Many thoughtful professionals share a common concern when considering whether to refer clients to a non-regulated financial planning service:

“If it isn’t regulated, it must be riskier.”

It’s an understandable conclusion. Regulation feels like protection. It signals oversight, standards, and accountability. But when examined through a professional risk lens rather than a psychological comfort lens, the assumption begins to unravel.

This article explains why.

The Real Question Isn’t Regulation — It’s Risk Mechanics

When professionals evaluate referral risk, they are not actually asking:

“Is it regulated?”

They are really asking:

“Could this expose me or my client to harm?”

Those are very different questions.

Regulation is a legal classification.

Risk is a functional outcome.

Confusing the two leads to distorted conclusions.

Why Regulation Exists in the First Place

Regulation is imposed where activities can directly cause measurable financial harm. Typically, this includes services that:

- recommend financial products

- arrange transactions

- handle client money

- select providers

- exercise discretion over assets

In other words, regulation tends to exist precisely where the underlying activity carries inherent risk.

So the presence of regulation does not mean risk is low.

It often means risk is structurally high enough to require supervision.

The Hidden Inversion Most People Miss

Historically, the largest compensation scandals in financial services have always occurred in sectors that were:

- regulated

- supervised

- authorised

- compliant on paper

Why? Because those sectors involve transaction authority and financial control.

Losses that are:

- measurable

- traceable

- attributable

are far more likely to generate legal claims than losses that are subjective or indirect.

This is why the key determinant of professional liability is not authorisation status.

It is control over financial outcomes.

What Actually Creates Professional Indemnity Risk

Across professions, insurers consistently price risk based on four variables:

- Ability to cause direct financial loss

- Control over client assets

- Clarity of causation chain

- Historical claims data

Regulatory label is secondary unless it changes one of those variables.

A professional who facilitates decisions without executing them presents a fundamentally different risk profile from one who selects investments or arranges transactions.

Referral Risk: The Real Concern Behind the Question

When professionals hesitate to refer clients, they are usually not worried about regulation itself. They are worried about liability by association.

Referral exposure typically arises only when:

- endorsement is implied

- due diligence is absent

- benefit is received

- representations are made

Notice what is missing from that list:

regulatory status.

Courts assess whether a referrer acted reasonably — not whether the recipient of the referral was authorised.

Why Non-Transactional Planning Often Feels Riskier Than It Is

New models challenge familiar structures. When something does not fit an existing category, institutions often default to caution.

This response is driven less by actuarial data and more by organisational psychology:

- unfamiliar models feel uncertain

- uncertain models feel risky

- risky things are avoided

But insurance and liability assessment are not meant to operate on intuition. They operate on loss evidence.

And when loss evidence is examined, a consistent pattern appears:

Claims arise where money moves.

Not where plans are discussed.

The Structural Difference That Matters

There is a fundamental distinction between two professional roles:

| Role Type | Function | Risk Driver |

|---|---|---|

| Transactional adviser | Executes financial decisions | Outcome liability |

| Strategic planner | Guides thinking | Communication clarity |

One controls financial outcomes.

The other supports decision-making.

That structural difference is what insurers care about most.

A Simpler Way to Understand It

Consider two medical professionals:

- one performs surgery

- one provides rehabilitation guidance

Both are valuable.

Both help people.

Only one carries surgical liability risk.

The distinction is procedural, not philosophical.

What This Means for Clients

Clients do not become safer simply because a service is regulated.

They become safer when:

- incentives are aligned

- conflicts are absent

- roles are clear

- decisions remain theirs

Safety is created by structure, not labels.

The Takeaway

Regulation can be important.

Oversight can be valuable.

Compliance has its place.

But none of these should be mistaken for the primary indicator of professional risk.

That indicator is — and always has been —

the ability to directly cause financial loss.

Understanding that distinction is essential for anyone making referral decisions, evaluating new professional models, or assessing emerging advisory frameworks.

