Imagine working hard your entire life, diligently saving for retirement, only to realise that a significant portion of your investment returns is quietly being absorbed by wealth management fees. It’s a reality for many investors who entrust their financial future to traditional wealth managers, often without fully understanding the long-term impact of fees on their wealth. But there’s another way—one that puts you in control, maximises your returns, and ensures your money is truly working for you.

The Hidden Cost of Wealth Management Fees

We recently examined a revealing study by EY, which showed that all major UK wealth management firms charge over 2% per annum in total fees. Some even take as much as 3.2% per annum. That may not sound like much, but over time, these fees quietly erode the value of your portfolio. When we compare this with the widely accepted 4% safe withdrawal rule, which assumes a real return (after inflation) of 4% per year, it becomes clear: wealth managers are taking the majority of your profits.

Think about that for a moment. Your investments might be working hard, but the lion’s share of the gains is going to your wealth manager—not to you.

A Smarter Alternative: The Low-Cost Passive Investment Route

In today’s world, you don’t need a wealth manager to access high-quality investment opportunities. A globally diversified, auto-rebalancing portfolio—a blend of 50-75% equities and 25-50% bonds—is available through passive investment platforms for as little as 0.25% per annum in management fees.

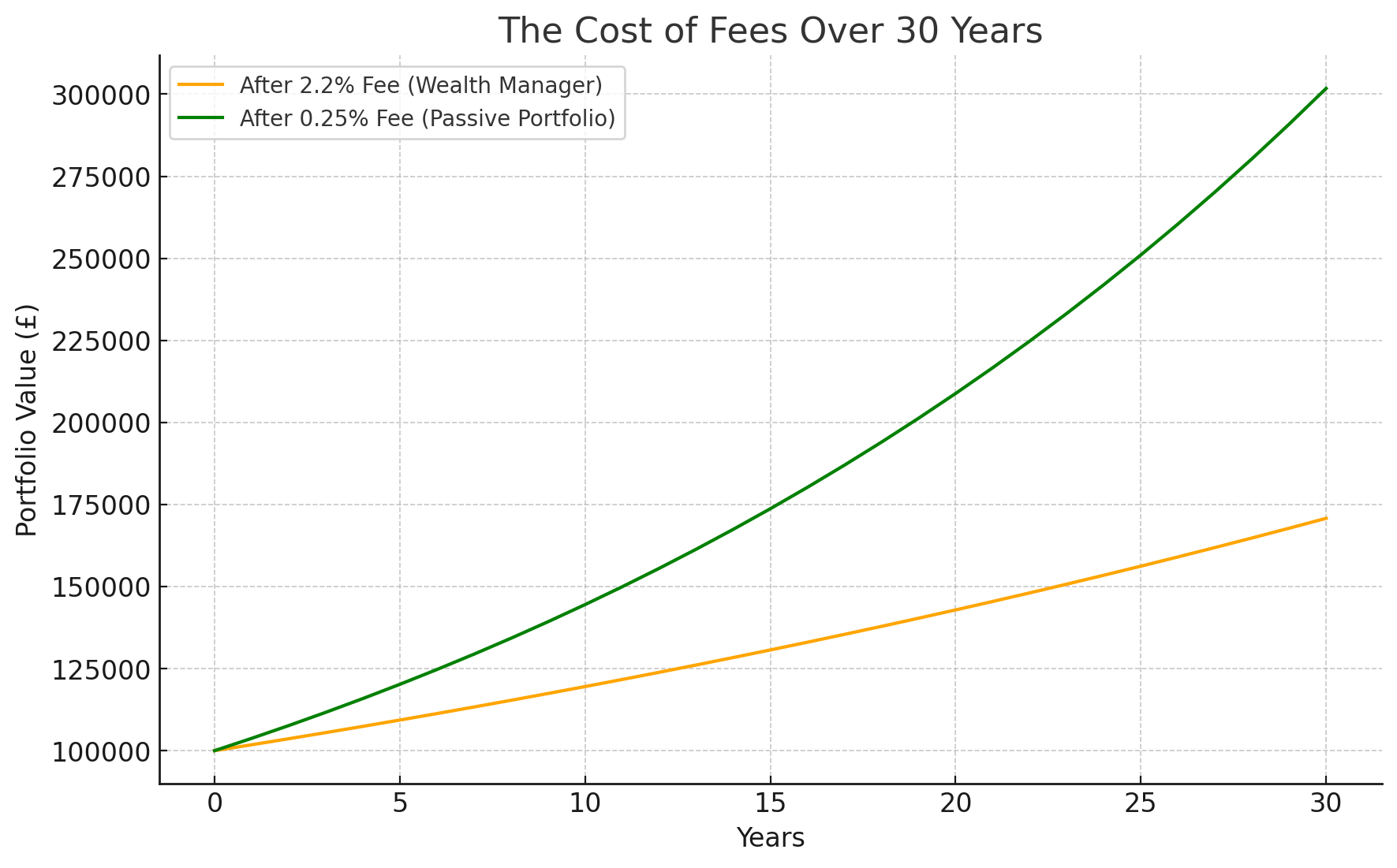

We modelled what happens over 30 years with two different investors:

- Investor A: Uses a traditional wealth manager with 2.2% fees.

