Most financial innovation cycles follow a familiar pattern.

New ideas emerge.

Confidence rises.

Education accelerates.

Narratives spread faster than understanding.

This is not a criticism. It’s how progress has always unfolded — from railways to dot-coms to structured finance to today’s digital assets and alternative investments.

The problem isn’t innovation.

The problem is what happens after the confidence runs out.

Phase 1: The Narrative Phase

Every cycle begins with a compelling story.

- A new solution to an old problem

- A promise of efficiency, freedom, or protection

- A sense that those who hesitate will be left behind

Education flourishes in this phase. Workshops fill. Courses sell. Confidence grows.

At this stage, discussion is optimistic and forward-looking. Questions are framed around access, understanding, and how to participate.

This phase feels empowering — and often is.

Phase 2: The Decision Phase

Between education and outcome lies a quieter moment.

This is where individuals make decisions under uncertainty — often balancing excitement, fear, trust, and personal circumstances.

For advisers and planners, this is where professional responsibility subtly shifts:

- How does this decision fit the person’s life, not just their portfolio?

- What assumptions does it rely on?

- What happens if conditions change?

- What support exists if things don’t go to plan?

These questions are rarely the loudest ones in the room — but they matter most over time.

Phase 3: The Stress Phase

Every system reveals its true design under stress.

Markets move.

Liquidity tightens.

Governance is tested.

Support structures are strained.

This phase is not proof that an idea was foolish or illegitimate. It is simply where theory meets reality.

Some systems absorb stress well.

Others expose fragility.

The difference lies not in the promise — but in the architecture.

Phase 4: The Aftermath Phase

This is the phase most financial education never reaches.

When losses occur, when disputes arise, when expectations collide with lived experience, people don’t just face financial consequences — they face emotional, psychological, and physical strain.

Common features of this phase include:

- Exhaustion and self-blame

- Complex complaint or recovery processes

- Systems that feel slow, opaque, or adversarial

- A sense of being left to navigate alone

This phase exists across all financial systems when harm occurs — traditional or innovative, regulated or experimental.

Yet it is rarely discussed upstream.

Phase 5: The Recovery Phase

Here lies the biggest gap in modern financial services.

Most systems are designed for entry.

Very few are designed for recovery.

Recovery is not just about money. It’s about:

- Health before litigation

- Stability before redress

- Rebuilding confidence before pursuing outcomes

Without recovery architecture, people are forced to fight complex systems at the very moment they are least resourced to do so.

This is where holistic, life-first planning becomes essential — not as a critique of innovation, but as its necessary counterpart.

Why This Matters for Planners and Advisers

Ethical guidance is not about predicting winners and losers.

It’s about acknowledging the full lifecycle of financial decisions — including what happens after things go wrong.

True professionalism asks:

- Are we preparing clients only for opportunity — or also for adversity?

- Do our models consider aftermath, not just outcomes?

- Are we designing advice that people can live with, even under stress?

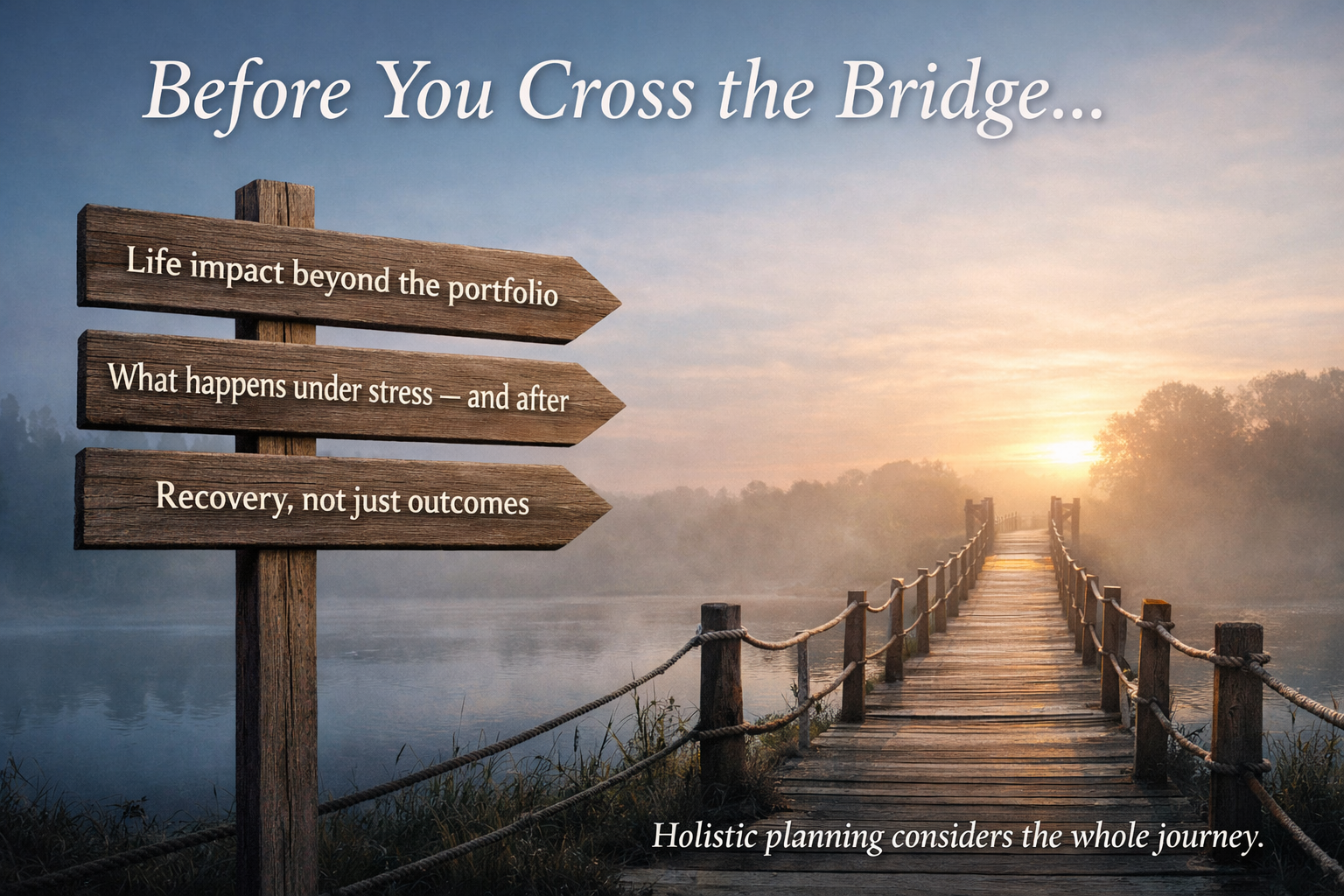

The Bridge Forward

The future of financial planning is not a binary choice between old systems and new ideas.

It is about building bridges — from narrative to reality, from confidence to resilience, from entry to recovery.

Innovation without recovery leaves people exposed.

Recovery without dignity leaves people diminished.

Holistic planning exists to hold the whole journey — human, financial, emotional — not just the moment of decision.

Because empowerment is not hype.

It is what remains when the story ends.

If you’re thinking about how financial guidance needs to evolve

beyond entry, beyond products, and beyond single-moment decisions —

there is a growing body of work exploring what holistic, life-first planning looks like in practice.

Some call it crossing the bridge.

It starts with asking better questions — about people, not just portfolios.

Visit the Academy of Life Planning for more details.