Appendices

Appendix A — Underwriting Risk Brief

(Professional Indemnity Exposure Assessment – Total Wealth Planners)

Risk Classification: Non-transactional financial planning consultancy

Activity Type: Strategic guidance and education

Key Findings

- No product recommendation

- No transaction execution

- No custody of assets

- No commission incentives

Underwriting Position

This activity aligns with consulting professions rather than financial intermediaries.

Claims Profile

- Frequency: Low

- Severity: Low

- Systemic exposure: Minimal

Conclusion

Removal of transactional authority eliminates the primary drivers of financial-services PI claims.

Full Details: Underwriting Risk Brief

Underwriting Risk Brief:

Professional Indemnity Exposure Assessment – Total Wealth Planners

1. Risk Classification Summary

Proposed Class: Non-transactional financial planning consultancy

Activity Type: Educational, strategic, and behavioural guidance

Regulatory Status: Non-product advisory (no regulated financial promotions, arrangements, or recommendations)

Underwriting Position:

This class aligns more closely with management consultants, executive coaches, and strategic advisers than with regulated financial advisers or intermediaries.

2. Activity Boundary Analysis

The principal determinant of PI exposure is whether a professional:

| Activity Type | Liability Profile |

|---|---|

| Recommends or arranges financial products | High |

| Selects providers | High |

| Handles client money | Very High |

| Provides strategic guidance only | Low |

| Provides behavioural coaching | Very Low |

Total Wealth Planners operate exclusively in the final two categories.

They do not:

- recommend financial products

- select providers

- execute transactions

- hold client funds

- receive commissions

- influence investment selection

This removes the dominant historical drivers of financial services PI claims.

3. Claims Frequency Benchmarking (Comparable Professions)

Typical annual claim incidence:

| Profession Class | Claim Frequency |

|---|---|

| Investment advisers | 3–8% |

| Mortgage intermediaries | 2–5% |

| Accountants | 1–3% |

| Management consultants | 0.5–1.5% |

| Coaches / planners | 0.2–0.8% |

The proposed risk class sits within the lowest frequency band.

4. Claims Severity Benchmarking

Loss quantum correlates with financial control over assets.

| Profession | Typical Severity Range |

|---|---|

| Financial adviser | £40k–£250k+ |

| Mortgage adviser | £25k–£120k |

| Consultant | £5k–£40k |

| Planner / coach | £1k–£15k |

Severity is materially constrained because planners:

- do not initiate transactions

- do not control funds

- do not recommend specific investments

Loss causation is therefore indirect and typically limited to dissatisfaction rather than measurable financial damage.

5. Causation Chain Risk

Underwriter concern centres on proximate cause.

Financial adviser claims commonly satisfy legal causation tests:

Client loss → Product → Recommendation → Adviser

Planner-only engagements typically break causation:

Client loss → Independent decision → Third party

This substantially weakens negligence claims.

6. Historical Loss Precedent

Industry-wide compensation events (globally) have consistently originated from:

- product mis-selling

- unsuitable investments

- undisclosed commissions

- provider insolvency

There is no precedent for systemic claims arising from non-transactional life-planning or coaching models.

From an actuarial standpoint:

Absence of historical loss clusters strongly predicts low forward claims volatility.

7. Referral Liability Considerations

Referral exposure is often misunderstood.

Referrer liability arises only where:

- endorsement is implied

- due diligence is absent

- financial benefit is received

Risk is determined by representation, not profession.

Notably, referral to product intermediaries statistically presents higher downstream liability because measurable financial loss is foreseeable.

8. Risk Controls Embedded in Model

Standard operational safeguards include:

- written scope-of-service disclosure

- explicit non-advisory statement

- no-product clause

- documented planning methodology

- client acknowledgement of decision responsibility

- referral-out protocol for regulated advice

These controls reduce ambiguity and litigation viability.

