When Legal Process Becomes a Legal Obstacle

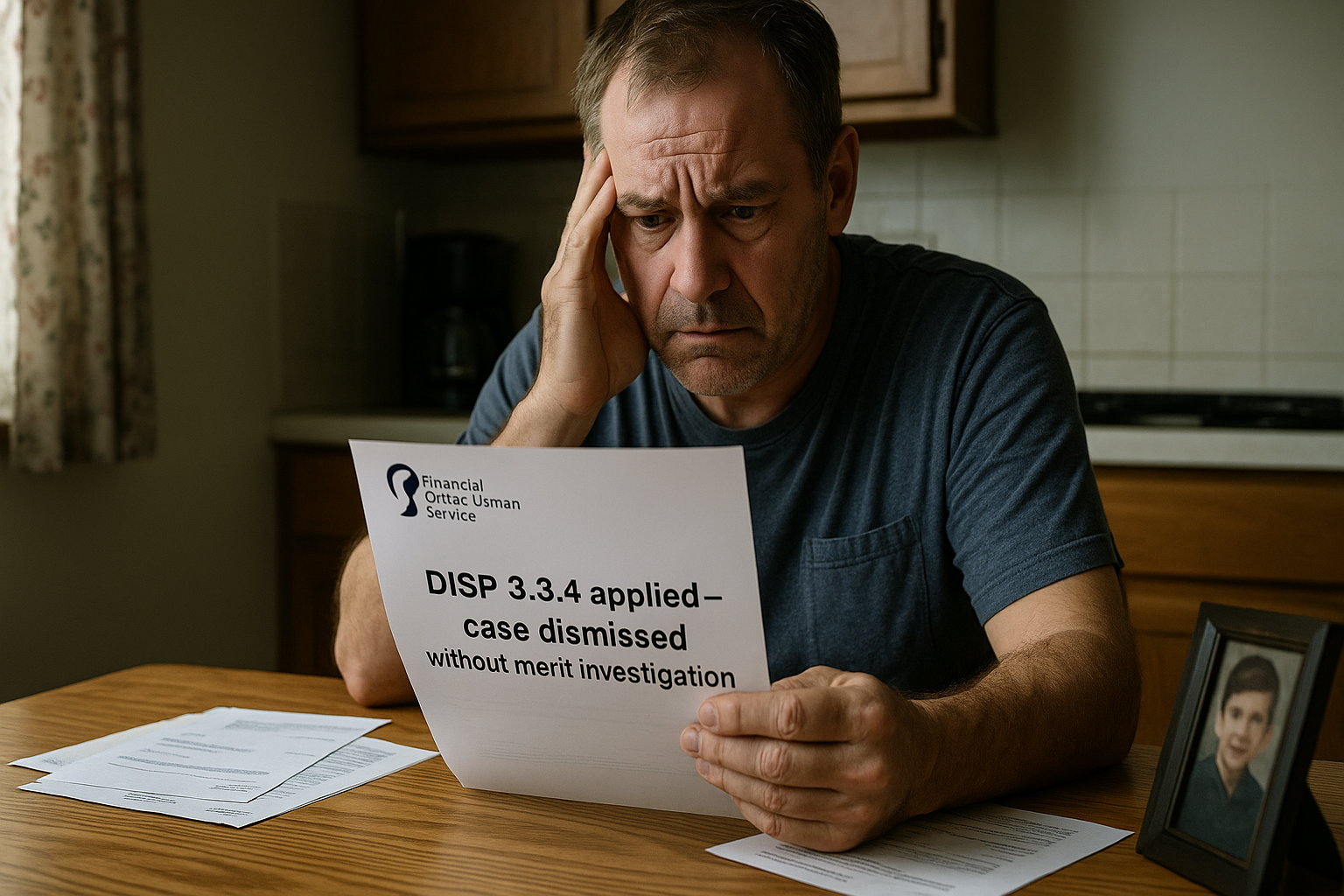

Behind the polished veneer of consumer protection in the UK’s financial services sector lies a procedural trapdoor—DISP 3.3.4 of the FCA Handbook.

At first glance, this rule appears rational: it allows the Financial Ombudsman Service (FOS) to dismiss complaints without investigating the merits if they fall outside defined criteria—such as being frivolous, outside time limits, or legally complex.

But here’s the deeper concern: in practice, DISP 3.3.4 has become a systemic tool for avoidance, enabling institutions to close down inconvenient truths and sidestep accountability.

A Loophole in the Name of Efficiency

This rule was revised after the 2015 Alternative Dispute Resolution (ADR) Directive, which aimed to make it easier—not harder—for consumers to raise concerns. Yet since then, a culture of exclusion has quietly taken root.

Instead of empowering victims, DISP 3.3.4 is now routinely cited to:

- Reject complaints that touch on deep misconduct, often with little transparency.

- Push victims towards courts they can’t afford, especially when fraud or complex jurisdictional issues are involved.

- Dismiss systemic concerns under the guise of being “too complex” or “better handled elsewhere.”

When Regulators Say ‘Not Our Job’

This misuse of procedure isn’t happening in isolation. Victims are increasingly reporting being:

- Bounced between the FOS, FCA, FSCS, HMRC, and courts—with no body claiming responsibility.

- Blocked by legal privilege, non-disclosure tactics, and regulatory handwashing.

- Punished by process—forced to relive trauma without closure, while institutions walk away unexamined.

Even the Mastercard Competition Appeal Tribunal and local authority pension cases have begun to expose how SRA-regulated law firms, public bodies, and pension trustees use these legal mechanisms—not to protect the public, but to protect themselves.

The Cost of Obstruction

This isn’t just a technicality—it’s a national cost:

- Withheld pensions mean unpaid taxes to HMRC and hardship for retirees.

- Unresolved fraud cases undermine faith in financial systems and regulators.

- Dismissed complaints deny justice to victims and enable repeat offenders.

Time for Transparency, Not Technicality

If we are serious about restoring trust in financial justice, DISP 3.3.4 must be reviewed and reformed.

- Consumers need a fair route to redress, not a revolving door of “not our jurisdiction” responses.

- Regulators need to act on substance, not sidestep complaints on procedure.

- And legal professionals must stop enabling these outcomes through silence or strategic obstruction.

As public awareness grows, this rule—once buried in an obscure section of the FCA Handbook—may well become a symbol of systemic failure. It’s time we opened the door it has closed for too many.

🙌 Stand With Ian. Speak the Truth. Spark the Change.

Ian Davis fought not just for himself, but for all of us.

If you’ve been affected by financial crime, or if you believe no one should ever suffer in silence—share this story.

Raise awareness. Demand reform. Reclaim your power.

- 🔗 Share this post with someone who needs to read it.

- 📣 Join the movement to unmask the robbers and rebuild lives.

- ✍️ Leave a comment to honour Ian or share your story.

- 🤝 Volunteer or collaborate with the Academy of Life Planning or Transparency Task Force.

🕯️ Let’s make sure no voice like Ian’s is ever silenced again.

Your Money or Your Life

Unmask the highway robbers – Enjoy wealth in every area of your life!

By Steve Conley. Available on Amazon. Visit www.steve.conley.co.uk to find out more.