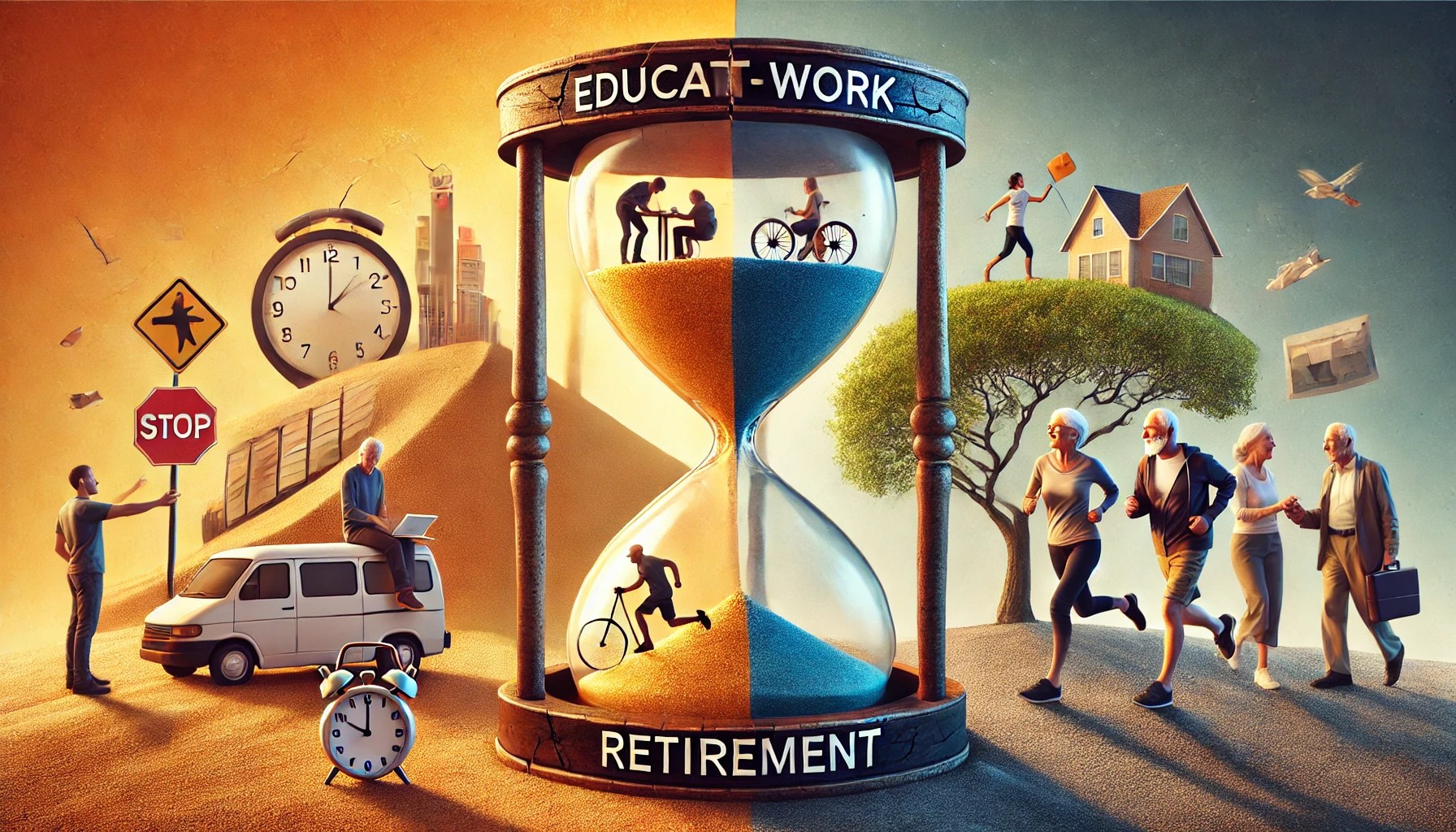

The financial industry has long relied on a model that divides life into three distinct stages: education, work, and retirement. This model, while simple and easy to understand, has become increasingly outdated as we face the realities of longer lifespans and evolving career paths. Yet, many asset managers continue to push this narrative, often instilling fear in people by suggesting they must drastically increase their assets under management or risk financial ruin in retirement. This fear-mongering approach not only ignores the complexities of modern life but also overlooks the importance of investing in human capital.

The Reality Behind Retirement Savings

Recent research from the Phoenix Group highlighted a concerning trend among Scots aged 40 to 66: 75% feel unprepared for retirement. This statistic, while alarming, is often used by asset managers to fuel the notion that people need to save more, often to the tune of £300,000 or more, to achieve a ‘moderate’ standard of living in retirement. The message is clear: if you haven’t saved enough, you’re in trouble.

However, this message is overly simplistic and fails to address the broader context of financial planning in today’s world. Professor Andrew J. Scott of the London Business School argues (at 28 mins + on this podcast) that the traditional three-stage life model—where individuals accumulate funds during their working years and then decumulate them in retirement—is no longer sufficient. With the possibility of living to 100 or beyond, the idea that one can simply save enough to retire comfortably at 65 is increasingly unrealistic.

