A practical guide for the 90% of people who will never receive regulated investment advice

In the UK today, more than 90% of people do not receive regulated financial advice.

This is not because people do not need help.

It is largely because the economics of retail advice firms make it impossible to serve most households.

When the financial services industry talks about “financial advice,” it usually means something very specific:

a regulated recommendation to buy or sell a financial product.

Producing that recommendation requires compliance systems, documentation, professional indemnity insurance, and regulatory oversight. These costs mean many advisers can only serve wealthier clients.

For the majority of households, the result is simple:

you are likely to be self-directed when it comes to retail investments.

The good news is that being self-directed does not mean being unsupported. The regulatory framework allows financial educators and planners to signpost independent sources of information and evidence-based investment principles that individuals can use to make their own decisions.

This article explains how to approach self-directed investing in a sensible and disciplined way.

Step 1: Start With Independent Consumer Research

If you are making investment decisions yourself, the first principle is simple:

do not rely solely on marketing material from financial companies.

Instead, start with independent consumer research.

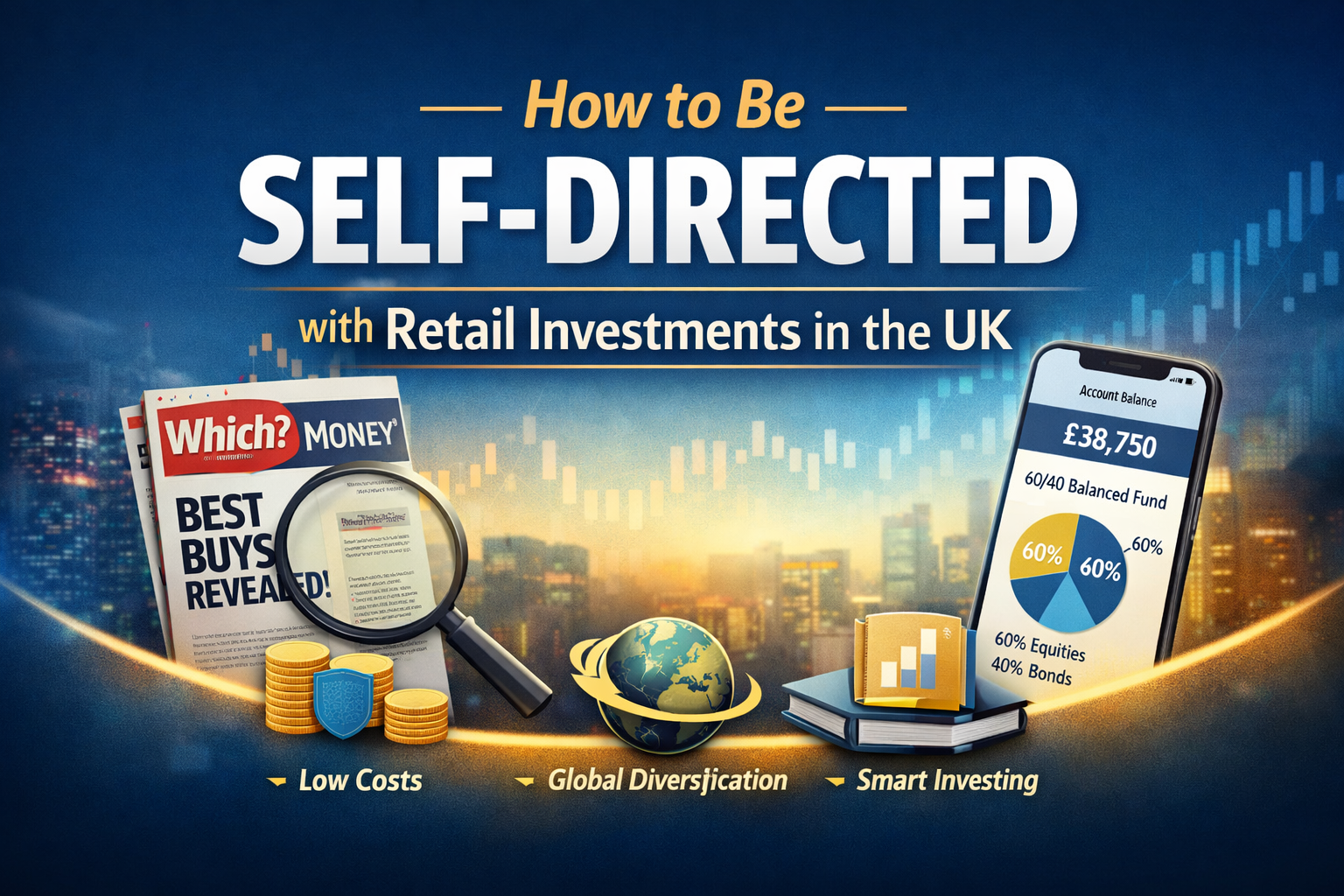

One of the most trusted sources in the UK is Which?.

The Which? Money magazine regularly surveys financial products and providers across the UK market.

Its value lies in several key features:

• recommendations are based on independent research and consumer feedback

• results are not influenced by product sponsorship

• the surveys cover platforms, savings accounts, and financial products

A subscription usually costs less than £10 per month, making it one of the most cost-effective sources of consumer financial research available.