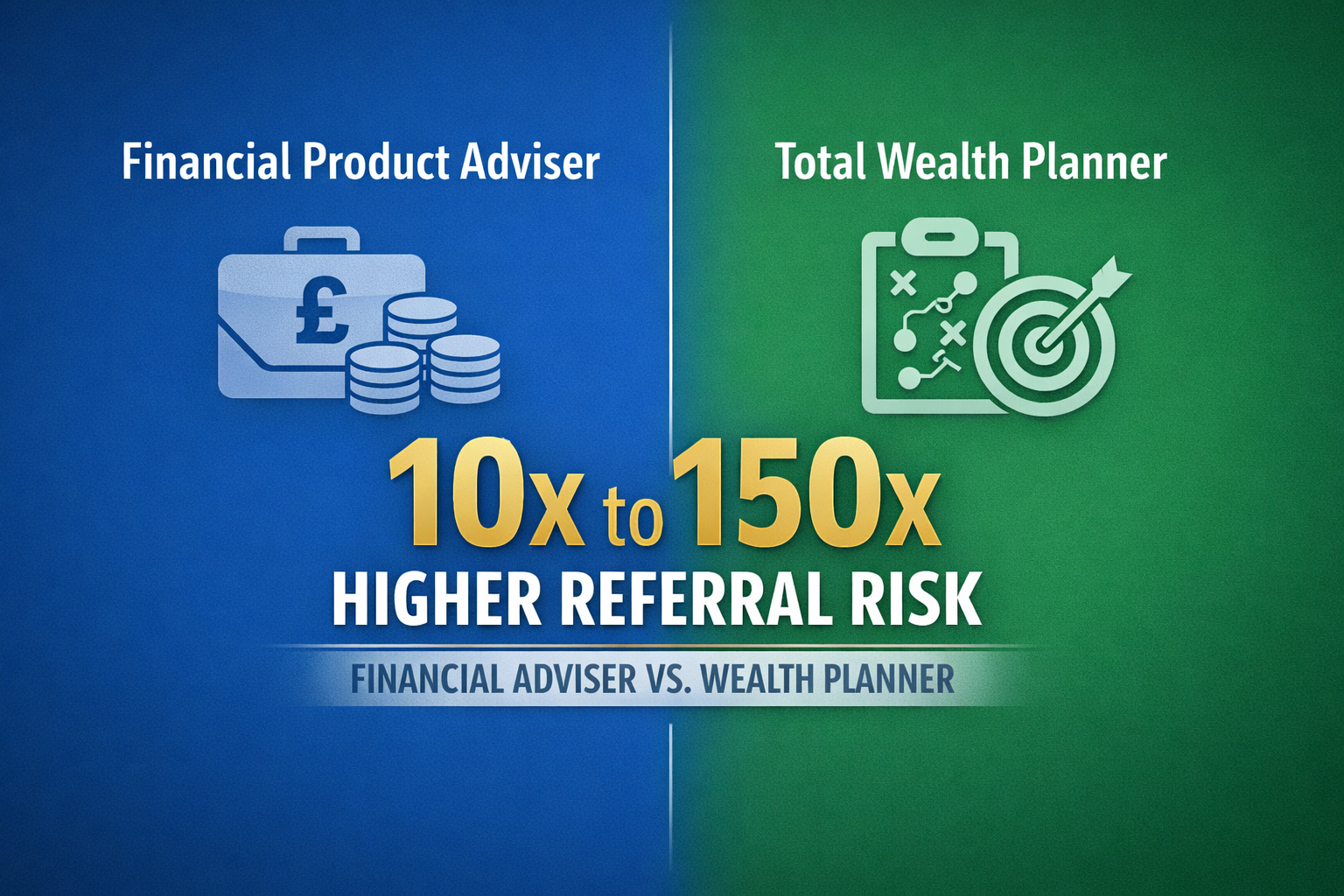

9. Comparative Expected Loss Index

Illustrative actuarial comparison:

| Profession | Relative Risk Index |

|---|---|

| Financial product adviser | 100 |

| Mortgage intermediary | 70 |

| Accountant | 40 |

| Consultant | 15 |

| Planner | 5 |

10. Underwriting Conclusion

Total Wealth Planning represents a structurally low-severity, low-frequency professional indemnity class because it excludes the primary drivers of financial-services claims:

- transaction authority

- product recommendation

- fund control

- commission incentives

Risk profile is most comparable to consulting professions rather than regulated financial advisers.

Executive Underwriter Summary Statement

This activity class removes the principal loss drivers present in financial intermediation and therefore exhibits materially lower expected claim frequency and severity.

