An Academy of Life Planning perspective

Why this article exists

The regulatory outlook for 2026 is framed as modernising, pro-growth, and inclusive. Many of the measures are presented as pragmatic responses to low participation, technological change, and political pressure to stimulate economic activity.

From the Academy of Life Planning’s standpoint, the test is not whether these measures increase activity, but whether they reduce harm, strengthen resilience, and build prosperity that can endure. Our concern is practical and human: we want fewer people harmed by the financial system at the end of 2026, not more.

That requires questioning some deeply embedded assumptions—especially what is meant by growth, participation, and protection.

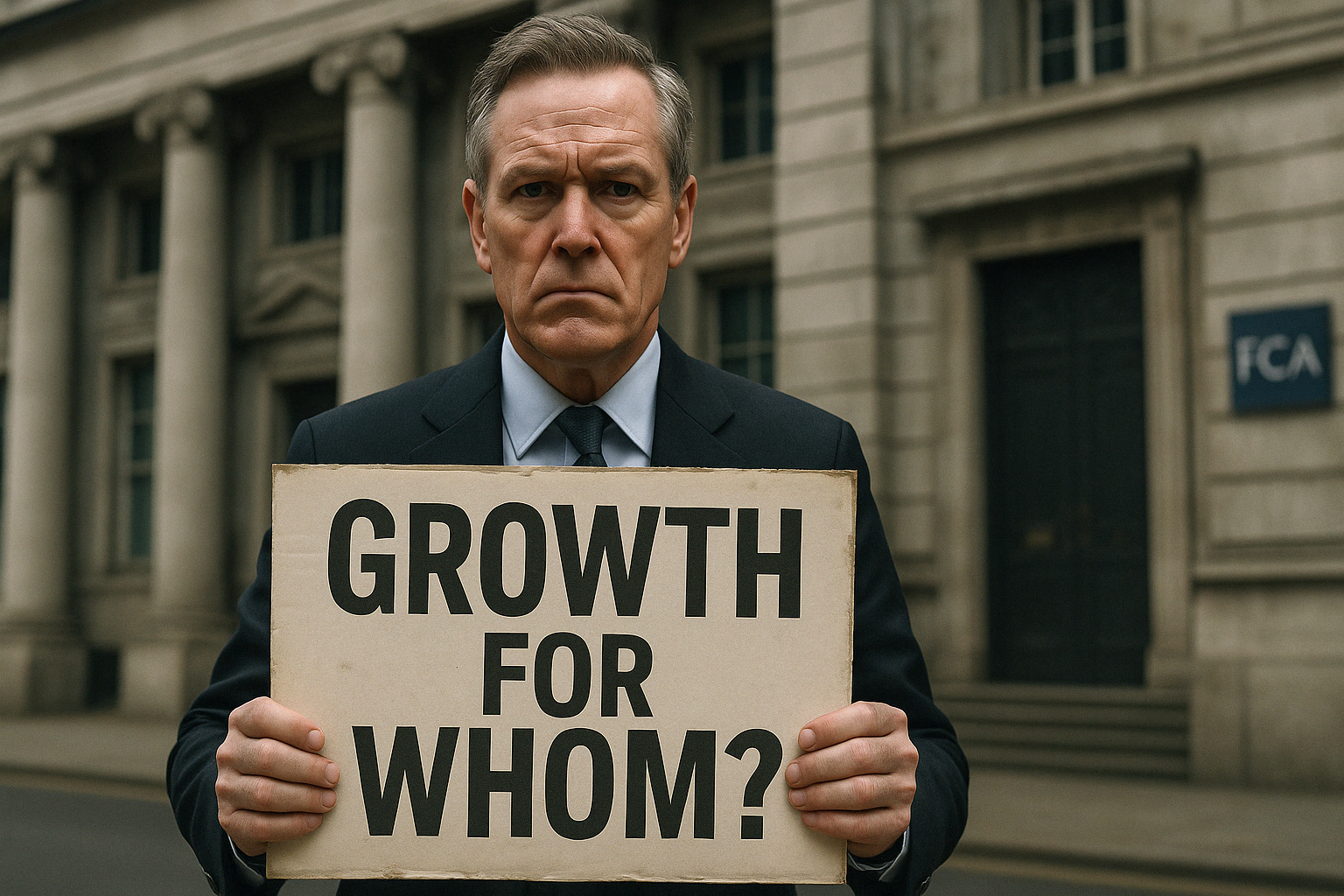

Growth is not inherently good — it is conditional

Growth is often treated as an unquestionable good, something that must be pursued and accelerated. In reality, growth is neither neutral nor guaranteed to be beneficial. It always has a direction, a distribution, and a cost.

A growth strategy should therefore begin with a prior question: growth of what, for whom, and at whose expense?

In advanced economies, the problem is not a shortage of capital seeking returns. Capital is abundant. The constraint is that large portions of the population lack the human capacity, security, and resilience needed to participate productively without being harmed.

