermediation persists not because it is structurally necessary, but because:

- legacy revenue models remain

- institutions evolve slowly

- consumers assume tradition equals protection

Systems often outlive the conditions that justified them.

But once those conditions disappear, change becomes inevitable.

The Direction of Travel

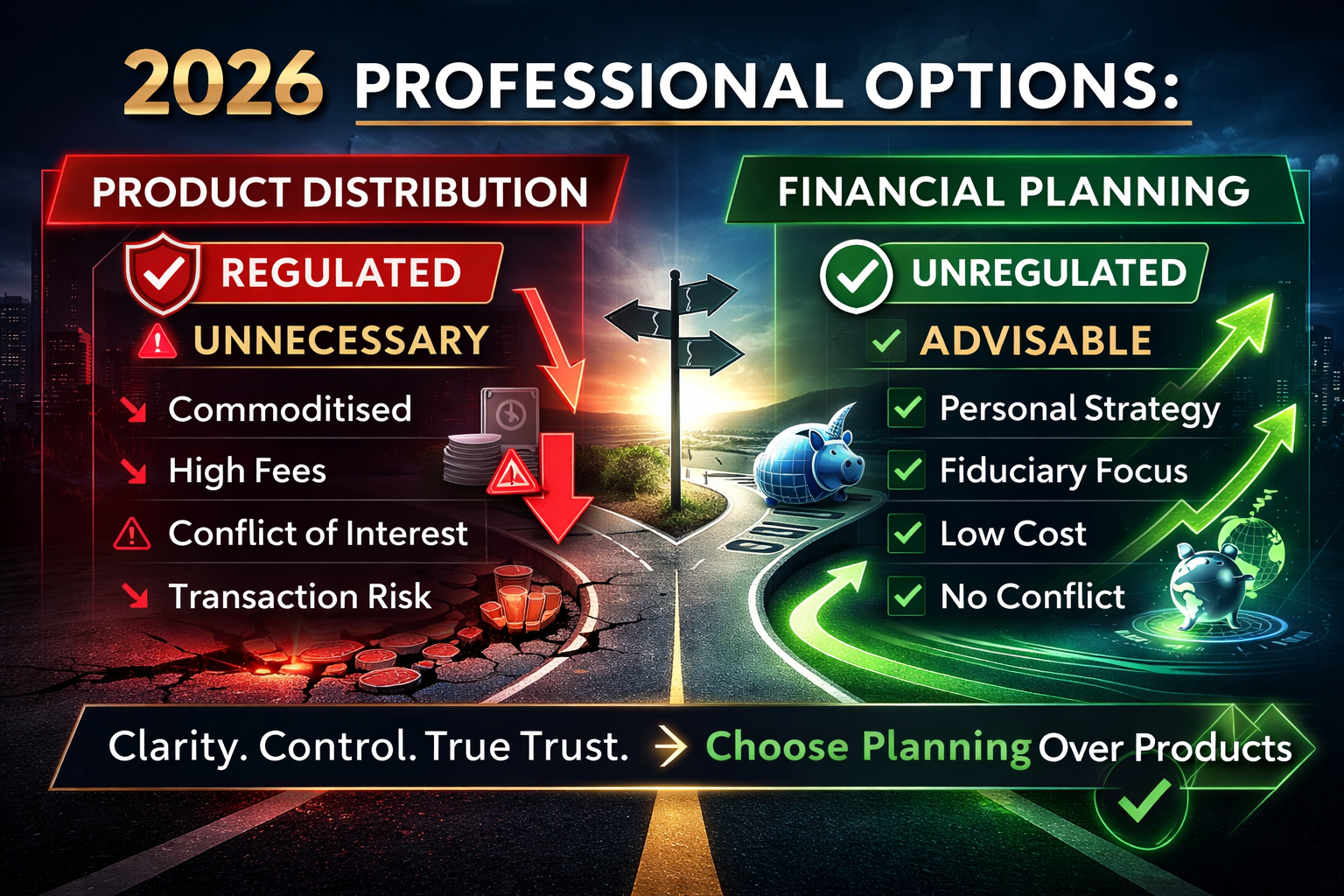

Markets are already separating two functions that were historically bundled:

- product distribution

- financial planning

Distribution is being automated.

Planning is becoming more valuable.

The future does not belong to transaction facilitators.

It belongs to decision architects.

The Realisation Moment

The most important insight citizens can grasp today is this:

Safety does not come from regulation alone.

Safety comes from structure.

And structurally, a professional who cannot execute transactions is often lower risk than one who can.

