Why Success Today Can Blind You to Opportunity Tomorrow

There’s a pattern emerging across the advice profession right now that deserves thoughtful attention — not alarm, not hype, just clarity.

In recent conversations with advisers internationally, one theme keeps surfacing:

many advisers are earning more than ever and working less than before — so change feels unnecessary.

That’s understandable. When a model is rewarding you, questioning it feels irrational.

But professional evolution rarely begins with dissatisfaction.

It begins with awareness.

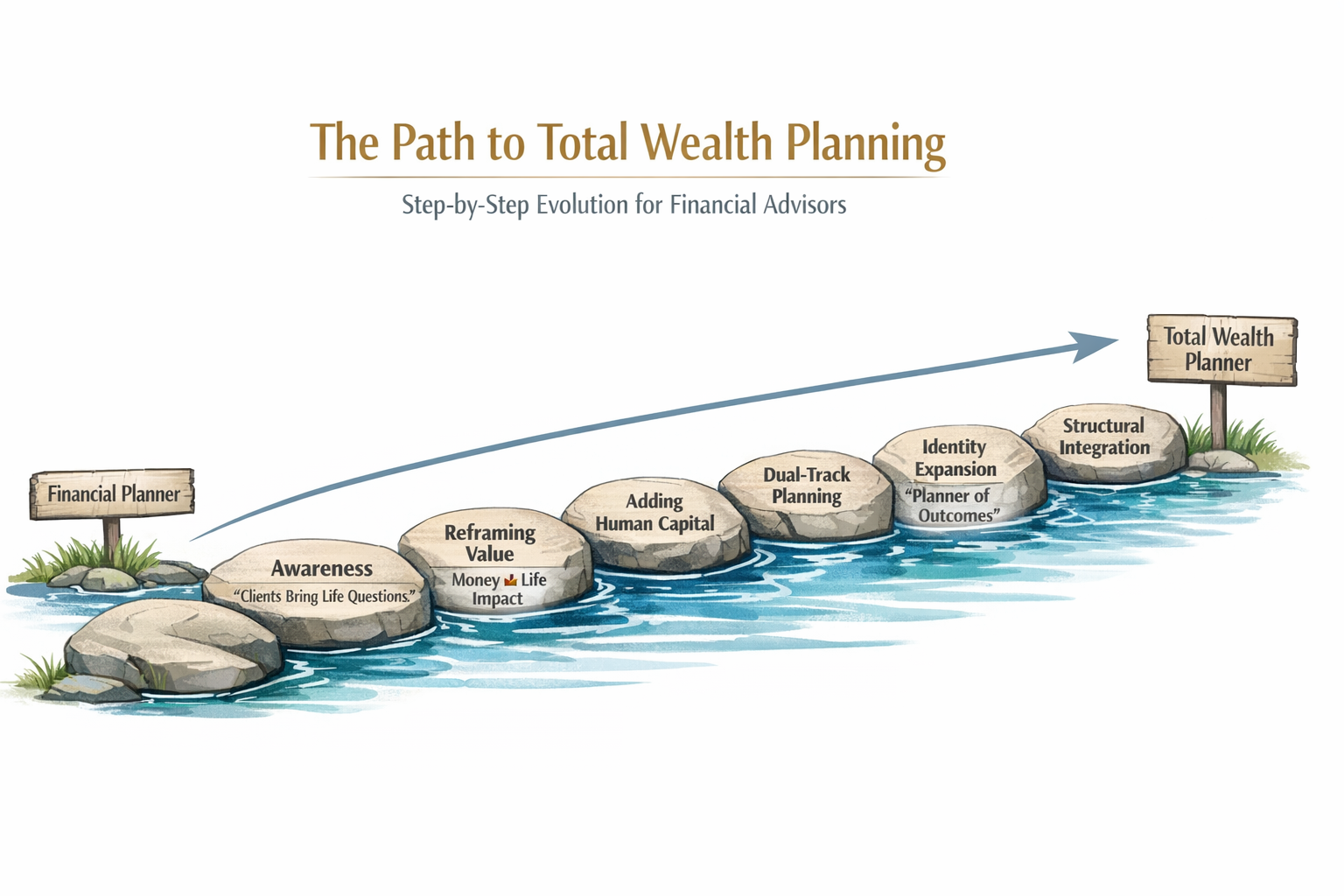

So instead of talking about transformation as a leap, let’s walk through the stepping-stones — the natural progression advisers move through as they expand from financial planner to Total Wealth Planner.

Not a jump. A path.

Stepping Stone 1 — Success Recognition

“Things are working. Why change?”

