Are you a Financial Ecosystem Adviser or Financial Asset Adviser?

I think we can all agree, well us financial planners at least, that cash flow forecasts are essential when it comes to financial planning.

If you are not using cash flow forecasts, then you are at best a needs and shortfall analyser. Without which suitability would be hard to demonstrate.

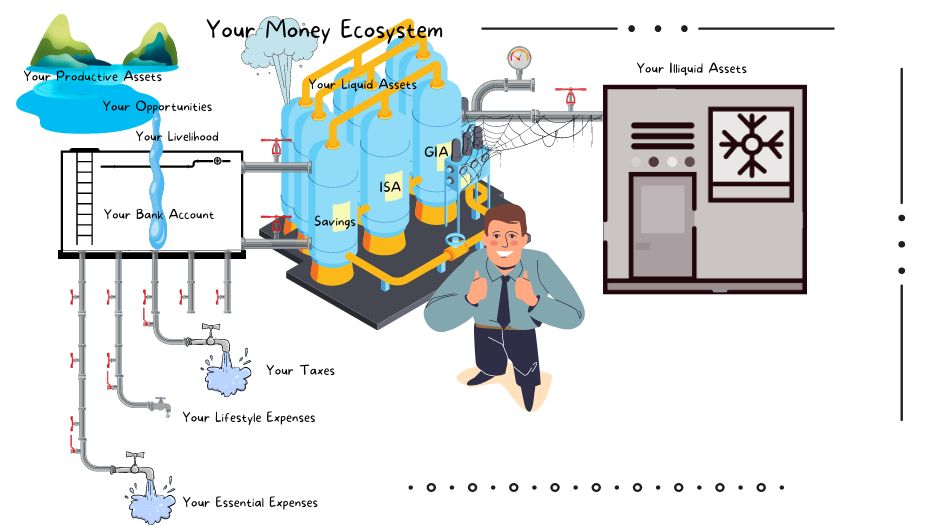

The problem with both models, they can take a very limited view of the whole financial ecosystem, and critically make some bold assumptions.

Let’s take the financial planner who is also a financial asset adviser; that is, I call myself a financial planner, but I pay myself by a percentage of assets under my advice. If we define ourselves by how we pay ourselves; I call myself a financial planner when really I am a financial asset adviser. At least 9 in 10 financial planners run this model.

There are several features of the financial asset adviser that strike me:

1. They are paid a percentage of financial assets under advice.

2. According to the Financial Conduct Authority (FCA), financial advisers charge an average of 2.4% of the amount invested for initial advice and 0.8% a year for ongoing advice (1.9% p.a with underlying product and portfolio charges factored in)². However, it’s important to note that financial advisers may also receive compensation in the form of bonuses, profit sharing, and commissions¹.

3. They are not paid on:

a) Property assets

b) Occupational Pension Scheme assets

c) Business assets

d) Other non-financial assets

e) Financial assets not under their advice, such as those managed by unconnected third-parties or self-managed by the client.

e) Liabilities

f) Income

g) Expenditure

4. “Show me the incentive, and I will show you the outcome.” – Charlie Munger. Where do you think cash flows end up? That’s right! Financial assets under their advice (and in product and portfolios factored in).

For example, if a client inherits a substantial sum should they a) repay the mortgage, b) buy a second property, c) gift to kids, d) gift to charity, or e) invest in financial assets?

Which one would the financial asset adviser recommend?

There are several big assumptions factored in by the financial asset adviser:

1. Income remains as is, perhaps increasing with national average earnings.

2. Income stops at a cliff edge retirement, perhaps phased in some circumstances.

3. Income stops at an earlier date on disability and you are unable to work due to illness or injury, unemployment, if you are diagnosed with a specified critical illness or medical condition, business operations are disrupted due to covered events, such as fire, natural disasters, or other unforeseen circumstances, if you are injured on the job, loss to the business in the event of the key person’s death or disability, various events that might prevent you from working, such as illness, injury, redundancy, or other unforeseen circumstances, and death.

4. Basic expenditure remains as is, perhaps increasing with retail prices.

5. Basic expenditure reduces at retirement.

6. Perhaps lifestyle expenditure is based on a life plan.

To maximise financial asset inflows, and hence fee income, the financial asset adviser must maintain income levels to retirement, assume cliff edge retirement, minimise expenditure during working life, and maximise expenditure in retirement. In other words, sell the retirement dream.

When the client retires, the financial asset adviser must switch to minimise expenditure to avoid drawdown on financial assets.

They also scare the client half to death on assumption 3 to maximise commission.

Annuities have been out of favour relative to drawdown, since commission was banned, as interest rates fell and deals looked poor at younger ages. However, now they are rising they are now in favour again. They can present an attractive option when adverse health is taken into consideration. Financial asset advisers take a fixed fee from pension pots to arrange annuity purchase. But then ongoing fees cease. Will this cause the financial adviser to defer annuity purchase, when annuity purchase may be the more favourable option?

As a financial planner who is not also a financial asset adviser, here’s what I think:

1. I am paid a fixed fee, wherever cash flows in the financial ecosystem.

2. I must factor in what makes the client happy. This can impact the income assumption. If the client is stuck on a treadmill of work existence taking the bet that they can buy happiness in later life, I would question it. And find work that they love, so that they never have to work a day in their life. Or find work that doesn’t feel like work, from which they never wish to retire.

3. If the client doesn’t have enough income, we would sit down and create a business plan to create more income.

4. The favourite future conversation has a focus on the next chapter of the client’s life. There is a price tag attached, and a liability forecast produced. We plan for happiness now, and test the lifetime forecast to see that this is sustainable into later life.

5. Continuing economic activity and passive income strategies are factored into retirement plans, more often than not there is no cliff edge retirement. Continued economic activity doing what you are good at, you love, the world needs, and will pay for extends your wealth health and happiness. You live longer better.

6. If a client inherits a substantial sum should they a) repay the mortgage, b) buy a second property, c) gift to kids, d) gift to charity, or e) invest in financial assets? We look at the pros and cons of each, and the client chooses the option they prefer.

Which option delivers the better outcome for the client? The financial ecosystem adviser, or the financial asset adviser?

Check out this earlier article: https://academyoflifeplanning.blog/2023/03/02/the-harsh-reality-the-financial-industrys-blindness-to-the-non-rich-majority/

Source: Conversation with Bing, 25/07/2023

(1) How much financial advice costs – Which?. https://www.which.co.uk/money/investing/financial-advice/how-much-financial-advice-costs-aODa70J6nYs7.

(2) Average Salary of a Financial Advisor – Investopedia. https://www.investopedia.com/ask/answers/120214/whats-average-salary-financial-advisor.asp.

(3) How Much Does a Financial Advisor Cost? – 2020 Financial Ltd. https://www.2020financial.co.uk/how-much-does-a-financial-advisor-cost/.

(4) Financial adviser fees – how much does a financial adviser cost …. https://www.unbiased.co.uk/discover/personal-finance/savings-investing/cost-of-advice.