For years we’ve told people that “financial advice” means picking funds, switching products, or optimising the investable sliver of their portfolio. But this narrow definition has hidden a deeper structural truth: regulated retail investments — the only area most advisers are authorised to touch — account for less than one percent of the total wealth of the average Brit. Human capital, life decisions, career strategy, resilience, family transitions, and purpose-driven planning make up the real 99%. When advice is restricted to the smallest slice of a person’s wealth, even the best professionals are forced to operate with one hand tied behind their back. The sector is full of good people — but the system remains too small for the needs of the public.

“Two observations Steve. One, you can be trustworthy, but not be trusted. Two, I think way more than 1% of regulated advisers are focused on financial planning and holistic wealth planning.

It disturbs me that the planning sector focuses on what divides practices rather than unites. I’d like to see more emphasis on what makes better practice than why everyone apart from a 1%“ elite” doesn’t try hard to meet customers needs and expectations”

You’re absolutely right — trust isn’t something we declare, it’s something others experience.

Being trustworthy is the starting point.

Being trusted is the outcome of consistently demonstrating transparency, accountability, and alignment with someone’s best interests.

One of the biggest problems in financial services is precisely this gap:

institutions that ask to be trusted without first proving they are structurally trustworthy.

That’s why our work focuses on rebuilding trust from the ground up — through open systems, clear conduct, and planners who remove conflicts rather than manage them.

Trust can’t be demanded.

It has to be earned, witnessed, and reinforced through action.

Thank you — I agree completely that many advisers aspire to be holistic, and that the profession is at its best when we focus on raising standards rather than drawing lines between practitioners.

But the core issue here isn’t effort or intention.

It’s scope — and the constraints of a structurally narrow system.

Most regulated advisers want to offer whole-life, whole-wealth planning.

The problem is that the regulatory perimeter only allows them to advise on regulated retail investments — which, as the data show, represent well under 1% of the total wealth of the average Brit.

That isn’t a reflection on the advisers themselves.

It’s a reflection of a system designed around product intermediation, not total-wealth decision-making.

A few key points:

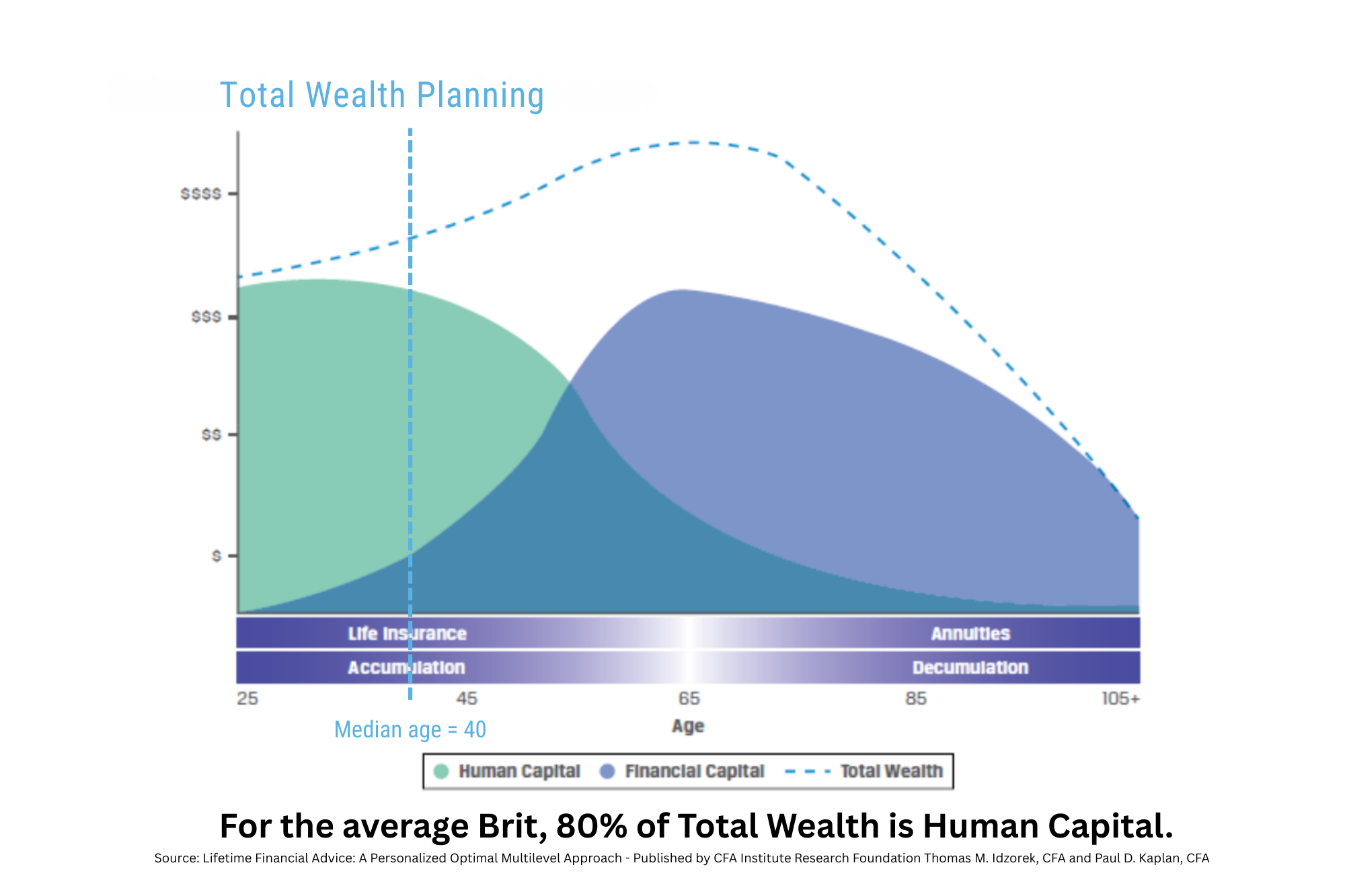

- Human capital represents the majority (c. 80%) of total wealth.

- Financial capital is ~14–20% of total wealth.

- Retail investments are a small fraction (<5%) of financial capital.

- Therefore, retail investments represent <1% of total wealth for the average person.

Advisers can be excellent, diligent, client-first professionals — and many are —

but if they are authorised only on that <1% slice, then the system prevents them from delivering truly holistic planning, no matter how much they want to.

That’s the heart of the discussion.

This is not about elevating an “elite”; it’s about elevating the conversation.

Holistic wealth planning requires working across:

- Human capital

- Financial capital

- Social capital

- Emotional and spiritual capital

- Lifetime choices

- Work, health, family, purpose, and transitions

Regulated investment advice covers only the part that can be sold as a product.

Holistic wealth planning covers the parts that actually define someone’s life.

My position is simple:

If we want better outcomes for consumers, we need planners empowered to support the full spectrum of human wealth — not just the investable 1%.

And that’s what the Academy trains for:

qualified professionals, many QCA Level 6+, accredited in total-wealth planning through the GAME Plan, helping people make life-first decisions before money-first decisions.

This isn’t about dividing practitioners.

It’s about unifying the profession around a broader, more honest definition of wealth, so advisers aren’t constrained to working on the tiniest slice of a client’s life.

Always happy to keep the dialogue open — we both want the same thing: better outcomes, greater trust, and a profession that truly serves people.

Sorry Steve, I disagree.

As you say, “People want guidance.” How can that be offered at scale without digital tools and access? You are right to flag the risk of guidance tools being turned into direct to consumer sales of products, but FCA’s final guidance allied to supervisors looking at how tools are used through a Consumer Duty lens could be enough to overcome your concerns.

I’d also add that the number of offerings out there now is nothing like what will be available from a range of service providers in 12 months. Firms are having to assess the revenue side of any proposition before launching.