If you’re thriving right now, that’s not a weakness. It’s evidence you’ve built real skill.

Strong markets in recent years have lifted assets under management and adviser income. Many professionals feel — quite reasonably — that the current model is validated.

This is not denial.

It’s data.

The key insight at this stage is simple:

Success confirms what works today.

It does not guarantee relevance tomorrow.

No action required yet. Just awareness.

Stepping Stone 2 — Pattern Noticing

Seeing the signals others dismiss

At this stage advisers begin noticing subtle shifts:

- clients asking broader life questions

- AI tools performing technical tasks faster

- younger clients expecting different conversations

- consolidation changing firm economics

None of these individually force change.

But together they form a pattern.

Professionals who advance aren’t reacting.

They’re observing.

Stepping Stone 3 — Reframing the Profession

From product expert → decision partner

Here the shift is conceptual, not operational.

The realisation:

Clients don’t just need portfolio optimisation.

They need life optimisation.

This doesn’t replace financial planning.

It contextualises it.

Financial capital becomes one resource among many.

Stepping Stone 4 — Expanding the Planning Lens

Adding Human Capital

Traditional planning focuses on:

- investments

- tax

- retirement income

- estate structures

Total Wealth Planning adds:

- earning potential

- adaptability

- decision patterns

- resilience

- life direction

Research consistently shows that for most individuals, human capital is their largest asset.

Ignoring it doesn’t simplify planning.

It distorts it.

Stepping Stone 5 — Dual Competence

Technical expertise + behavioural leadership

At this point advisers notice something powerful:

Clients don’t struggle most with calculations.

They struggle with decisions.

This is where the adviser’s role evolves from:

information provider → thinking partner

Technology handles computation.

Humans handle meaning.

That distinction is the future of the profession.

Stepping Stone 6 — Identity Shift

“What I do” becomes “Who I am professionally.”

The most significant transition is internal.

Not:

I offer new services.

But:

I solve a broader category of problems.

Advisers here begin to see themselves as:

- strategic coordinators

- life-architecture designers

- behavioural stabilisers

- outcome planners

This isn’t a new job title.

It’s a matured professional identity.

Stepping Stone 7 — Total Wealth Planner

The integrated practitioner

At this stage the distinction becomes clear:

| Financial Planner | Total Wealth Planner |

|---|---|

| Optimises assets | Optimises lives |

| Measures returns | Measures outcomes |

| Focuses on money | Focuses on resources |

| Solves transactions | Solves trajectories |

Importantly:

You didn’t abandon financial planning.

You expanded it.

Why Many Advisers Pause Before Crossing

If your income is rising, your clients are happy, and your calendar is manageable, urgency disappears. That’s human nature.

As one adviser observed, when earnings increase significantly, the natural reaction is:

“Why would I change my business model?”

That question is rational.

But history shows something consistent across professions:

The biggest shifts rarely happen when change feels urgent.

They happen when change feels unnecessary.

The Real Opportunity

The future isn’t a battle between advisers and technology.

It’s a division of labour.

Technology

- calculates

- aggregates

- models

- summarises

Humans

- interpret

- prioritise

- motivate

- guide

The profession isn’t disappearing.

It’s specialising.

The Invitation

If you’re reading this and thinking:

“I’m not there yet.”

Good.

You’re not supposed to be.

This isn’t a bridge you must cross today.

It’s a path you can step along at your own pace.

Most advisers are already on it.

They just haven’t named the steps yet.

Final Thought

The advisers who thrive in the next era won’t be the fastest to adopt tools.

They’ll be the clearest about their role.

Tools change.

Human needs don’t.

Total Wealth Planning isn’t a new profession. It’s financial planning — fully evolved.

Clear real-world cases where leaders delayed change because things were still working — and that delay proved decisive.

1) Kodak — Invented the Future, Ignored It

Situation:

Kodak actually invented the digital camera in 1975.

Why they didn’t act:

Film sales were booming. Profit margins were enormous. There was no urgency.

Leadership logic at the time:

Why disrupt a wildly profitable business?

Outcome:

Digital photography eventually replaced film entirely. Kodak filed for bankruptcy in 2012.

Lesson:

Success delayed adaptation.

2) Blockbuster — Dominant Until Overnight Irrelevant

Situation:

Blockbuster dominated home entertainment in the early 2000s.

Why they didn’t act:

Late fees alone generated hundreds of millions annually. The model looked unstoppable.

Leadership logic:

Streaming and mail-order rentals are niche. Stores are our strength.

Outcome:

They dismissed partnership opportunities with Netflix. Within a decade, they were gone.