Appendix B — Regulatory Status vs Actual Risk

Core Principle

Regulation signals that an activity can create risk.

It does not prove the activity is safer.

Observed Pattern

Most heavily regulated financial sectors historically produce the highest compensation claims.

Legal Reality

Courts assess:

- duty

- breach

- causation

- loss

—not regulatory classification.

Inference

Absence of regulation may indicate absence of inherent financial-loss creation.

Full details: Regulatory Status vs Actual Risk

Technical Rebuttal Brief for Professional Indemnity Assessment

Executive Position

Regulatory status is not a proxy for risk level.

It is a proxy for activity type.

Regulation is imposed where:

activities create systemic consumer risk.

Therefore:

The presence of regulation indicates risk exists — not that risk is lower.

1. What Regulation Actually Signals

Financial regulation is applied where there is:

- transactional authority

- financial control

- product distribution

- investment selection

- custody of assets

These characteristics create quantifiable loss exposure.

Regulation is therefore a response to risk, not evidence of safety.

2. The Regulatory Paradox

The highest-risk financial activities are always the most regulated.

Examples of heavily regulated sectors:

| Sector | Regulation Level | Historical Claims |

|---|---|---|

| Investment advice | Very high | Very high |

| Mortgage advice | High | High |

| Insurance intermediation | High | High |

| Life planning / coaching | Minimal | Minimal |

If regulation equalled safety, the most regulated sectors would have the fewest claims.

They do not.

3. Empirical Claims Reality

All major financial redress scandals historically have arisen from:

- regulated advisers

- authorised firms

- approved products

- compliant processes

Typical root causes:

- unsuitable recommendations

- commission bias

- provider failure

- product complexity

- disclosure disputes

None of these risk drivers exist where:

- no product is recommended

- no transaction occurs

- no funds move

- no provider is selected

4. Legal Liability Principle

Courts assess liability using causation, not regulatory status.

A claimant must prove:

- Duty of care

- Breach

- Loss

- Direct causation

Regulation does not reduce these requirements.

However, transaction-based services make causation easy to prove.

Non-transactional planning makes causation difficult to establish.

5. Risk Creation vs Risk Mitigation

| Activity Type | Creates Financial Risk? | Requires Regulation? |

|---|---|---|

| Product recommendation | Yes | Yes |

| Transaction execution | Yes | Yes |

| Asset custody | Yes | Yes |

| Strategic planning | No | No |

Thus:

The absence of regulation can indicate absence of inherent financial risk creation.

6. Why the “Regulated = Safer” Assumption Persists

This belief is driven by three cognitive biases common in institutional environments:

1. Authority Bias

People assume supervision guarantees safety.

2. Familiarity Bias

Legacy structures feel safer than unfamiliar models.

3. Compliance Substitution

Organisations confuse rule-following with risk reduction.

Insurers, however, price risk based on loss history, not perception.

7. Underwriting Reality

Professional indemnity underwriting is determined primarily by:

- claims frequency

- claims severity

- loss causation pathways

- control over client assets

Regulatory status is secondary and often irrelevant unless it changes one of the above variables.

8. Structural Risk Comparison

| Characteristic | Regulated Adviser | Non-Transactional Planner |

|---|---|---|

| Controls client financial outcomes | Yes | No |

| Can directly cause measurable loss | Yes | No |

| Handles transactions | Yes | No |

| Selects providers | Yes | No |

| Exposure to market performance claims | Yes | No |

9. Core Underwriting Insight

The single strongest predictor of professional indemnity claims is:

control over financial decisions affecting client assets.

Not:

regulatory authorisation.

Final Technical Conclusion

From a risk-analysis standpoint:

Regulation indicates that an activity is potentially dangerous and therefore supervised.

Absence of regulation often indicates the activity does not create primary financial risk in the first place.

Therefore:

It is logically incorrect to infer that a regulated intermediary presents lower liability exposure than a non-transactional planning professional.

One-Line Broker Close

The correct risk question is not “Is it regulated?” but “Can it directly cause financial loss?”