You should also bear in mind how much potential harm there is from people following influencers and punting on instruments like crypto, CFD’s etc. I’ll take some imperfections with targeted support over Uber-provision or the investment equivalent of the Wild-West.

Thank you — and I absolutely recognise the intention behind targeted support. We both agree that people want guidance and that digital tools will play a major role in delivering it at scale. The question is what kind of guidance, and from whom.

Let me explain the structural issue at the heart of my concern.

FCA-regulated retail investments represent less than one percent of the total wealth of the average Brit.

That’s not opinion — that’s what the data imply when you combine:

- Research showing human capital makes up around 80% of lifetime wealth (Cobb 2004; Ibbotson/CFA Institute definition of total wealth).

- ONS findings that financial capital is only ~14–20% of total wealth.

- FCA data showing that most of that financial capital sits in cash — not in retail investments.

- And retail investments themselves represent <5% of financial capital.

Put those together and the picture is clear:

The only area advisers are authorised to touch is well under 1% of a person’s real wealth.

So the issue isn’t that advisers lack skill or professionalism — many are exceptional.

The issue is that the regulatory perimeter only allows them to advise on the smallest slice.

Now apply that to your point about guidance tools.

Guidance on 1% of wealth cannot credibly direct decisions about the other 99%.

Building digital systems to scale guidance is sensible.

But building systems that scale product-distribution-framed guidance into areas of life they’re not designed to address poses real risk:

- Life decisions

- Work decisions

- Human capital

- Pension choices

- Career transitions

- Debt, income, resilience

- Family transitions

- Housing and lifestyle

These have the biggest impact on lifetime outcomes — and they sit almost entirely outside the 1% retail investment authorisation perimeter.

Targeted support, as currently framed, lets product manufacturers provide “what people like you did” nudges without accountability, while implying they can guide total-wealth decisions. That’s the structural problem.

On influencers and the “Wild West”

You’re right: TikTok-finance and crypto-pumping are harmful.

But the answer is not to hand the steering wheel of total-wealth guidance to product distributors.

The Academy’s model is different:

- 95% of our planners are Level 4+

- 75% are Level 6+ — higher than the general market

- They’re trained as total-wealth practitioners, not product intermediaries

- They provide generic advice without conflicts

- And they empower clients to understand, decide, and act for themselves

We’re not replacing quality advice.

We’re replacing intermediation with education + empowerment.

My core point:

Digital tools are essential — but they must be structurally trustworthy.

They must serve the consumer, not the distributor.

They must cover the whole of life, not just the investable 1%.

If we get this right, we elevate the profession and protect the public.

If we get it wrong, we scale the old model into a bigger problem.

Always happy to continue the dialogue — we’re both aiming for better outcomes, but we must ensure the architecture itself doesn’t reproduce the issues we’re trying to solve.

FCA regulated retail investments represent less than one percent of wealth of the average Brit.

Is it sensible to expect someone authorised to advise on less than one percent of your total wealth to guide decisions about the whole of your life? Yes or no?

Let me break that down for you:

- Quantifying the Wealth of Nations: The Impact of Intangible Capital (Cobb, 2004). The paper reports that in the U.S., intangible capital (comprising human plus social capital) was ~$418,000 per person (in year 2000 dollars) — about 80 % of total wealth per capita for that country in that year.

- The Mean Age in United Kingdom (2021 – 2029, years) according to global data. The average (mean) age in Britain is around 40.2 years (est. for 2021).

- Lifetime Financial Advice: A Personalized Optimal Multilevel Approach. With a foreword by Roger G. Ibbotson – Published by CFA Institute Research Foundation, defines Total Wealth = Human Capital plus Financial Capital.

- According to the ONS “Household total wealth in Great Britain: April 2020 to March 2022”, net financial wealth accounted for 14 % of household wealth.

- The FCA’s “Financial Lives 2024” report shows that among UK adults with £10,000+ in investible assets, 61 % held all or at least three-quarters in cash savings rather than investments in 2024.

And, the ONS data excluded business assets. And investment include shares as well as mutual funds. But if two thirds of savings and investments are in savings, that means less than 5% is in investments (which includes shares).