Lesson:

Market leadership masked structural vulnerability.

3) Nokia — Winning the Race They Didn’t Know Had Changed

Situation:

In 2007 Nokia controlled ~50% of the global mobile phone market.

Why they didn’t act:

Sales were strong. Market share was dominant. Their phones were everywhere.

Leadership logic:

We’re already winning. Why redesign the model?

What they missed:

The iPhone didn’t just change phones.

It changed what a phone was.

Outcome:

Within five years, their dominance collapsed.

Lesson:

They optimised the old game while the game itself changed.

4) Banking Analogy Relevant to Advisers

Before online banking:

- branch traffic was high

- profits were stable

- customers seemed loyal

So many banks delayed digital investment.

Today:

- most transactions are digital

- branches are closing globally

- fintech firms set expectations

Again, the pattern:

Stability delayed transformation.

The Pattern Behind All These Cases

Across industries, leaders don’t resist change because they’re foolish.

They resist because:

- the current system is rewarding them

- risks seem theoretical

- signals appear early but weak

In behavioural economics this is called:

Success bias — when current success convinces us current methods are permanent.

Why This Matters Professionally Today

The lesson isn’t “change immediately.”

It’s:

When everything feels fine, that’s when strategic thinking matters most.

Urgency forces reaction.

Comfort requires foresight.

✅ Simple rule of thumb

| If you feel… | You should ask… |

|---|---|

| Threatened | How do I respond? |

| Comfortable | What am I not seeing yet? |

⭐ Insight worth keeping

History’s biggest professional disruptions rarely surprise observers.

They surprise participants.

