Most financial advisers didn’t enter the profession to sell products.

They entered it to help people make better decisions about their lives.

And yet, many now find themselves constrained — not by their ethics or competence, but by the narrow scope of the system they work within.

This article isn’t a critique of advisers.

It’s an invitation to those who already feel the limits of the current model — and are quietly asking whether there’s a more complete way to serve.

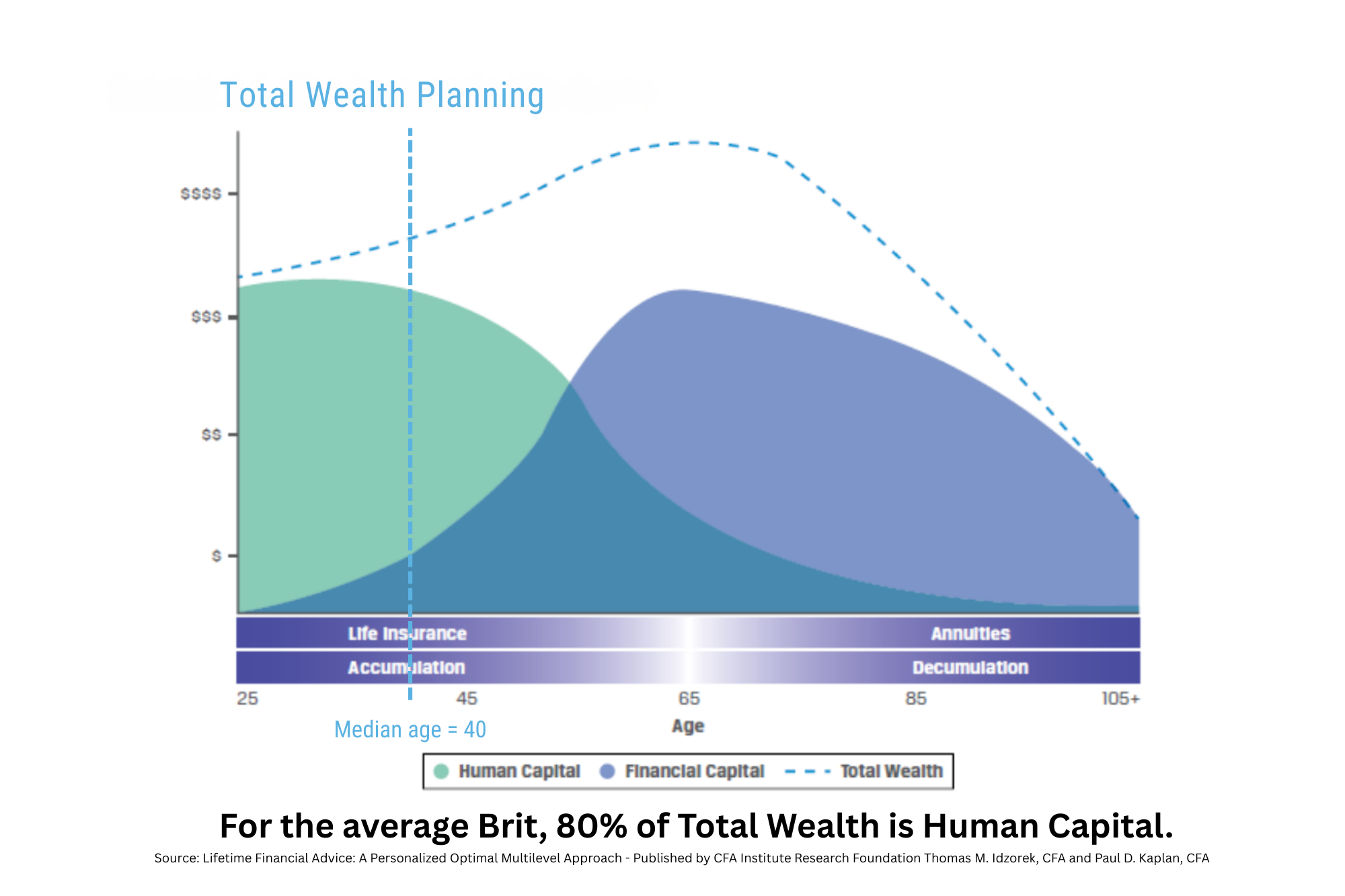

The uncomfortable arithmetic of modern advice

Let’s start with something factual, not ideological.

When we look at the composition of the average Brit’s lifetime wealth, a clear picture emerges:

- Human capital — skills, earning capacity, health, adaptability — makes up the majority

- Financial capital is a much smaller share

- Retail investments, the only area most advisers are authorised to advise on, represent well under 1% of total wealth of the average Brit.

That’s not a judgement on advisers.

It’s a description of a system built around product intermediation, not whole-life decision-making.