- Investor B: Uses a low-cost passive portfolio with 0.25% fees.

Here is a graphical representation of the impact of fees over 30 years, comparing a Wealth Manager Portfolio (2.2% fees) and a Passive Portfolio (0.25% fees).

Key Takeaways:

- The Passive Portfolio (green line) grows significantly more over time due to lower fees.

- The Wealth Manager Portfolio (orange line) accumulates much less wealth due to the compounding effect of higher fees.

- Over 30 years, the difference in portfolio value is substantial, reinforcing how fees can erode investment returns.

The result? Investor B ends up with significantly more money, simply because less is being siphoned off in fees. That’s the power of keeping costs low—your returns compound for you, not someone else.

Why Being a Self-Directed Investor Empowers You

Many people delegate investment decisions because they feel finance is too complex. But the truth is, you don’t need a finance degree or years of experience to manage your money well. Modern investing platforms make it easier than ever to build a diversified portfolio with minimal effort.

Here’s what self-directed investing offers:

✅ Lower Costs – More of your returns stay in your pocket.

✅ Transparency – You know exactly where your money is and what it’s doing.

✅ Simplicity – Automated, passive investing strategies require little time commitment.

✅ Control – You’re no longer reliant on wealth managers who may have their own interests at heart.

✅ Better Long-Term Outcomes – By avoiding high fees, your wealth grows more efficiently over time.

The Shift Towards Financial Freedom

Being in charge of your investments doesn’t mean you have to do everything alone. There are excellent resources, educational platforms, and financial life planners who can guide you in making informed, confident decisions—without the conflicts of interest often seen in traditional wealth management.

The reality is simple: the more you pay in fees, the less wealth you build for yourself. By choosing a low-cost, self-directed approach, you take ownership of your financial future and ensure your money is truly working in your best interests.

Take Action: Start Building Your Wealth Today

Making the switch doesn’t have to be overwhelming. Start by exploring passive investing platforms, learning about globally diversified funds, and understanding how small changes—like lowering fees—can lead to a huge difference in your financial future.

You’ve worked hard for your money. Now it’s time to make sure your money is working hard for you. Are you ready to take control?

Contact us to find out more about being your own wealth manager, at the Academy of Life Planning.

Disclaimer:

Investment values can go down as well as up, and past performance is not a reliable indicator of future results. There is no guarantee that any investment strategy or product will achieve its intended outcome. Before making any investment decisions, you should assess your own financial situation and risk tolerance, and consider seeking independent professional planning advice.

The information provided is for general informational purposes only and does not constitute financial, tax, or legal advice. Please be aware that political risks are inherent, as successive governments may alter policies, including the taxation of pensions. Such changes can significantly affect the value of your retirement savings and investment outcomes. Past performance and current tax regimes are not indicative of future results. It is essential to consult with an independent financial planner to ensure that your strategy remains appropriate in light of potential regulatory and policy changes.

Additional notes:

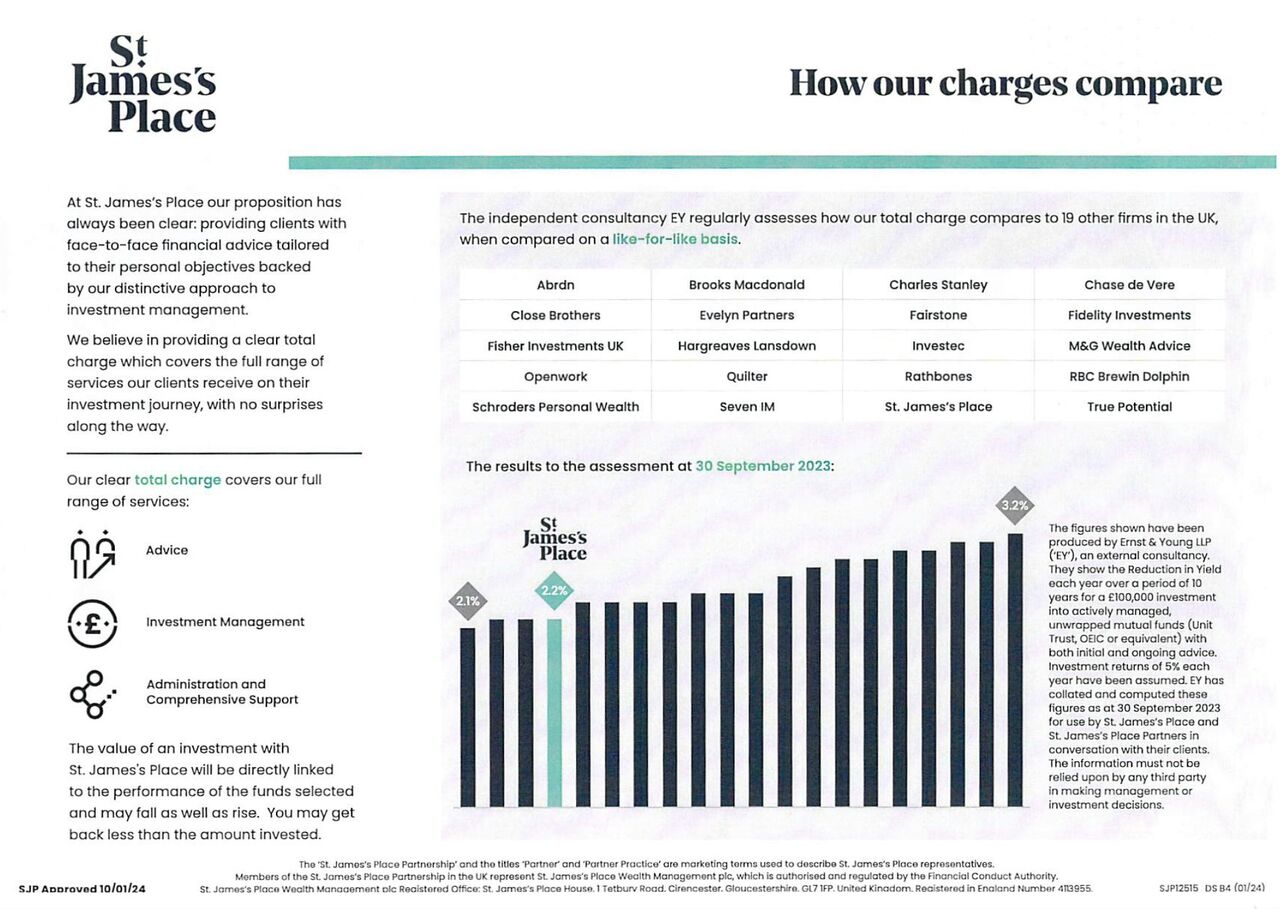

🌟 EY Report on Wealth Management Fees – How Does SJP Compare? 🌟

Transparency and fairness in fees are essential for ensuring clients receive true value in financial advice. That’s why St. James’s Place (SJP) regularly commissions Ernst & Young (EY) to conduct independent assessments of wealth management charges across the UK.

📊 Key Findings:

- The latest EY survey (as of 30 September 2023) shows that SJP’s total charges are just 0.1% per annum higher than the lowest provider assessed.

- The report compares SJP with 19 other firms, including major names like Quilter, Rathbones, and Hargreaves Lansdown.

- SJP’s fees fall at the lower end of the spectrum, with total charges at 2.2% per annum, compared to a high of 3.2% per annum among competitors.

💡 Beyond Fees: The Value Factor

While charges are an important consideration, investment performance is equally—if not more—critical when assessing value for money. Clients should evaluate both factors together when making decisions about their financial future.

🔎 What do you think? Are fees alone a fair way to compare financial advice, or should performance and service quality take precedence? Let’s discuss in the comments!

The 4% safe drawdown theory

The 4% safe drawdown theory, often called the 4% rule, is a widely referenced guideline in retirement planning. It suggests that retirees can safely withdraw 4% of their retirement savings each year, adjusted for inflation, without running out of money over a 30-year period.

Origins of the 4% Rule

The rule was developed by William Bengen, a financial planner, in 1994. Bengen conducted historical analysis of market returns and inflation to determine a sustainable withdrawal rate. He found that 4% was the highest rate that consistently allowed portfolios to last for at least 30 years, even during severe market downturns like the Great Depression.

How It Works

- Initial Withdrawal: In the first year of retirement, withdraw 4% of your total savings.

- Example: If you have £500,000 saved, you withdraw £20,000 in year one.

- Adjust for Inflation: Each subsequent year, you increase withdrawals by the rate of inflation to maintain purchasing power.

- Investment Assumptions: The rule assumes a balanced portfolio of 50-75% equities and 25-50% bonds, providing growth while managing risk.