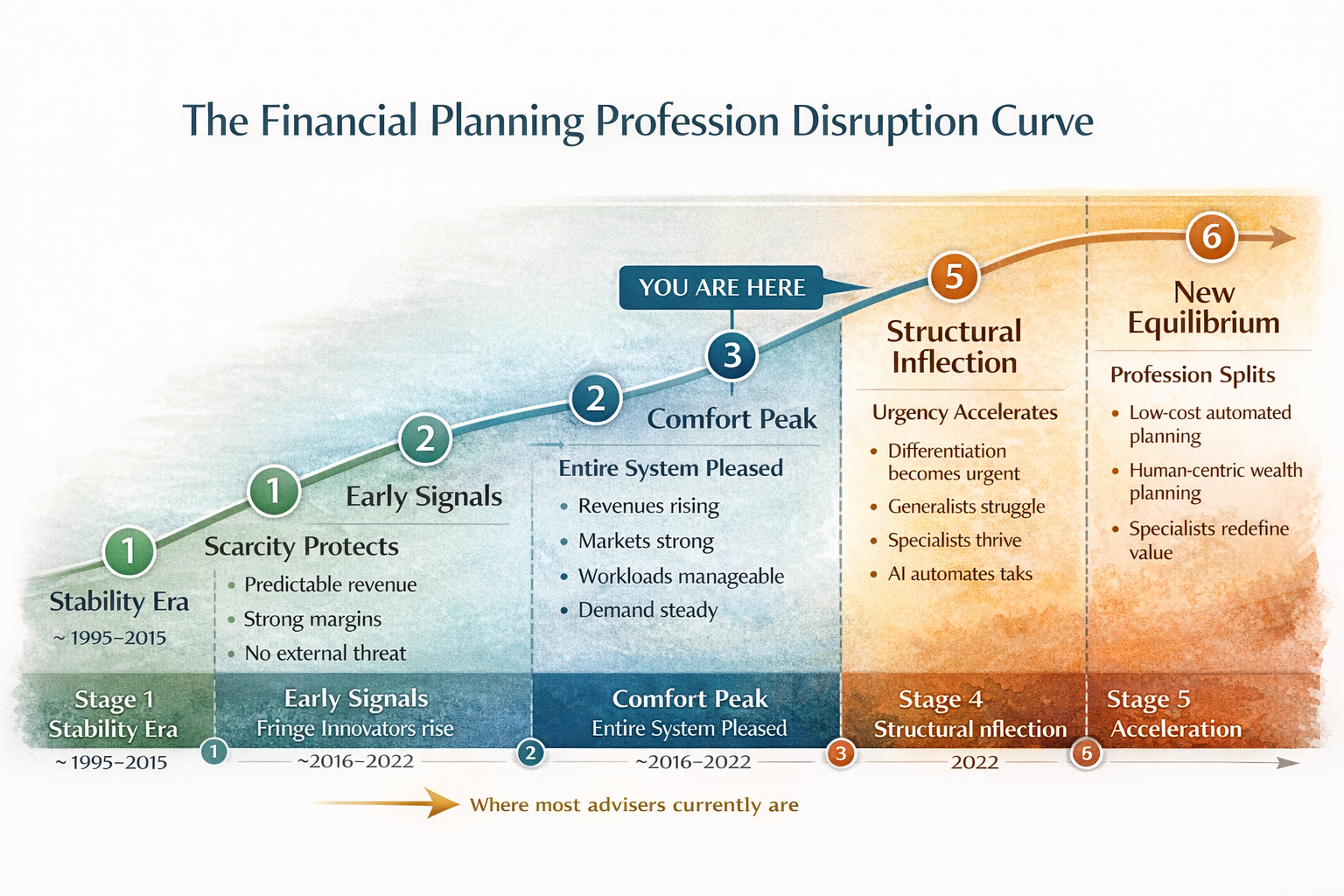

The Disruption Curve — Where Financial Planners Likely Sit Today

Stage 1 — Stability Era (Already Passed)

What it looks like

- predictable revenue

- strong margins

- clear value proposition

- little external threat

Financial planning equivalent (1995–2015)

- product expertise was scarce

- information asymmetry favoured advisers

- clients needed gatekeepers

Profession status: essential intermediary

Stage 2 — Early Signals (Also Passed)

Indicators

- new tools appear

- fringe innovators experiment

- incumbents dismiss change

Financial planning equivalent (2016–2022)

- robo-advisers emerge

- fintech platforms rise

- behavioural finance gains traction

- clients access research directly

Industry reaction:

“Interesting… but niche.”

Profession status: confident incumbent

Stage 3 — Comfort Peak (Where Most Advisers Are Now)

This is the most deceptive stage.

Visible reality

- revenues rising

- markets strong

- workloads manageable

- demand steady

As one adviser noted recently:

many advisers are making more money while working less. DavidC_SteveC_Transcript_170226

Hidden reality

- AI can already perform large parts of technical work

- client expectations are shifting

- younger generations want different relationships

Psychological state of industry:

No problem exists.

Profession status: successful but exposed

Stage 4 — Structural Inflection (Beginning Now)

This is the turning point phase.

Signals

- sudden valuation drops in legacy firms

- consolidation accelerates

- new entrants scale fast

- pricing pressure emerges

Not collapse — re-pricing of value.

Key dynamic:

Technology doesn’t eliminate advisers.

It eliminates tasks advisers used to charge for.

Profession status: redefinition phase

Stage 5 — Acceleration (Next 2–5 Years Likely)

Historically, once industries hit this stage:

- differentiation becomes urgent

- generalists struggle

- specialists thrive

- identity shifts

Advisers who remain purely technical compete with software.

Advisers who expand into human-centric roles become more valuable.

Profession status: divergence

Two paths form.

Stage 6 — New Equilibrium (Future State)

Every disrupted profession eventually stabilises again — but with a different structure.

Likely future model:

| Old Value | New Value |

|---|---|

| knowing products | knowing people |

| calculating plans | guiding decisions |

| selling solutions | designing lives |

| managing money | managing outcomes |

Profession status: strategic partner

The Critical Insight

Industries don’t change when technology appears.

They change when behaviour shifts.

Technology is already here.

Behaviour is just starting to move.

That means we are not at the start of disruption.

We are at the recognition phase.

Where the Opportunity Actually Lies

Historically, the biggest winners are not:

- early adopters

- or late adopters

They’re the ones who move during the comfort phase — before urgency forces everyone else to act.

Because at that point:

- competition is low

- resistance is high

- differentiation is easy

✅ Plain-English positioning

Financial planning isn’t about to disappear.

It’s about to split.

Into:

- automated planning

- human planning

The future belongs to professionals who operate in the second category.

⭐ Strategic takeaway

The riskiest time to change is when you have to.

The smartest time is when you don’t.

Ready to Step Across the Bridge?

If you’re sensing that traditional planning is no longer enough for the clients you truly want to serve, that instinct is worth paying attention to.

The next evolution of your professional journey is not about abandoning what you know. It’s about expanding it — integrating human capital, behavioural insight, and life architecture into the financial planning framework you already understand.

The Academy of Life Planning invites you to explore that transition.

Across the bridge you’ll discover:

- A proven framework for integrating human and financial capital

- A professional pathway to becoming a Total Wealth Planner

- Tools that deepen client outcomes and professional fulfilment

- A global community of forward-thinking planners shaping the future of the profession

You don’t have to leap.

You just have to look.

Start by exploring the pathway and seeing whether it aligns with the planner you feel called to become.

The bridge is open.