There is a growing chorus of voices calling for higher auto-enrolment pension contributions in the UK.

A recent survey reported that 43% of business leaders support increasing contributions, with many arguing that workers simply are not saving enough for retirement.

At first glance, that sounds responsible.

Who wouldn’t want people to have more money in later life?

But beneath the surface lies a question that is rarely asked.

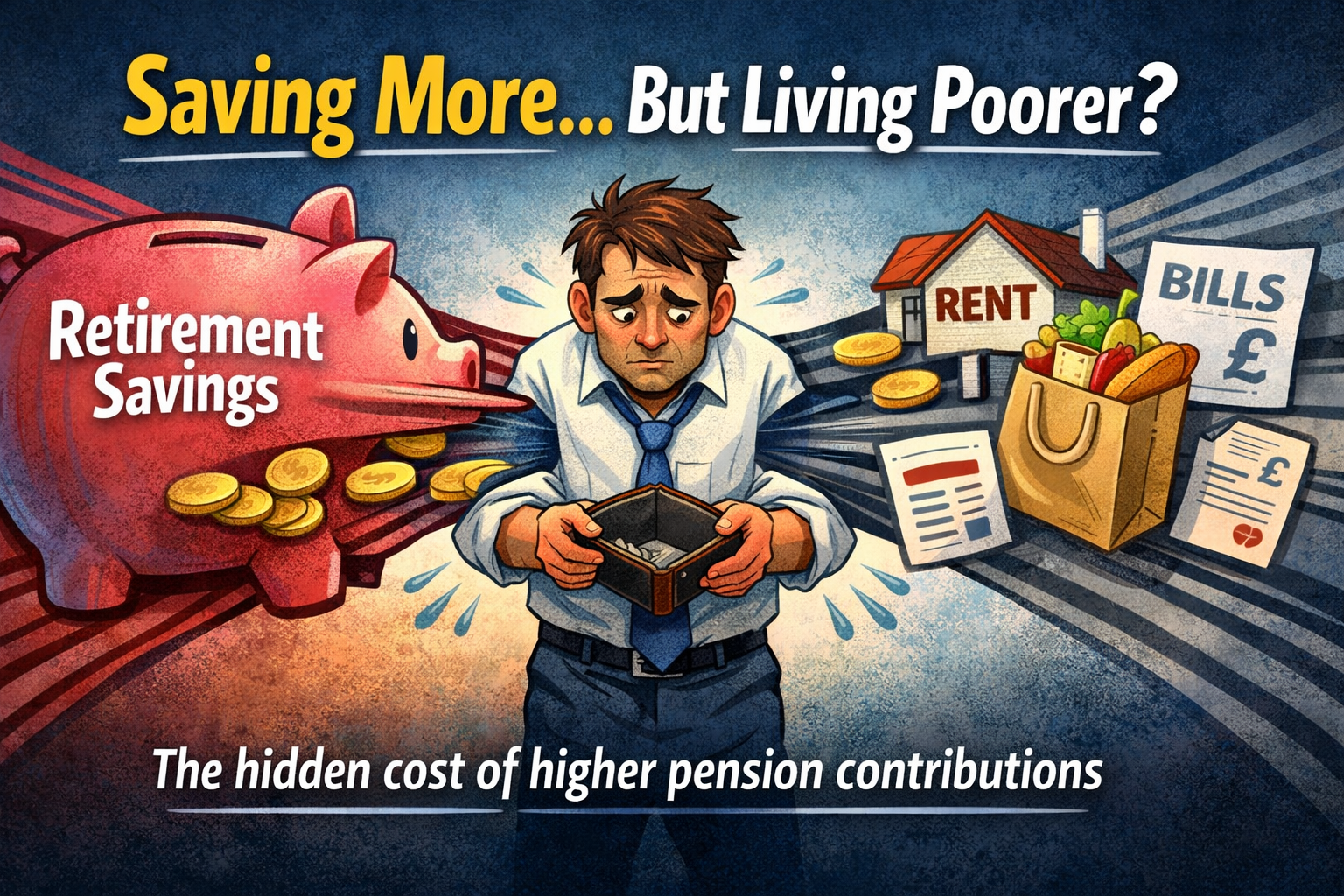

What if the policy designed to reduce poverty in old age actually increases poverty during working life?

The Financial Capital Bias

Public policy discussions about retirement poverty are overwhelmingly framed around financial capital strategies:

- increase pension contributions

- expand pension coverage

- build larger retirement funds

The assumption is simple:

more money saved today equals less poverty tomorrow.

But this view focuses almost entirely on financial capital.

It largely ignores something just as important:

human capital.

Human capital includes:

- skills

- health

- earning capacity

- adaptability

- entrepreneurship

- social and family networks

These are the assets that actually generate income throughout life.

Yet when governments design anti-poverty policies, human capital strategies are rarely at the centre of the discussion.

Why?

Because human capital policies are harder to measure and do not always feed directly into the financial growth metrics that dominate economic policy.

The Hidden Trade-Off

Increasing mandatory pension contributions means something very simple.

Workers take home less money today.

For higher earners this may be manageable.

For millions of households already struggling with:

- housing costs

- childcare

- energy bills

- food inflation

even a small reduction in disposable income can push them closer to financial stress.

In effect, the policy transfers resources from the present to the future.

For some households that is sensible.

For others, it may deepen working-age poverty.

And here lies the irony.

Many of the people who are told to save more into pensions are the same people who may later find that their pension savings reduce their eligibility for means-tested benefits in retirement.

The system rarely acknowledges this interaction.

Who Actually Benefits?

When the burden of pension contributions increases, the benefits are not evenly distributed.

Two institutions clearly gain.

Government

Larger private pension savings reduce future pressure on public social security systems.

The financial services industry

Bigger pension pots mean larger funds under management, which generates ongoing fees across the investment chain.

That does not mean pensions are bad.

Far from it.

But it does mean we should be honest about who benefits most from policies that push contribution levels higher.

The Missing Strategy: Human Capital

A more balanced approach to poverty prevention would combine financial capital strategies with human capital strategies.

For example:

- helping people build multiple income streams

- supporting later-life earning capacity

- encouraging entrepreneurship and flexible work

- investing in skills throughout life

- strengthening family and community support networks

These strategies reduce poverty without forcing households to defer large amounts of income for decades.

They also recognise an important reality.

Many people will continue to generate income well into later life, whether through work, business, consulting, or part-time roles.

The Real Question

The UK pension system has achieved something remarkable.

More than 22 million workers are now saving through auto-enrolment.

That success should not be dismissed.

But success should not stop us asking better questions.

Instead of asking only:

“How do we increase pension contributions?”

We should also ask:

- How do we reduce poverty during working life?

- How do we build human capital as well as financial capital?

- How do we create resilient income across the whole life cycle?

Because poverty is not just a retirement problem.

For many households, it is a working-age problem first.

And policies that ignore that reality risk solving one problem while quietly creating another.