The Wake-Up Call

For decades, people asked:

“Which adviser should I use?”

In 2026, the more intelligent question is:

“Do I need an intermediary at all?”

Because once individuals understand they can act directly, they start choosing support intentionally — rather than assuming it is always required.

That shift is called agency.

And agency is the foundation of financial freedom.

The era of blind reliance is ending.

The era of informed autonomy has begun.

The mission now is simple:

help citizens see the system clearly enough to choose wisely within it.

[Reference: The Regulation Illusion: Why “Authorised” Doesn’t Always Mean Lower Risk.]

The Great Financial Illusion of 2026 — And Why It’s Time Citizens Reclaimed Control

For decades, the financial system has operated on an assumption most people never consciously agreed to:

That ordinary individuals cannot manage their own financial lives without an intermediary.

That assumption may once have reflected reality.

In 2026, it no longer does.

Yet millions of people still behave as if it does.

This is not a criticism. It’s a wake-up call.

The World Has Changed. The Model Hasn’t.

Technology has fundamentally altered the economics of financial services:

- Investment products are commoditised

- Platforms provide direct access

- Fees are transparent

- Tools are automated

- Knowledge is universal

- AI explains decisions in seconds

In practical terms, the informational advantage that once justified product intermediation has disappeared.

What used to require a professional can now be executed safely, cheaply, and clearly by individuals themselves.

And when scarcity disappears, so should dependence.

The Hidden Truth Most People Haven’t Been Told

Financial planning and financial product distribution are not the same activity.

One is:

helping someone think clearly about their life and money.

The other is:

implementing a regulated transaction.

They were historically bundled together — not because they had to be, but because it was commercially efficient.

Today that bundle is no longer structurally necessary.

Yet many consumers still pay for it as if it were.

What Structurally Trustworthy Systems Look Like

A trustworthy system is not defined by good intentions.

It is defined by design.

A structurally trustworthy financial system has three characteristics:

1. Transparency

You can see how it works and how it gets paid.

2. Alignment

The person helping you does not earn more when you do something unnecessary.

3. Autonomy

You can act independently if you choose.

When these exist, trust is built into the architecture — not dependent on personalities.

Why the Old Model Persists

If the world has changed, why hasn’t behaviour?

Because systems outlive their usefulness.

- Institutions adapt slowly

- Professions defend legacy models

- Consumers assume tradition equals necessity

Most people don’t question financial structures for the same reason they don’t question plumbing or electricity: they assume someone else has already solved it.

But assumption is not the same as truth.

The Real Question Citizens Should Be Asking

Not:

“Which adviser should I use?”

But:

“Do I actually need an intermediary for this decision?”

That single question changes everything.

Because once people realise they can act directly, they start deciding when they should seek help — rather than assuming they always must.

That shift is called agency. And agency is the foundation of financial wellbeing.

The Role of the Modern Planner

The future does not belong to product distributors.

It belongs to professionals who help people:

- think clearly

- decide wisely

- act confidently

That is planning.

That is guidance.

That is human value.

And it is very different from intermediation.

Why the Academy Exists

The Academy of Life Planning was founded on a simple conviction:

People deserve systems they can trust without needing blind faith.

Its mission has never been to oppose professionals.

It has always been to evolve the profession.

From:

transaction facilitators

To:

architects of financial lives.

From:

gatekeepers

To:

guides.

From:

intermediaries

To:

empowerers.

The Invitation

2026 is not the future.

It’s already here.

Citizens now have tools, access, and intelligence at their fingertips that previous generations never imagined.

So the question is no longer whether people can take control of their financial lives.

The question is:

Will they?

The era of dependency is ending.

The era of informed autonomy has begun.

If you are ready to understand your options, learn how modern planning works, and see what a structurally trustworthy financial life looks like, explore the Academy and discover what becomes possible when knowledge replaces reliance.

Ready to Step Across the Bridge?

If you’re sensing that traditional planning is no longer enough for the clients you truly want to serve, that instinct is worth paying attention to.

The next evolution of your professional journey is not about abandoning what you know. It’s about expanding it — integrating human capital, behavioural insight, and life architecture into the financial planning framework you already understand.

The Academy of Life Planning invites you to explore that transition.

Across the bridge you’ll discover:

- A proven framework for integrating human and financial capital

- A professional pathway to becoming a Total Wealth Planner

- Tools that deepen client outcomes and professional fulfilment

- A global community of forward-thinking planners shaping the future of the profession

You don’t have to leap.

You just have to look.

Start by exploring the pathway and seeing whether it aligns with the planner you feel called to become.

The bridge is open.