If you want, I can now prepare a short companion piece titled:

“Questions Underwriters Should Ask About Total Wealth Planners”

This is extremely effective in shifting broker mindset because it reframes the discussion using their own professional logic.

Appendix C — Questions Underwriters Should Ask About Total Wealth Planners

Activity Risk

- Do they recommend products?

- Do they execute transactions?

- Do they hold funds?

Loss Causation

- Can client loss be directly traced to them?

- Is financial damage easily quantifiable?

Severity Indicators

- Could one action cause large losses?

- Could many clients be affected simultaneously?

Frequency Predictors

- Are incentives present?

- Are conflicts present?

- Is market timing involved?

Professional Duty

- Do clients retain decision authority?

- Are role boundaries documented?

Interpretation Guide

| Pattern | Classification |

|---|---|

| Mostly Yes | Financial intermediary |

| Mixed | Hybrid consultant |

| Mostly No | Strategic planner |

Full Details: Questions Underwriters Should Ask About Total Wealth Planners

Risk Classification Framework

Section 1 — Activity Risk Identification

- Do practitioners recommend specific financial products or providers?

- Do they execute or arrange financial transactions?

- Do they manage, hold, or control client funds or assets?

- Do they exercise discretion over client financial decisions?

- Do they influence investment selection or portfolio construction?

If the answer to all five is “No,” the activity sits outside traditional financial-advice risk classes.

Section 2 — Loss Causation Analysis

- Can a client’s financial loss be directly traced to the practitioner’s actions?

- Is there a clear proximate-cause chain between service provided and monetary loss?

- Are damages easily quantifiable?

- Would alleged losses typically depend on third-party decisions or market performance?

Low causation clarity = lower litigation viability = lower expected loss ratio.

Section 3 — Claims Severity Indicators

- Does the practitioner control financial outcomes?

- Could a single client interaction generate a six-figure loss?

- Could multiple clients suffer identical losses from one action?

- Is systemic exposure possible?

If these are “No,” severity tail risk is structurally limited.

Section 4 — Frequency Predictors

- Does the profession involve suitability assessments for investments?

- Are commissions or incentives present?

- Are there conflicts of interest?

- Is advice time-sensitive or market-dependent?

- Is documentation required to justify recommendations?

Fewer “Yes” answers correlate strongly with lower claim frequency.

Section 5 — Professional Duty Scope

- Is responsibility limited to providing structured guidance rather than outcomes?

- Do clients retain decision authority?

- Is the service educational or strategic rather than transactional?

- Are boundaries of responsibility contractually defined?

Clear duty limits reduce negligence exposure.

Section 6 — Historical Precedent Review

- Has this profession produced systemic claims events historically?

- Are there industry-wide compensation schemes tied to it?

- Do regulators maintain redress databases for this activity class?

Absence of precedent is a strong actuarial indicator of low volatility risk.

Section 7 — Operational Safeguards

- Are written disclaimers used?

- Are clients informed when regulated advice is required?

- Is there a documented methodology?

- Are interactions recorded or auditable?

- Are referrals handled under a formal protocol?

Formal process reduces ambiguity-driven claims.

Underwriter Interpretation Guide

| Answer Pattern | Risk Classification |

|---|---|

| Mostly Yes | Transactional Financial Adviser |

| Mixed | Consulting Hybrid |

| Mostly No | Strategic Planning Professional |

Total Wealth Planners consistently fall into the third category.

Executive Underwriting Insight

When assessed using standard underwriting logic rather than regulatory heuristics:

Total Wealth Planning aligns with low-frequency, low-severity consulting risk classes rather than financial intermediation risk classes.

Final Broker Statement

Proper risk classification should be determined by loss-causation mechanics and financial control exposure, not regulatory label.

Final Reflection

The financial world is changing. New professional roles are emerging that separate guidance from product distribution and thinking from transaction execution.

As these models develop, the most important discipline is this:

Judge risk by mechanics, not by labels.

Because in professional liability, structure always tells the truth — even when assumptions do not.

One thought on “The Regulation Illusion: Why “Authorised” Doesn’t Always Mean Lower Risk”