Most new financial advisers are taught to plan only half a life.

The familiar model—accumulation, transition, retirement, legacy—has become so normalised that few stop to ask a more fundamental question:

What exactly are we planning?

The answer, in practice, is almost always the same:

financial capital.

Savings. Investments. Pensions. Decumulation strategies. Estate planning.

All important.

All necessary.

But deeply incomplete.

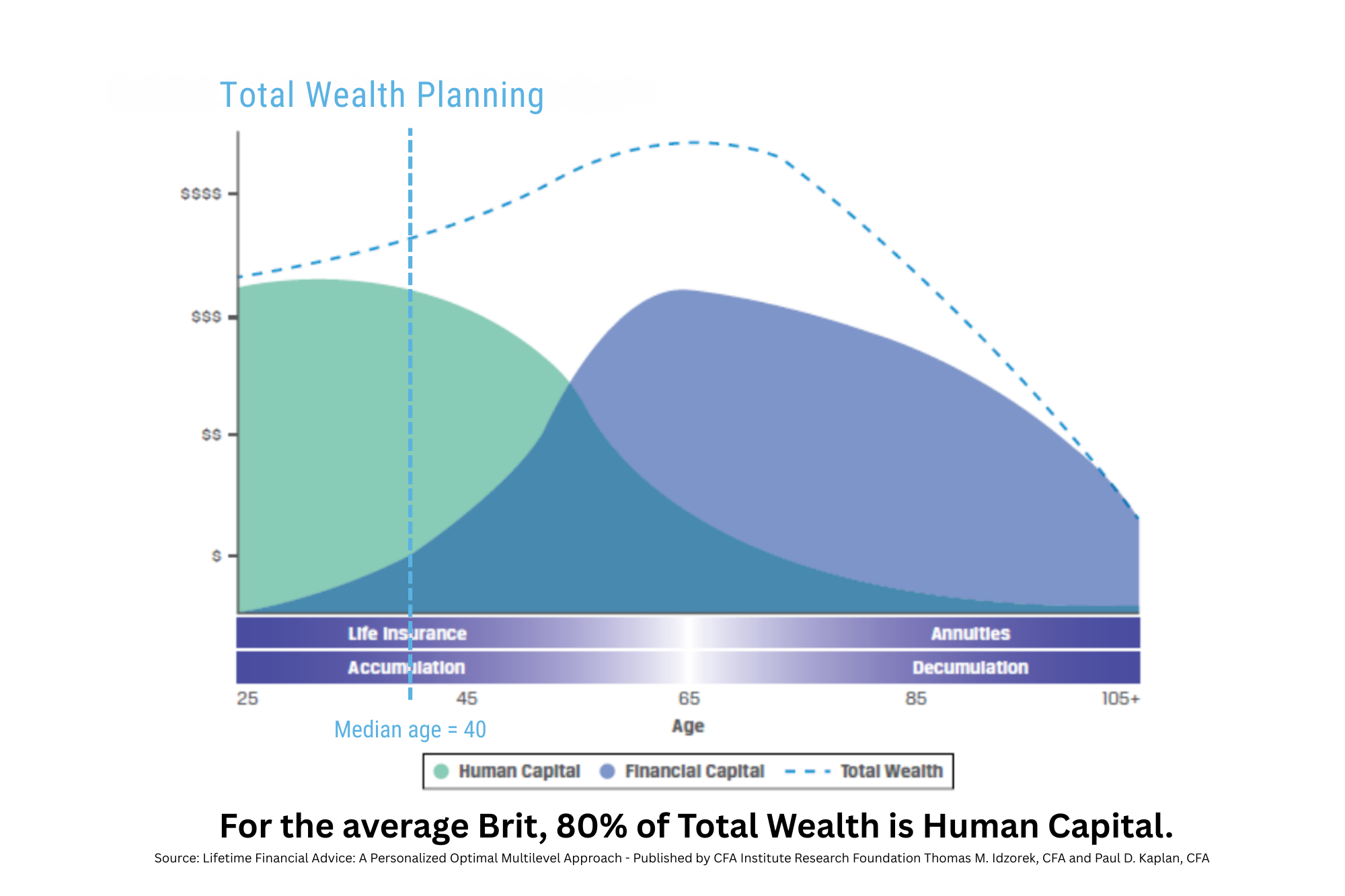

Because financial capital is not the primary source of wealth in a nation, a family, or a life.

Human capital is.

By most economic measures, around 80% of a developed nation’s wealth sits in its human capital—its skills, health, creativity, adaptability, relationships, and capacity to create value over time.

Yet this dominant form of wealth is largely invisible in mainstream financial planning.

That omission has consequences—not just for clients, but for society.

The Hidden Assumption in the Traditional Model

The traditional lifetime planning framework quietly assumes something profound:

- Human capital is front-loaded

- Financial capital is the real objective

- Retirement is the point at which contribution ends

In effect, the story goes like this:

- Learn when you are young

- Earn while you are useful

- Save enough to stop

- Withdraw until death

- Pass on money, not meaning

This model may have made sense in a mid-20th-century industrial economy.

It makes far less sense in a world of:

- Longer lives

- Faster technological change

- Automation and AI

- Fragile employment structures

- Widespread loss of purpose in later life

Most strikingly, it leads to an extraordinary outcome:

We spend a lifetime building human capital… then discard it.