The result is a quiet tension many advisers already feel:

“I’m trained to help people — but I’m only allowed to advise on the smallest slice of what actually shapes their life.”

Trust, intention, and structural limits

Most advisers I meet are conscientious, client-first professionals.

Many already practise in a holistic spirit — discussing goals, wellbeing, family, and long-term direction.

The issue isn’t intention.

It’s scope.

You can be personally trustworthy and still operate inside a system that isn’t structurally trustworthy.

A system that:

- centres advice on what can be sold

- asks clients to trust incentives they can’t see

- stretches investment-framed guidance into life decisions it was never designed to govern

This creates a trust gap — not because advisers lack integrity, but because the architecture itself is too narrow.

Why scaling “1% guidance” won’t solve a 100% problem

There’s a growing belief that digital guidance tools will close the advice gap.

Technology will play a vital role.

But here’s the structural question we need to ask first:

Can guidance on less than 1% of someone’s wealth responsibly steer decisions about the other 99%?

Life decisions — career moves, pension choices, housing, resilience, family transitions — are not investment problems.

They are human capital and life-design problems.

Scaling product-framed guidance into these areas risks amplifying the very misalignment Consumer Duty is meant to correct.

The answer isn’t “no guidance”.

It’s better guidance — from a wider frame.

What Total Wealth Planning actually means

Total Wealth Planning doesn’t replace financial advice.

It reframes where advice fits.

It works across the full spectrum of human wealth:

- human capital

- financial capital

- social and family context

- wellbeing and resilience

- purpose, work, and life transitions

It separates planning from products, so decisions can be made calmly, transparently, and without hidden incentives.

And crucially, it empowers people to understand and direct their own lives — rather than outsourcing agency to intermediated structures.

This isn’t a retreat from professionalism.

It’s an expansion of it.

This isn’t about dividing the profession

Let’s be clear.

This is not about:

- creating a new elite

- dismissing regulated advice

- attacking advisers who remain inside the current model

It is about recognising a truth many advisers already feel:

The future of the profession lies beyond the investable 1%.

Total Wealth Planning liberates advisers to work with the whole person — not just the portion of life that can be wrapped in a product.

A bridge, not a rupture

Transitioning doesn’t require burning bridges, abandoning professionalism, or rejecting regulation.

Many advisers begin by:

- separating planning conversations from product implementation

- expanding their work into generic advice, education, and life-first frameworks

- using tools that are transparent, auditable, and structurally trustworthy

- gradually shifting their value proposition from asset management to life navigation

This is a rite of passage, not a rebellion.

Why this shift is already underway

Whether the industry likes it or not, the economics are moving:

- Investment management is being commoditised by AI

- Consumers are already using technology for guidance

- Consumer Duty is pulling focus toward outcomes, not products

- Percentage-of-assets fees are becoming harder to justify

- Public trust increasingly flows toward transparent, empowering models

The question isn’t if the model evolves.

It’s who leads that evolution — and with what values.

An invitation, not a verdict

If you’re an adviser who:

- wants to work with the whole person

- feels constrained by a product-first perimeter

- believes trust must be designed into systems, not merely asserted

- wants to help before harm, not explain it afterwards

…then Total Wealth Planning may already describe the work you’re trying to do.

The Academy of Life Planning exists to support that transition — training experienced professionals to become Certified GAME Plan Practitioners and practise as Total Wealth Planners, working across the real drivers of lifetime wellbeing.

This isn’t about stepping away from standards.

It’s about stepping into a fuller definition of wealth.

The question that matters

So here’s the simplest question I can ask — not rhetorically, but structurally:

Is it reasonable to expect advisers authorised on less than 1% of someone’s wealth to guide decisions about 100% of their life?

If the answer feels uncomfortable, that discomfort isn’t failure.

It’s the signal that the profession is ready to grow.

Read more: Why Britain Needs Total-Wealth Planners — Not 1% Advisers.

If This Resonates…

If you’re a financial planner who’s beginning to sense that

products, portfolios, and performance alone no longer tell the whole story,

you’re not alone.

Many capable, ethical advisers reach a point where they start asking quieter questions:

- Is this really the best way to serve people?

- Why do some clients thrive — while others, given the same advice, don’t?

- What sits beneath money that actually shapes outcomes?

Exploring Total Wealth Planning isn’t about rejecting your past experience.

It’s about building on it — by placing human capital, agency, and life design at the centre of your work.

The Academy of Life Planning exists for advisers in that in-between space:

- those transitioning from traditional financial planning

- those curious about empowerment-led, product-free models

- those wanting to serve clients more deeply, without ideology or pressure

You don’t need to commit to anything.

You don’t need to “switch sides”.

You’re simply invited to explore, learn, and see whether this approach aligns with how you want to practise in the next chapter.

Explore the Academy and the Total Wealth Planning pathway

Sometimes the most important shift isn’t a leap —

it’s a gentle crossing.