Only 1 in 10 Britons are financially secure.

That headline should stop us in our tracks.

But it shouldn’t surprise us.

For decades, financial planning has focused on managing what people already have — not on increasing their capacity to create more.

And here’s the uncomfortable truth:

You cannot empty the pockets of those whose pockets are already empty.

You cannot build a reservoir if there is no water source.

You cannot optimise scarcity.

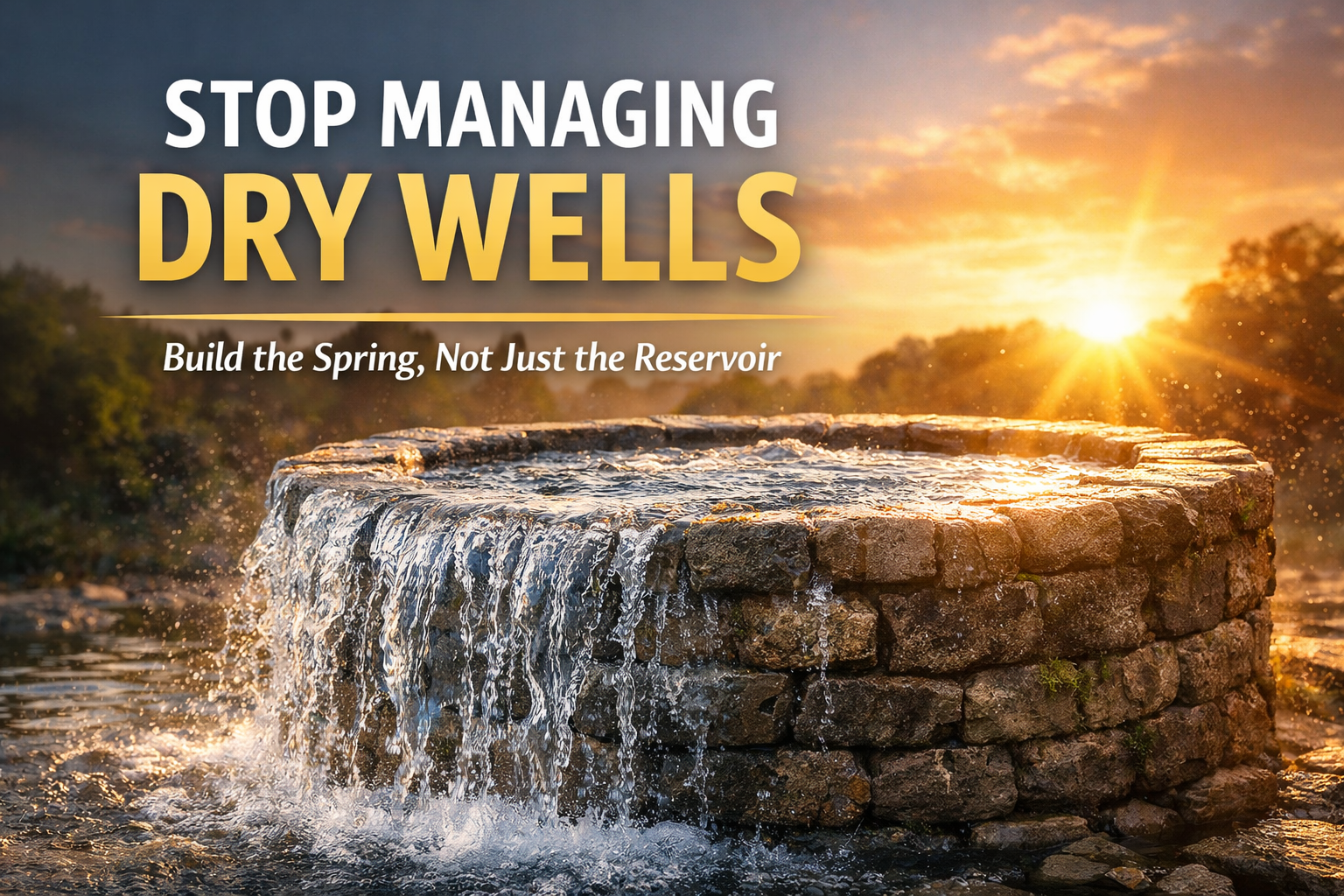

Money Is Like Water

Think of financial security as a water system.

- Income is the spring.

- Human capital is the underground source.

- Savings are the reservoir.

- Investments are irrigation channels.

- Protection is flood defence.

If the spring dries up, the reservoir empties.

Most financial advice focuses on protecting and organising the reservoir. Budgeting. Consolidation. Asset allocation. Pension wrappers.

But if there is no consistent flow feeding the system, those strategies eventually fail.

A dry well cannot be managed into abundance.

It must be reconnected to a source.

The Structural Blind Spot

Traditional financial plans typically start here:

- What do you earn?