Step 2: Use a Direct-to-Consumer Investment Platform

Once you have reviewed independent surveys, the next step is usually opening an account with a Direct-to-Consumer (D2C) investment platform.

These platforms allow individuals to:

• hold ISAs and pensions

• access diversified investment funds

• manage investments without a financial intermediary

The UK regulator recognises that consumers now have broad access to these types of investments.

In the foreword to the Consumer Duty consultation paper, former interim CEO of the Financial Conduct Authority, Chris Woolard noted that consumers now have access to a wide range of low-cost, globally diversified investments.

In other words, the tools required for diversified investing are widely available to individuals.

Step 3: Follow Evidence-Based Investment Principles

When investing without a financial adviser, it is particularly important to rely on evidence-based investment thinking rather than speculation.

Two excellent UK resources include:

- How to Fund the Life You Want by Robin Powell and Jonathan Hollow

- Be Your Own Financial Adviser by Jonquil Lowe

These books explain principles supported by decades of academic research, including:

• global diversification

• keeping costs low

• maintaining long-term discipline

• avoiding attempts to time markets

These principles underpin most sensible long-term investment strategies.

Step 4: Use Simple Diversified Funds

For most self-directed investors, simplicity is an advantage.

A practical approach is to use multi-asset funds that automatically rebalance themselves.

These funds typically contain two core building blocks:

• global equities (shares)

• fixed interest securities (bonds)

The fund manager maintains the target allocation between these assets and automatically rebalances the portfolio when markets move.

For example, a 60/40 fund might hold:

• 60% equities

• 40% bonds

Most providers offer a range of funds aligned with different risk levels.

Typical examples include:

| Fund | Equity Allocation | Description |

|---|---|---|

| 20 fund | 20% equities | cautious |

| 40 fund | 40% equities | defensive |

| 60 fund | 60% equities | balanced |

| 80 fund | 80% equities | growth |

| 100 fund | 100% equities | adventurous |

These funds allow investors to maintain diversified portfolios with minimal ongoing management.

Step 5: Match Investments to Your Time Horizon

Investment choices should reflect when you expect to need the money.

A simple framework can help guide decisions.

Short-term needs (0–5 years)

Money required within the next five years should normally be held in deposit accounts rather than investments.

Most households benefit from maintaining an emergency fund equal to around six months of expenditure.

If you hold larger deposits, it is sensible to spread money across institutions so that balances remain within the protection limits of the UK deposit protection scheme.

Medium-term goals (5–10 years)

For money required within the next decade, many investors choose balanced portfolios.

One simple rule of thumb sometimes used is:

100 minus your age = approximate equity allocation

For example:

Age 40 → roughly 60% equities / 40% bonds

This approach is simple and avoids unnecessary complexity.

Long-term investing (10+ years)

Money invested over longer periods can typically tolerate greater exposure to equities.

Some investors choose allocations around 90% equities and 10% bonds for long-term portfolios.

One simple way to approximate this allocation is combining funds with different equity levels — for example blending an 80% equity fund with a 100% equity fund.

The key principle is long-term discipline.

Most investment returns come from time in the market, not timing the market.

Step 6: Keep Costs Low

Costs are one factor that will certainly affect investment outcomes.

Many investors therefore prioritise:

• fund charges below 0.50% per year

• platform charges around 0.35% per year

Combined costs significantly above these levels deserve careful scrutiny.

Even small differences in fees can compound into large differences in long-term wealth.

Step 7: Avoid Unnecessary Complexity

For most retail investors, the core components of a sensible portfolio are simply:

• global equities

• high-quality bonds

We do not recommend alternative assets such as:

• commodities

• speculative property investments

• cryptocurrency

Some investors may choose to explore these assets, but they introduce additional risk and complexity.

For most households, a diversified equity-and-bond portfolio is more than sufficient.

Step 8: Keep Investments in Perspective

A final point is often overlooked.

For the average UK household, retail investments represent only a small fraction of total lifetime wealth.

Most wealth comes from:

• future earnings (human capital)

• the family home

• pension entitlements

Retail investment portfolios are often only a small proportion of total wealth.

This means it is usually unproductive to spend large amounts of time worrying about short-term market movements or chasing marginal investment improvements.

Sound financial planning is far more about life decisions, career choices, and long-term stability than about constantly adjusting investment portfolios.

The Bottom Line

If you do not have access to regulated retail investment advice, a sensible approach is still available.

A practical framework looks like this:

- Use independent consumer research such as Which? Money

- Invest through a reputable D2C platform

- Follow evidence-based investment principles

- Use diversified multi-asset funds

- Match investments to your time horizon

- Keep costs low

- Avoid unnecessary complexity

And if your situation becomes more complex — such as inheritance decisions, business ownership, major tax planning, retirement transitions, or other significant life changes — it may help to consult a registered financial professional who is a Total Wealth Planner.

A Total Wealth Planner is not incentivised to sell financial products. Their role is to help you think clearly across the full picture of your life and wealth.

That distinction matters.

The real gap in the UK is not access to product distribution.

It is access to structurally trustworthy financial thinking.