When growth strategies focus on expanding financial activity without addressing this constraint, they do not create prosperity. They redistribute risk downward.

Participation is not automatically progress

“Wider participation” in investments is frequently presented as a social good. That assumption deserves scrutiny.

For households living close to the margin, participation in financial markets does not always build wealth. More often, it:

- diverts scarce income away from immediate needs,

- exposes people to volatility they cannot absorb,

- and transfers fees and risk to those least able to carry them.

From years of witnessing real cases through consumer advocacy, transparency work, and recovery support, it is clear that many people are already over-exposed. Confidence in investments is not too low; it is often unjustifiably high. Complexity, marketing narratives, and behavioural nudges routinely obscure risk.

Encouraging greater participation without first strengthening financial resilience does not empower people. It places them in harm’s way.

The hidden cost of financial confidence

A recurring pattern in cases of financial harm is not ignorance, but misplaced confidence:

- confidence in structures that appear legitimate,

- confidence in advice that is, in reality, sales,

- confidence that regulation implies safety.

When people believe systems are designed to protect them, they take risks they otherwise would not. The result is not empowerment, but catastrophic loss—often discovered too late to reverse.

Any regulatory agenda that increases exposure without first rebuilding trustworthiness risks producing more victims, not fewer.

The “advice gap” misdiagnosis

Low levels of regulated advice uptake are frequently cited as justification for new distribution models. But framing the issue as an “advice gap” masks a deeper problem.

What many people experience is not a lack of advice, but:

- advice they cannot afford,

- advice tied to product sales,

- or advice that does not reflect their lived reality.

When sales activity is relabelled as “support” or “guidance”, expectations are quietly reshaped. In several jurisdictions, the use of the word advice by product distributors is tightly restricted precisely because of this risk. Where that clarity is absent, consumers reasonably assume a duty of care that may not exist.

This is not a semantic issue. It is a liability and harm issue.

Targeted support and the amplification of risk

Targeted support is intended to help groups of consumers make decisions more confidently. The concern is not the intent, but the context in which it operates.

Targeted support is most likely to be used:

- near retirement,

- during financial stress,

- at moments of transition or uncertainty.

These are periods of heightened vulnerability. Introducing scaled suggestions at these points—especially without full advice safeguards—amplifies risk rather than reducing it.

Where judgement is required, and where outcomes depend on segmentation, data quality, and interpretation, harm does not need malice to occur. Systemic design alone is enough.

AI, opacity, and accountability

The growing use of AI in financial services is often discussed in terms of efficiency and innovation. Less attention is paid to accountability.

Existing regulatory frameworks assume decisions can be explained, challenged, and traced to responsible individuals. AI-mediated systems complicate all three. When harm occurs, it becomes harder for consumers to understand what happened, harder for firms to evidence good outcomes, and harder for regulators and ombudsmen to assign responsibility.

Growth built on opaque decision-making is fragile. It accelerates activity while weakening trust.

Asset thresholds and invisible vulnerability

Proposals to reduce protections for individuals above certain asset thresholds are often justified as focusing regulation where it is “most needed”. The problem is that asset size is a poor proxy for safety.

Many people with substantial assets are:

- asset-rich but income-poor,

- highly concentrated in one sector,

- dependent on illiquid or cyclical value,

- exposed to irreversible loss.

Removing protections based on headline figures does not remove vulnerability. It simply makes it harder to see—and harder to remedy when harm occurs.

Growth within planetary limits

Any discussion of growth that ignores environmental constraints is incomplete.

If everyone consumed at the level of the average high-consumption economy, we would require multiple planets to sustain it. That is not a future-facing growth strategy; it is ecological drawdown.

True growth must therefore be qualitative, not merely quantitative:

- growth in capability, not consumption,

- growth in resilience, not extraction,

- growth in contribution, not throughput.

Short-term gains for humanity at the expense of the planet are long-term losses for humanity.

Where sustainable growth actually comes from

The most reliable driver of long-term prosperity is not increased financial participation, but expanded economic agency.

Investment in human capital—skills, health, adaptability, confidence, and local productivity—allows more people to contribute meaningfully. It reduces dependency, increases real output, and circulates value within communities rather than extracting it into distant balance sheets.

This is growth that compounds across generations.

A measure of success for 2026

If the regulatory changes ahead result in:

- more people exposed to risks they do not understand,

- more complexity without accountability,

- and more households needing recovery and redress,

then the strategy will have failed, regardless of headline growth figures.

A successful agenda would be one where:

- fewer lives are financially devastated,

- fewer people require rescue after harm,

- and more people are able to sustain themselves without being drawn into extractive systems.

That is not anti-growth.

It is growth that respects people, future generations, and the planet we all depend on.

At the Academy of Life Planning, that is the outcome we are working toward—quietly, persistently, and with those most affected always in mind.