The Old Model vs. Today’s Reality

Asset managers who continue to advocate for the old model are ignoring the fact that modern life is far more complex. People are living longer, pursuing diverse career paths, and often working well into what was traditionally considered “retirement age.” The idea that one must accumulate a massive nest egg to survive these later years is based on outdated assumptions and does not consider the various ways individuals can continue to generate income, maintain their health, and stay engaged with the world around them.

This is where the concept of investing in human capital becomes crucial. Rather than solely focusing on financial capital, individuals should also be investing in their health, skills, relationships, and purpose. These elements not only contribute to a fulfilling life but also provide the flexibility and resilience needed to navigate the uncertainties of a long life.

Fear-Driven Selling: The Real Problem

The fear-driven approach used by many asset managers is not just misleading; it can also be harmful. By scaring people into thinking they need to save more than they possibly can, these firms are pushing individuals into making financial decisions that may not be in their best interest. This approach also perpetuates a sense of helplessness and inadequacy, particularly among those who already feel unprepared for retirement.

“Many asset management firms are enthusiastic about the idea of a 100-year life because they believe it means people will need to save more. However, I believe this perspective misses the bigger picture. The real challenge of planning for retirement when you might live to 100 is not just about saving enough money—it’s about investing in your human capital. It’s incredibly difficult to save enough to retire comfortably at 65 or 70 and still have enough to last until 100. We need innovative income insurance solutions to support those with very long lives, while also preparing for the uncertainties ahead, like how long you’ll be able to work or what your health might be like. The key, therefore, isn’t just in your savings strategy, but in investing in your human capital—your health, skills, sense of purpose, curiosity, engagement, and relationships. These are the assets that will help you maintain your financial security over the long term.” – Andrew J. Scott

What’s needed is a shift in focus from purely financial accumulation to a more holistic view of life planning. This includes recognising the value of ongoing learning, career flexibility, and health maintenance as integral parts of a secure and fulfilling life. By doing so, we can move away from the outdated three-stage model and towards a more realistic and empowering approach to planning for the future.

Conclusion: A New Approach to Life Planning

The traditional three-stage life model, once a cornerstone of financial planning, is increasingly irrelevant in today’s world. Asset managers who continue to promote this model, often through fear-based tactics, are doing a disservice to those they aim to help. Instead, it’s time to embrace a more nuanced approach that recognises the complexities of modern life and the importance of investing in human capital.

As we move forward, the conversation around retirement should shift from one of fear and scarcity to one of empowerment and possibility. By focusing on the full spectrum of life’s opportunities and challenges, we can help individuals not just survive but thrive in their later years, regardless of how much they have in their pension pot.

Q&A on Rethinking Retirement and the Three-Stage Life Model

Q1: What is the traditional three-stage life model?

- A1: The traditional three-stage life model divides life into three distinct phases: education (where you acquire knowledge and skills), work (where you build your career and accumulate savings), and retirement (where you live off the savings accumulated during your working years). This model has been the foundation of retirement planning for decades.

Q2: Why is the three-stage life model considered outdated?

- A2: The three-stage life model is increasingly seen as outdated because it doesn’t account for the complexities of modern life. People are living longer, pursuing multiple careers, and often working beyond traditional retirement age. This model assumes a linear life path, which doesn’t reflect the diverse and dynamic ways people live and work today.

Q3: How do asset managers use the old model to scare people?

- A3: Some asset managers use the outdated three-stage model to create fear around retirement savings. They suggest that if people don’t drastically increase their assets under management, they won’t have enough money to retire comfortably. This fear-mongering approach pushes people to focus solely on financial accumulation, often leading to stress and poor financial, and possibly health, decisions.

Q4: What alternative approach is suggested in the article?

- A4: The article suggests shifting the focus from purely financial accumulation to a more holistic approach that includes investing in human capital. This means prioritising health, skills, relationships, and lifelong learning. By doing so, individuals can create a more resilient and adaptable financial plan that aligns with the realities of longer life expectancies and diverse career paths.

Q5: What does investing in human capital involve?

- A5: Investing in human capital involves nurturing your health, continuously learning and developing new skills, maintaining meaningful relationships, and staying engaged with your community and passions. These elements not only enhance your quality of life but also provide a foundation for financial security by enabling you to adapt to changes in work and life circumstances.

Q6: How can people prepare for retirement if the old model doesn’t work?

- A6: Preparing for retirement today requires a more flexible and personalised approach. Instead of focusing solely on saving a large sum of money, individuals should consider multiple income streams, including part-time work, investments, and social security. Additionally, staying healthy and engaged in purposeful activities can help reduce financial pressures in later years.

Q7: What should people do if they feel unprepared for retirement?

- A7: If you feel unprepared for retirement, it’s important to start by assessing your current situation and setting realistic goals. Seek guidance from trusted financial planners or use low-cost resources for DIYers like Planning My Life. Remember that it’s never too late to invest in your human capital and make adjustments to your financial plan to better align with your long-term needs.

Q8: How does this new approach to retirement planning benefit society?

- A8: This new approach to retirement planning benefits society by promoting greater financial resilience and well-being among individuals. It reduces the pressure on social safety nets and encourages people to remain active and engaged throughout their lives, leading to healthier, more fulfilling communities. Additionally, it shifts the narrative from fear and scarcity to empowerment and possibility.