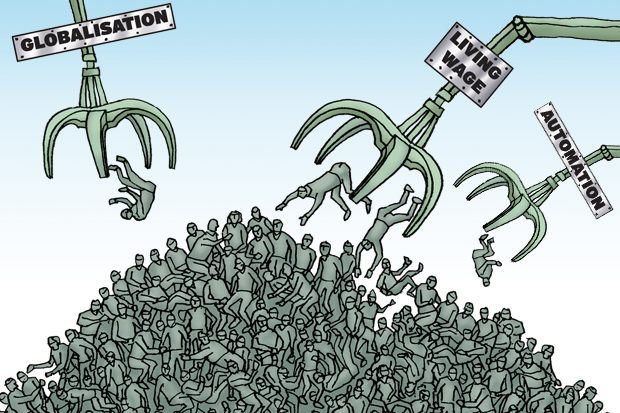

In future, automation, globalisation, living wage constantly throws mid-skilled workers on the scrap heap. Whole industries will obsolesce. People will need to reinvent themselves repeatedly, often involving an intense period of exploration, experimenting, innovating, prototyping, and re-skilling. People must frequently fund these valleys of transformation from savings as they explore exciting possibilities to reinvent themselves through learning cycles.

As financial planners focus on the 5% of the population who are wealthy baby boomers with FPv3.0 for the foreseeable future, what happens to your financial planning business pre-2040, with £6.1 trillion intergenerational wealth transfer to Gen X, Y, & Z.

FPv3.0 goes like this. Accumulate wealth in a job for life for the best part of 40 years on the bet your savings will decumulate to buy you happiness in the last 20 years.

Why does your model need an upgrade?

If ever you want to engage the other 95%, that’s not how life goes.

Half of the people born today will be still alive at age 100.

The savings rate for 40 years to fund 50% final salary for 40 years is 50% of pay, give or take, considering inflation and charges offsetting returns. The unrealistic savings rate will mean that people need to remain economically active for 60 years, or more.

People may run portfolios of work: part-time work, gigs, and own businesses. The cash flow forecast will look less like a single mountain peaking at retirement and more like a whole range of mountains across an entire lifetime.

Due to scientific and technological change acceleration, periods of knowledge significance and work security are shortening. Transitions are more frequent. Not just in work life, but also in our personal life. New relationships. New locations. We need to upskill to stay relevant. We need a continuing life plan.

We need to build savings quickly. The future FPv5.0 may require delivering 2% alpha per month over 40 months rather than 2% alpha per year over 40 years.

Financial products v3.0 are less relevant.

Take pensions. A savings product that delivers 2% alpha per year over 40 years is outmoded. Illiquidity before age 55 is useless — steep drawdowns after 55 tax-inefficient. Annual allowance limitations prevent pots from being replenished as you attempt to climb the following cash flow mountain for the next transformational event in a few years. Lifetime limits are too low to fund a 100-year life. Many will still be working at the age 75 transition, when they take the tax hit.

We need a complete break from the past with different products for a different life journey.

Features of FP v5.0:

- More planning than products.

- “What if scenario” for our possible selves – cash modelling.

- Building savings pots for the multiple valleys.

- Multiple business plans, and foresight about market developments, needed to create assets from meaningful projects throughout a lifetime.

- Products need to be flexible for repeat accumulation/ decumulation, forever accessible, allowing for contribution breaks.

- We need life plans for the intangible assets: health & vitality, knowledge & skills, connections & diverse networks, reputation & brand.

- We need a sense of identity – a life narrative that has coherence, continuity, and causality. We need a path that provides a sense of purpose and integrity for our life. Future stages are more likely to succeed if they are less threatening to our identity. A strong sense of who you are and what you value — continuity in the narrative about past, present, and future.

“The traditional life required only the lightest planning touch and little in the way of reflection since it had certainty and predictability baked into it.” – The 100-year life: Living and working in an age of longevity, by Lynda Gratton and Andrew Scott.

If you want to help people make the right choices, upgrade to FPv5.0 with the Game Plan.

Game plan accreditation is achieved through the Academy of Life Planning mentorship, providing on-the-job coaching and training to preserve competitive advantage.

In association with HapNav, the Happiness navigator.