A Total Wealth Lens: Financial Capital and Human Capital

Total Wealth Planning begins with a simple reframing:

Total Wealth = Financial Capital + Human Capital

Financial capital is stored value.

Human capital is productive potential.

Financial capital is finite and exhaustible.

Human capital is adaptive, renewable, and relational.

Crucially, financial capital is downstream of human capital.

Money is not created in a vacuum. It is the by-product of applied skill, effort, insight, and care—either your own or someone else’s.

So what happens if we map the human side of the equation across a lifetime, rather than treating it as an inconvenient prelude to “real” planning?

The Human Capital Lifecycle (A Missing Map)

1. Accumulation: Building Human Capital

Human capital accumulation begins long before the first payslip.

It includes:

- Education and skills

- Emotional intelligence

- Health and energy

- Values, curiosity, and identity

- Social and professional networks

This phase does not end at 21, or 25, or even 40.

In a Total Wealth framework, lifelong learning is not optional. It is a core asset-management strategy.

Planners who understand this help clients:

- Invest in themselves, not just markets

- See learning as compounding

- Recognise that adaptability is a form of wealth

2. Preservation: Maintaining and Renewing Human Capital

In financial planning, preservation usually means risk management.

In human terms, it means:

- Physical and mental health

- Avoiding burnout

- Maintaining relevance

- Psychological safety and meaning

- Continuous skill renewal

This is where many people quietly lose wealth—through exhaustion, illness, disengagement, or identity collapse—long before money becomes an issue.

A Total Wealth Planner asks:

- What is eroding this person’s capacity to earn, create, or contribute?

- What needs protecting now to preserve future optionality?

3. Crystallisation / Transition: Converting Human Capital into Livelihood

This is the most misunderstood—and most powerful—phase.

Human capital “crystallisation” does not mean stopping work.

It means leveraging accumulated capability into sustainable livelihood.

This may include:

- Entrepreneurship

- Portfolio careers

- Consultancy or coaching

- Mentoring, teaching, or advisory roles

- Community-embedded enterprise

Here, human capital is intentionally converted into:

- Financial capital

- Time autonomy

- Meaningful contribution

- Resilience against economic shocks

This is not a late-life afterthought.

It is strategic livelihood design.

4. Decumulation: The Changing Nature of Human Capital

Unlike financial capital, human capital does not simply “run down”.

It transforms.

Yes, some capacities decline with age—particularly those tied to speed, stamina, or narrow technical execution.

But others often increase:

- Wisdom

- Pattern recognition

- Judgment

- Emotional regulation

- Systems thinking

- Teaching and stewardship

The tragedy of the conventional retirement model is that it treats all human capital as obsolete once paid employment ends.

It confuses exit from a job with expiry of value.

5. Succession: Passing On Human Capital, Not Just Money

Financial succession planning focuses on assets.

Human succession planning focuses on:

- Knowledge transfer

- Skill transmission

- Values and culture

- Mentorship and apprenticeship

- Intergenerational continuity

When societies fail to do this, they experience:

- Skill shortages

- Loss of institutional memory

- Cultural fragmentation

- Disconnected generations

At the individual level, people experience:

- Loss of identity

- Loss of purpose

- Premature decline

Teaching others is not an indulgence.

It is the highest return on a lifetime of accumulated human capital.

The Greatest Waste: “Retiring” Human Capital

Here is the uncomfortable truth:

For many people, retirement means throwing their most valuable asset on the scrap heap.

After decades of investment, development, and lived experience, we tell people—explicitly or implicitly:

- You are done

- You are no longer needed

- Your role is consumption, not contribution

From a Total Wealth perspective, this is not just sad.

It is economically irrational.

Socially damaging.

And psychologically corrosive.

What This Means for New Planners

If you are entering the profession today, you are not just managing portfolios.

You are helping people navigate:

- Identity transitions

- Livelihood risk

- Meaning and contribution

- Structural shifts in work and value creation

A planner who understands human capital across a lifetime:

- Plans with people, not over them

- Designs for agency, not dependency

- Sees retirement as evolution, not erasure

- Helps clients stay economically and socially alive

This is the bigger picture.

Not “financial planning versus life planning”.

But planning for total wealth in a human world.

A Final Reflection

Money matters.

But people matter more.

Financial capital supports life.

Human capital creates it.

The future of planning belongs to those willing to hold both—

and to help others do the same.

Ready to expand your planning lens?

If you’re a planner who already cares about doing the right thing for clients —

and you can sense that traditional, product-led planning no longer tells the whole story — you’re not alone.

The Academy of Life Planning exists to support planners who want to:

- Work with people, not just portfolios

- Integrate human capital and financial capital into one coherent framework

- Help clients stay economically, psychologically, and socially alive across a lifetime

- Transition at their own pace, without abandoning professionalism or credibility

You don’t need to reject everything you’ve learned.

You simply need a bigger picture.

At the Academy, we help planners make that shift — thoughtfully, ethically, and practically — so they can become Total Wealth Planners for a changing world.

👉 Join the Academy of Life Planning

Explore the training, community, and frameworks that support planning for total wealth — not just retirement.

A bridge, not a leap. A progression, not a rebellion.