Criticism and Limitations

- Market Volatility: The rule was based on historical data, but future returns are uncertain. A severe market downturn early in retirement (sequence of returns risk) could deplete savings faster.

- Low Interest Rates: The original study assumed higher bond returns than are available today, making the rule potentially outdated.

- Longevity Risk: If you live beyond 30 years in retirement, the 4% rule might not be sustainable.

- Personal Circumstances: Individual factors like healthcare costs, lifestyle changes, and unexpected expenses can impact the feasibility of the rule.

Modern Adaptations

- Dynamic Withdrawals: Some advisers suggest adjusting withdrawals based on market performance rather than sticking to a fixed 4%.

- Guardrails Approach: Reduce withdrawals in bad market years and increase them in strong market years to extend portfolio longevity.

- Lower Withdrawal Rates: Some suggest 3% or 3.5% might be more appropriate in today’s economic environment.

Final Thoughts

The 4% rule remains a useful starting point for retirement planning but should not be followed blindly. It’s essential to review individual needs, market conditions, and other income sources to create a flexible, personalised drawdown strategy.

The investors “real annual profit” on the portfolio is typically 4%

Yes, the 4% rule is calculated after inflation, meaning it aims to maintain the retiree’s purchasing power over time. However, the rule does not explicitly account for investment fees and charges, which could reduce the effective withdrawal rate.

Breaking It Down:

- After Inflation:

- The 4% withdrawal rate is designed to be a “real” (inflation-adjusted) withdrawal.

- Each year, the withdrawal amount is increased in line with inflation to maintain the retiree’s standard of living.

- Before or After Fees?

- The original 4% rule assumes gross investment returns, meaning fees were not explicitly factored into the calculation.

- If fees are 1% per annum, for example, the net return required for the portfolio to sustain withdrawals would need to be higher than 4%.

- What This Implies About Returns:

- Essentially, the rule assumes that the investor’s portfolio achieves a long-term real return (after inflation) of around 4% per annum.

- Given that typical market returns are higher before inflation, this suggests an assumed nominal return of around 6-7% per annum, depending on historical inflation rates.

Key Takeaways:

- The 4% rule is after inflation but does not fully account for fees.

- If an investor is paying 1-2% in total charges, they may need to adjust withdrawals accordingly (e.g., withdrawing 3% instead of 4% to maintain sustainability).

- The rule implicitly assumes that investment portfolios generate a real return of 4% per year on average, which may not always be achievable depending on market conditions.

All wealth managers surveyed took most of the profit, without exception

Yes, based on the EY survey showing that all wealth managers charge over 2% per annum in fees, and the 4% safe withdrawal rule, the natural conclusion is that wealth managers take most—if not all—of the real investment return.

Breaking It Down:

- Real Annual Profit (after inflation):

- The 4% rule is based on an assumed 4% real return on the portfolio (after inflation).

- Wealth Manager Fees (from the EY survey):

- The lowest total charge was 2.1% per annum.

- The highest was 3.2% per annum.

- St. James’s Place was at 2.2% per annum, near the lower end.

- Impact on Investor Returns:

- If the real return is 4% per annum and fees are 2.1% to 3.2%, then investors are left with only 1.9% to 0.8% real return per year.

- At the higher end of the fee range, fees consume nearly all real returns.

- This significantly reduces the sustainability of retirement withdrawals and long-term wealth growth.

Conclusion:

- All surveyed wealth managers took more than 2% of the portfolio’s annual real return in fees.

- In many cases, this means they absorbed more than 50%—or even close to 100%—of the investor’s real return.

- For investors, this raises serious concerns about value for money, especially when passive investment strategies (e.g., low-cost index funds) often charge less than 0.5% per annum.

Final Thought:

This analysis suggests that many investors using traditional wealth management services may be working harder for their money than their money is working for them. A fee-efficient investment strategy could dramatically improve long-term financial outcomes.

Be Your Own Financial Planner

Create wealth, then save the wealth you’ve created. Choose readily understood, well-diversified, low-cost investments to save money, and we will show you how.

As Christopher Woolard, former CEO of the Financial Conduct Authority, said:

“The overwhelming majority of retail investors are best served by readily understood, well-diversified and low-cost investments which are already available from a range of providers, but many retail investors don’t choose these.”

Source: Call for Input: Consumer investments | FCA

Ever wanted to cut out the middleman and take control of your own financial destiny? Well, guess what? The 2nd edition of Be Your Own Financial Adviser by the brilliant Jonquil Lowe is out now—and it’s here to turn you into your own personal finance guru!

Why pay someone else to manage your money when you can do it better yourself? This book is

packed with all the tools, tips, and tricks you need to navigate the financial jungle like a pro—

because, let’s face it, who knows your money better than you do?