If financial capital is less than 20% of total wealth for the average Brit, and retail investments is less than 5% of financial capital, then retail investments is less than one percent of total wealth.

Having firms give advice to the average Brit on total wealth decisions by only giving advice on buying and selling regulated investments, could result in unfavourable outcomes. Would you agree, yes or no?

Even worse, having mutual investment firms give you targeted support relating to total wealth, saying what people like you did, but without accountability for giving specific advice, is even worse. Wouldn’t you agree, yes or no?

We do not advocate for people following unqualified influencers. According to a poll of its members, the Academy of Life Planning found that 95% of its planners are qualified to QCA Level 4 and above, and 75% qualified to QCA Level 6 and above. That is, the vast majority of our members are Certified or Chartered financial service professionals, which is a higher level of professionalism than FCA regulated advisers generally.

Academy members are also trained and accredited as total wealth practitioners, through the GAME Plan practitioner training course.

Our view is that outcomes for consumers would improve if given generic advice from a Holistic (Total) Wealth Planner, and they were educated, activated, and empowered to manage their own finances, rather than asking a product distributor to make decisions for them.

If we want genuinely better outcomes, we have to widen the frame. Holistic wealth planning isn’t about dividing the profession; it’s about liberating it. It allows advisers to work with the whole person — their human, social, financial, emotional, and spiritual capital — instead of being confined to product intermediation. The data is clear: consumers need guidance on life-first decisions, not just the investable one percent. By expanding the perimeter, we empower both practitioners and the people they serve. It’s time to build a profession capable of supporting the full spectrum of human wealth.

If you want to work at this deeper level — beyond products, beyond the 1%, and into the real drivers of lifetime wellbeing — the Academy of Life Planning can train you to become a Certified GAME Plan Practitioner and a Holistic Wealth Planner. Join a community of highly qualified professionals who are redefining what financial planning means.

Train with the Academy and help lead Britain into a new era of total-wealth planning. Find out more about our training programmes.

Addendum: Responding to the “Nothing Will Ever Change” Mindset

Some wealth managers argue that the investment-advice model will never shift because “that’s where the real money is.”

I hear this often — and I understand why the cynicism exists.

For decades, the clever play in the industry has been simple:

Tap into client assets → charge a percentage → scale the revenue.

But the belief that this model is immortal is not a law of finance — it’s just a habit of history.

The world around it is already changing in ways that make its decline inevitable.

1. Consumers are voting with their behaviour

56% of UK adults now use AI for financial guidance.

When people realise that machines can manage the investable 1% cheaper, faster, and without conflicts, the old fee structure becomes economically unsustainable.

This isn’t a moral judgment — it’s market reality.

2. Regulation is shifting away from intermediation

Consumer Duty focuses on outcomes, not products.

Once value must be demonstrated in life results rather than fund selection, percentage-of-assets fees lose their justification.

3. Technology is commoditising investment management

AI has already driven the marginal cost of basic investment tasks close to zero.

When something becomes a commodity, prices collapse.

No amount of narrative can stop that.

4. The real value — and demand — lies in the 99% ignored by the old model

Career strategy

Family transitions

Human capital growth

Resilience and wellbeing

Purpose, legacy and life design

Decision-making clarity

These are the areas where lives change — and where the public genuinely needs help.

This is what Holistic Wealth Planners are trained to deliver.

5. Structural trustworthiness is becoming a competitive advantage

Consumers are increasingly rejecting opaque, extraction-based fee models.

Transparent, educational, empowering frameworks are more investable — both ethically and economically — because they create real, lasting value.

The bottom line

When someone says “this will never change,” the answer is simple:

It’s already changing. Not because the industry wants it, but because the economics, technology, and public expectations demand it.

The future belongs to planners who serve the whole person, not just the investable fraction — and that’s why the Academy is building the global pathway to Holistic Wealth Planning.

One thought on “Why Britain Needs Total-Wealth Planners — Not 1% Advisers”