Product sellers, or product advisers, in general want to plug into your assets and charge a fee. If you have no assets to offer them, they can’t figure out how they are going to get paid. If your assets are a residential property portfolio, for example. And your finances are messy, and you need to figure out your tax liability. They won’t help you.

If you are a reader of “Millionaire Expat: How To Build Wealth Living Overseas”, a book by Andrew Hallam, and you want confirmation that your DIY investment strategy using ETFs and index funds is sensible. They won’t help you.

Those few that will help you may offer you a life plan on a fee-for-service basis, that is some cash flow modelling and tax advice. But they will be burning to run your money for you to plug into your assets and charge their fee. They can’t help themselves but to mention it with pursed lips and a shaking head.

You see, product sellers make poor life planners. Here’s why.

No product creates wealth.

Products manage wealth.

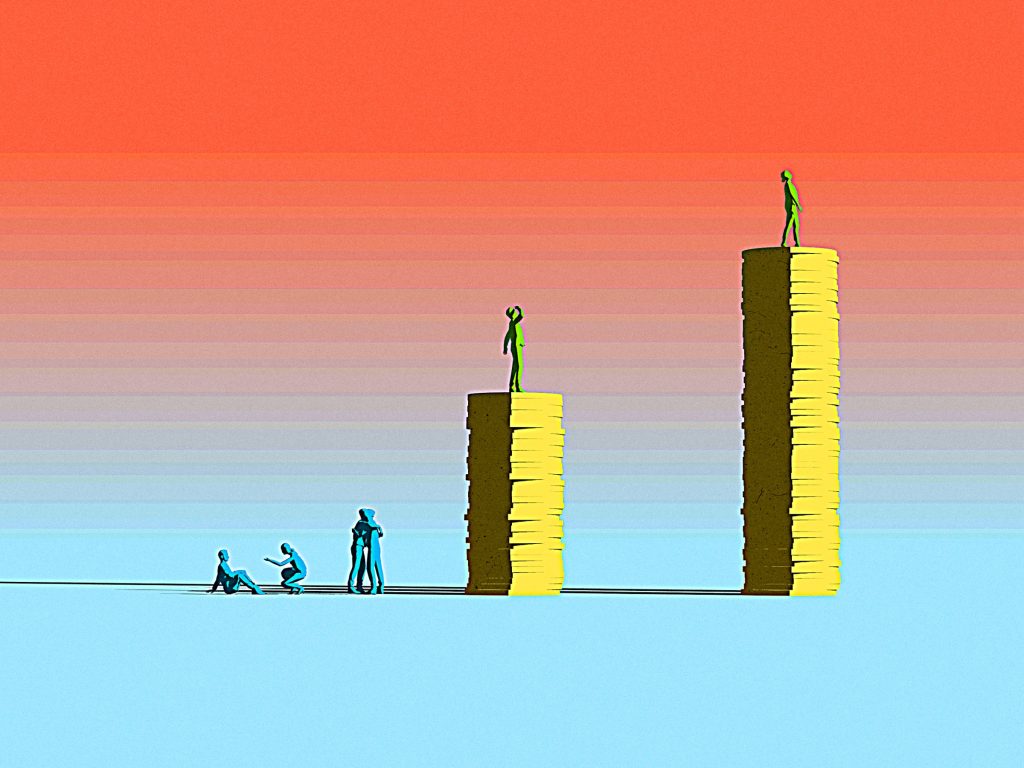

Products are only suitable for the wealthy.

Ask the product seller for their investable asset threshold if you don’t believe me.

You have to be wealthy to begin with, to be a client of a product seller; for them to plug into your assets and charge a fee.

For the wealthy a life plan is merely a plan for how to spend their money.

Now for those who aren’t wealthy, what use is a product seller?

Now take a look at the client adviser, the life planner, the non-intermediating financial planner. They offer a service whereby they can drop into your lifetime cash flow a three-year business plan for the business of you to create wealth.

No product is sold.

Simply, a wealth creation strategy is dropped into the life plan.

Now, the service is extremely useful for those who aren’t wealthy.

Ten years ago, when I graduated with my RLP from the Kinder Institute of Life Planning, I could never figure out how product selling came into the conversation in the Knowledge part of EVOKE. It seemed disconnected.

Here, let’s talk for several meetings about your life. Several meetings in, today we are going to talk about products! Huh!! We called it putting in place the financial architecture to support the life plan. But, here’s the thing …

… the products don’t put in place the financial architecture, the client does.

What I mean by that is, the products run the financial architecture – as one Telegraph reader puts it “for the stupid and rich” – the client’s entrepreneurial spirit and industry puts in place the money.

That’s what is missing.

The adviser should be selling plans, not products.

There should be a wall between advice and product.

Otherwise the life plan is merely a spending plan for the rich and stupid.

There is a case for life planning for the wealthy. But, I’m not sure any fee-driven sales person would see it. For they may not have it within themselves.

Here is the missing point …

The wealthy are self-actualising, as American psychologist Abraham Maslow put it. That is, they are at the point of being the best they can be. Maslow discovered a higher need in the last years of his life. That is self-transcendence. Where you are thinking bigger than yourself, about creating something that will be long remembered after you have passed. A legacy. Making the world a better place for you having lived.

The late Dr. Wayne Dyer called this transition from self-actualisation to self-transcendence, “the Shift”. He said it happened in the afternoon to the evening of our lifetime. Where previously we had pursued wealth and knowledge, past this shift our goals are about service to others.

As Christians put it, “As each has received a gift, use it to serve one another, as good stewards of God’s varied grace.” (1 Peter 4.10).

For the wealthy, the life planner explores life purpose.

Knowing yourself, life becomes worth living.

And death less painful.

Now, this service is extremely useful for those who are wealthy.

As my good friend George Kinder once said:

“There should be a wall, between advice and products, between advice and large institutions, and between our regulators and large institutions. We need an integrity that is impeccable. Until we actually institute a way of bringing good heart, great integrity and a fiduciary relationship that is sustainable into the industry, we are going to fail. We have to make this change, and we have to make it now.”

At the Academy of Life Planning we are faith neutral and faith friendly. We work with different values and perspectives in a respectful and sensitive way.

If you want to become a non-intermediating financial planner contact us today to find out how the Academy of Life Planning can help you.

☎️ 07850 10 20 70

📧 steve@aolp.co

📲 Direct Message