- What do you spend?

- What do you save?

- How do we invest the surplus?

That assumes surplus exists.

For millions of people, it doesn’t.

When income is fragile, stagnant, or capped, savings advice becomes pressure rather than empowerment. It becomes an instruction to restrict rather than a pathway to expand.

The issue isn’t poor discipline.

It’s under-developed or under-leveraged human capital.

Human Capital Is the Primary Asset

In national accounting terms, human capital represents the majority of total wealth.

Yet in many financial plans, it’s treated as a background assumption.

Human capital includes:

- Skills and experience

- Health and energy

- Networks and reputation

- Adaptability

- Entrepreneurial capacity

- Intellectual property

- Positioning in the marketplace

It is the engine that generates income, resilience, and optionality.

Without strengthening that engine, financial planning becomes a rearrangement exercise.

From Dry Well to Flowing Spring

The Total Wealth Plan begins where traditional plans often don’t.

It asks:

- What productive assets are currently dormant?

- What capabilities are undervalued?

- What entrepreneurial opportunities exist?

- What income pathways are possible?

- What risks threaten your earning power?

- What small shifts could increase sustainable cashflow?

Before focusing on savings, it focuses on flow.

When flow increases:

- Debt can be paid down faster.

- Emergency reserves can be built.

- Financial anxiety reduces.

- Investment becomes possible.

- Long-term security becomes realistic.

Security follows production.

The Journey: From Suffering to Security

Financial insecurity is rarely just a numbers issue.

It affects confidence. Relationships. Health. Decision-making.

When income is fragile, every unexpected expense feels existential.

A regenerative planning approach creates a pathway:

Suffering → Survival → Stability → Security

Not through austerity alone.

Through expansion of capacity.

Through structured human capital development.

Through entrepreneurial clarity.

Through agency.

The Profession at a Crossroads

If only 1 in 10 people are truly financially secure, the design of mainstream planning needs examination.

A system that:

- Focuses primarily on financial capital

- Prioritises product distribution

- Assumes surplus income

- Underestimates productive potential

…will struggle to address structural vulnerability.

A Total Wealth approach recognises that:

Financial capital is downstream of human capital.

You don’t solve insecurity by telling people to shrink forever.

You solve it by helping them grow.

The Real Shift

The real shift in financial planning is not technological.

It is philosophical.

From:

“How do we manage your money?”

To:

“How do we increase your capacity to create sustainable wealth?”

When the spring flows, the reservoir fills.

When the reservoir fills, stability emerges.

When stability emerges, dignity returns.

That is the difference between managing dry wells and building sustainable ecosystems.

And if we are serious about moving from a nation of financial fragility to one of resilience, we must start where the water begins.

If you’re curious what that looks like in practice, explore the free Total Wealth Plan at:

Appendix A: Financial Security in the UK – Key Findings (February 2026)

A report published by Financial Planning Today (11 February 2026) highlights significant structural vulnerability in UK household finances, based on a new Financial Readiness Index.

Headline Findings

- Only 11% of British adults meet the benchmarks for true financial security.

- 46% report feeling financially secure, revealing a substantial gap between perception and actual preparedness.

- The UK was categorised overall as “financially uncertain”, with average resilience scores well below robust thresholds.

Financial security in this context was defined as having adequate savings, emergency buffers, long-term planning, and readiness for financial shocks — not merely subjective confidence.

Preparedness Levels

- 19% were assessed as fully prepared for both current and future financial needs.

- 17% were not prepared at all.

- Even among households earning over £100,000, financial insecurity remained present.

- Younger adults and mid-career families (particularly ages 35–44) scored lower due to housing costs, childcare pressures, and limited savings accumulation.

Broader Context

These findings align with wider UK data indicating structural fragility:

- Approximately 1 in 10 adults have no cash savings.

- Many households lack sufficient emergency reserves.

- Millions face financial vulnerability characterised by debt burdens, rising living costs, and minimal financial buffers.

Implications for Financial Planning

The findings suggest three critical priorities for the profession:

- Closing the gap between perceived and actual financial resilience.

- Strengthening foundational financial buffers and long-term planning capability.

- Providing targeted support and education to vulnerable and pressured demographic groups.

The data above describes financial fragility, but it does not fully explain its cause. When nearly nine in ten adults fall short of true financial security, the issue is not simply inadequate saving behaviour — it is constrained productive capacity. Financial capital can only accumulate when income is resilient, adaptable, and expandable. The missing variable in most resilience discussions is human capital: the skills, adaptability, entrepreneurial capability, and earning power that generate sustainable cashflow. Without strengthening that underlying source, emergency funds and investment strategies remain structurally limited. To move the Financial Readiness Index meaningfully upward, the starting point must be regeneration of income capacity — restoring flow before optimising storage.